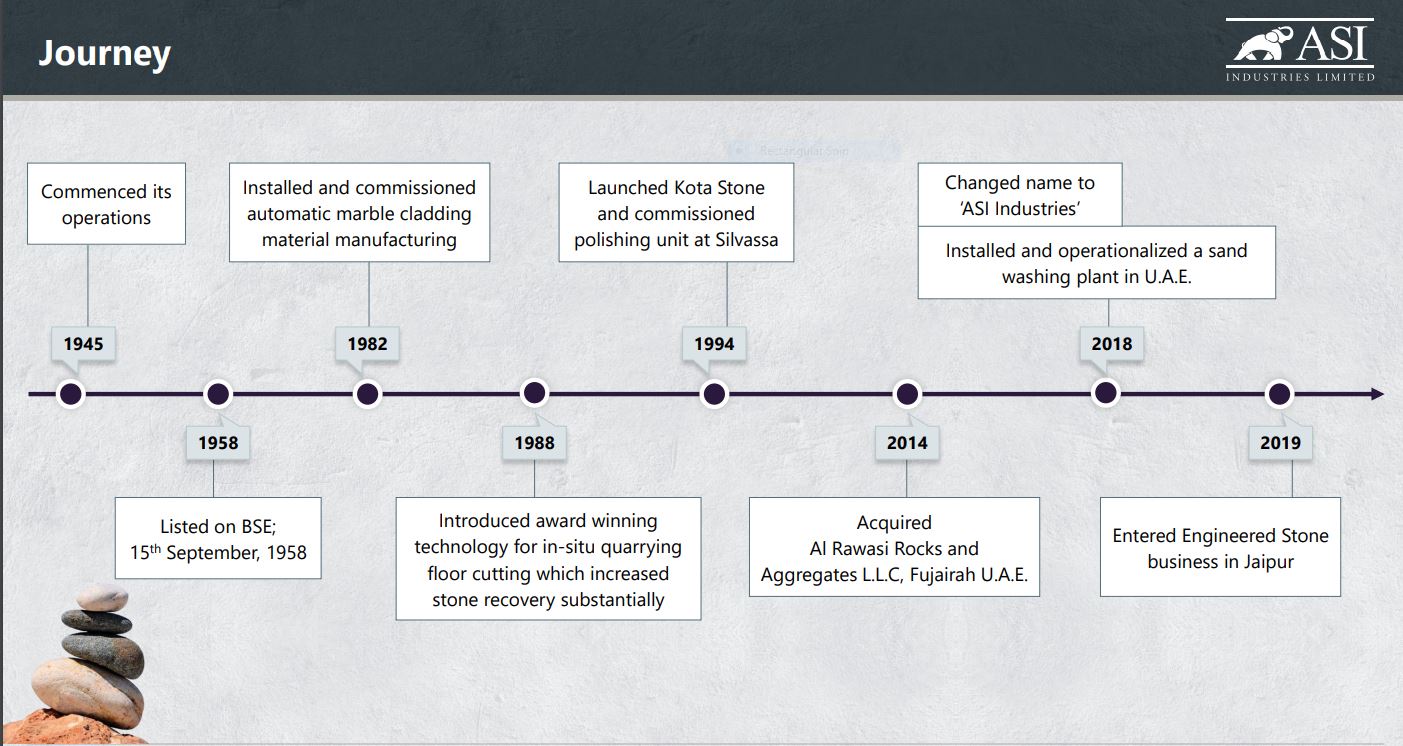

Been studying this company Associated Stone Industries. They own the largest quarries in the world spread across 10 sq kms in Rajasthan producing ~15 million sq m of Kotah stone every year. The company is promoted and run by Chairman & MD, Deepak Jatia (of the Jatia family (not certain of exact relations) – Hardcastle Restaurants, Pudumjee Paper Mills Pune, etc. Also, slightly irrelevant to the topic, but last year sold their home in Malabar Hill in Mumbai to Kumar Managalam Birla for Rs. 425 crore)

Consolidated Financials

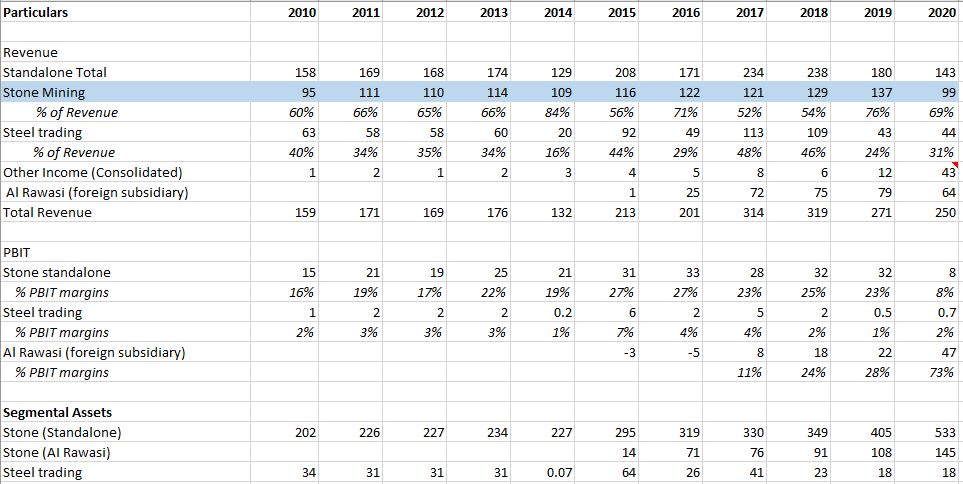

Rs. Crore FY14 FY15 FY16 Q1 FY17 Q4 FY16 Q3 FY16 Q2 FY16 Q1 FY16

Revenues 130.7 208.8 197.0 79.3 74.2 44.9 35.6 42.3

EBITDA 26.5 35.8 37.9 19.9 21.2 9.7 -4.9 11.9

EBITDA margin 20.3% 17.1% 19.2% 25.1% 28.6% 21.5% -13.7% 28.1%

EBIT 18.6 29.4 23.8 15.8 17.1 5.7 -8.7 9.6

PAT 10.1 14.5 7.8 9.0 10.2 3.9 -9.7 3.3

PAT margin 7.7% 6.9% 3.9% 11.4% 13.8% 8.8% -27.3% 7.8%

Adjusted EPS* (stock split) 1.5 2.2 1.2 1.4 1.6 0.6 -1.5 0.5

Book Value 26.6 28.3 29.2

They acquired, through their Mauritius-based subsidiary ASI Global Ltd (ASIGL), Al Rawasi Rocks and Aggregates LLC, Fujairah UAE, for $5.9 million. The company further invested around $11.89 million towards quarry development, plant & machinery & working capital margin. Al Rawasi Rocks and Aggregates is engaged in quarrying and mining. It offers extract rocks, marble, minerals and crushed limestone, etc having applications traversing a multitude of industries, including steel, chemical and construction plants. As per the annual report, they are looking to tap the opportunity of huge volume of industrial, infrastructure, reclamation and other construction work currently underway in the Arabian Gulf region. The estimated reserve of quarry of this Company is around 200 million tones which is sufficient for about 45 years of its operations. Also, according to some articles I researched, the UAE is the main source of limestone in India as almost all the steel plants on the west coast have reported import of limestone from either UAE or Oman because it is logistically cheaper for them to ship it from here rather than truck it from other places in India. It makes a $7-8 difference a tonne to just get it imported than trucking. Commercial production started only in June 2015 (Profitability was hence impacted in FY16 as utilisation was low).

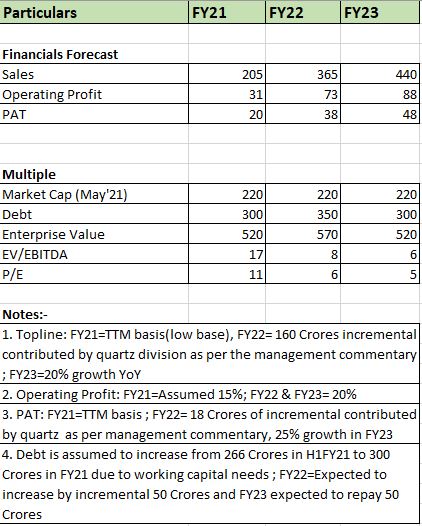

The company seems to have navigated well through the tough times faced by the mining industry – kept tight operational cost controls, retained customers by offering better payment terms to them, low leverage etc. The opportunities for the company seem huge with construction, infra related activities expected to pick up, with increased government focus. This may lead to increased revenue and profitability with increased utilisation of capacity in UAE.

The key concerns revolve around a slowdown in slowdown in growth of construction and infra activities. Further, environmental issues are another key issue which could affect the business. The company is also involved in certain trading of steel & other products which is a low margin business.

Current mkt cap is around 150 cr, CMP is Rs 23 and book value is Rs 29 cr. Further, it has been a consistently dividend paying company and also got a fairly lean balance sheet with a net d/e of 0.7. Q1 FY17 overall revenue stood at Rs 79 cr (vs Rs 42 cr YoY) with PAT of Rs 9 cr (vs 3.3 cr yoy). The UAE subsidiary contributed Rs 18 cr in Q1 and already reporting PAT of Rs 1 cr.

Would welcome any further inputs/suggestions that would help gain a better perspective about the prospects of the company.

Disclosure: Invested (5% of portfolio)