Hi,

Myself Aswin, 29 year old salaried individual and I’m new to equities. Started investing in Jan 2017. I’ve been delaying from requesting a review of my investments fearing dilution of the quality of discussions in this forum. Of late I’ve been investing a sizeable portion of my savings into equities and when I look back, I understand that have been doing it in haste. To be honest, I need to take a step back and analyze what I’m doing. Hence I request you to review my investments.

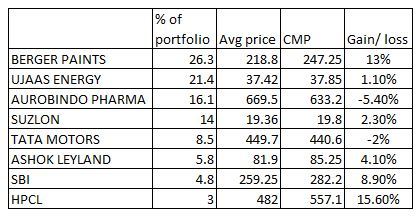

Berger paints: Invested in Jan 2017, when the markets were recovering from the effects of demonetization. Read news about their setting up of a new plant in Assam to cater to the requirements of North-East. Recently they started a plant in Pune also. Rising demand in the decorative and industrial paint sector are some of the positives for this sector.

Ujaas Energy: Invested a major chunk after Feb 22, when their promoters sold off a portion of their shares to fund new projects. The central government’s drive to promote renewables, especially solar rooftop, coupled with the fact that Ujaas energy is a leader in this sector attracted me.

Suzlon Energy: Articles in this forum on Suzlon being a turnaround story grabbed my attention. Suzlon’s latest S111 120m diameter turbine with PLF > 37%, decreasing debt etc looks good. I was tracking this company when it was in the mid 16s, but invested only recently. However, I consider this to be a risky investment in the short term, given the entry point.

Aurobindo Pharma: Their long list of ANDA approvals and acquisition of Portugese company Generis are positives. Read research papers citing capacity expansion (3 new formulation plants), which will positively impact their sales. Downside of the impact of USFDA is a concern and need to see how it turns out.

Tata Motors: Rising volumes and sales of Jaguar Land Rover in UK, EU and China and capacity expansion in Slovakia are positives. Supreme Court order on BS-III ban is a negative impact and I felt that the CMP is attractive. If they could export the old BS-III models, that would be good news.

Ashok Leyland: Same as Tata Motors with respect to BS-III. They are trying to increase their exports and have recently struck a deal to export engines to the US. Their use of IEGR system (intelligent exhaust gas recirculation) over SCR for BS-IV engines which does not require re-routing of piping looks interesting.

State Bank of India: Bought SBI in Jan when the banks were rallying. There was news of merger with other banks which would improve the efficiency and profits in the long run.

Hindustan Petroleum: Pricing power of OMCs to set the retail fuel prices attracted the most. This is a share I neglected all along. I should have added more when it was hovering in the 500-510 range.