Hi all,

Perhaps this is already being discussed in some of the other posts, but I wanted to bring special focus on to this. The asset management industry in my view is poised to grow at a healthy rate over the next 25 years. This space is still very nascent in India and I am embarking on a detailed study on understand the industry, the different businesses within this space, the critical success factors and the key data points to follow. Some of my initial thoughts and notes below, please feel free to chip in. (Much of the data I will refer to below are from the HDFC AMC IPO Prospectus, if you are interested please feel free to read that report)

INDUSTRY

The asset management (mutual fund) industry in India has 41 players in total. A total of Rs.23 Trillion is being managed by these funds. The top 5 players and their market share are as below. June 2018 AUM is in trillions of Indian rupees. (The numbers are so mindbogglingly big that it is difficult to get heads around this; and the constant switching between Indian and international numeric system makes it even more complicated!)

| Mutual Fund Name | June 2018 AUM | June 2018 Mareket Share |

|---|---|---|

| ICICI Prudential Mutual Fund | 3.1 | 13.26% |

| HDFC Mutual Fund | 3.07 | 13.12% |

| Aditya Birla Sun Life Mutual Fund | 2.5 | 10.66% |

| Reliance Mutual Fund | 2.4 | 10.28% |

| SBI Mutual Fund | 2.3 | 9.97% |

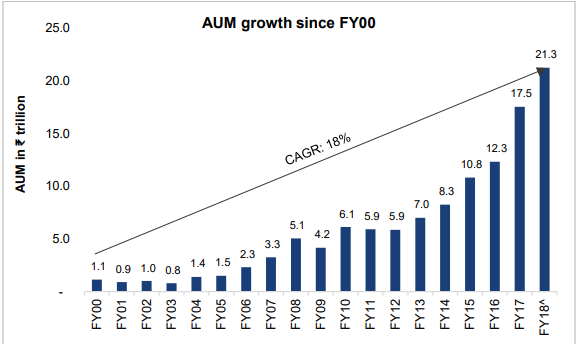

The overall AUM of this industry has grown 20X in the last 18 years. However much of the increase has happened in the last 5 years or so. So from a business cycle perspective, we are possibly at the peak of the most recent cycle. This is understandable given how much the equity markets have gone up in the same period.

However, what is interesting is that the total number of fund houses has only grown from 32 at the end of FY-2000 to 41 at the end of FY18. My guess is because of the nature of the economics of running this business. The larger the size, the higher the operational efficiencies. But more on that later.

Product/Service Offering

Principally, there are 3 types of product offering

- Actively managed equity funds

- Non-equity oriented debt funds

- Portfolio management and segregated account services

Then there are a combination of these - Hybrid funds, ETF, open ended and closed ended funds, index linked funds, arbitrage funds and the list is endless.

Market Size Estimate/Industry Potential

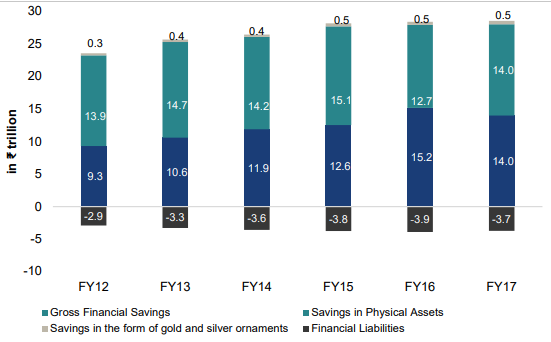

The Indian household on an average saves more than our counterparts elsewhere. Savings rate in India is 29% as against the world average of 25%. But most of these savings (Close to 70%) are tied to physical assets or gold and this is set to change. My hypothesis is that real estate prices have gone up so dramatically in Tier-1 and Tier-2 cities that the average middle class Indian family is no more able to afford buying 1 or more than 1 property. The proportion of net financial assets in total household savings

has seen a sharp rise from 31% in Fiscal 2012 to 42% in Fiscal 2017.

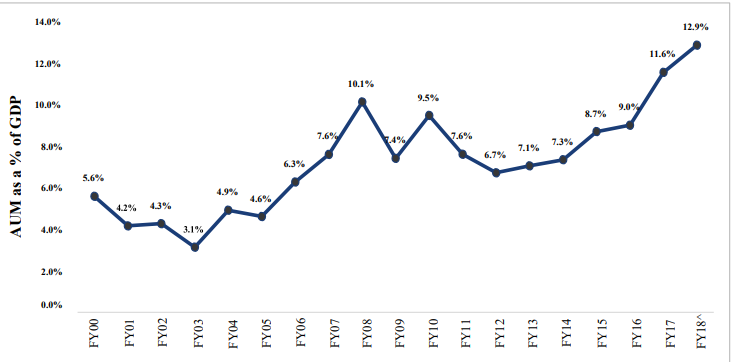

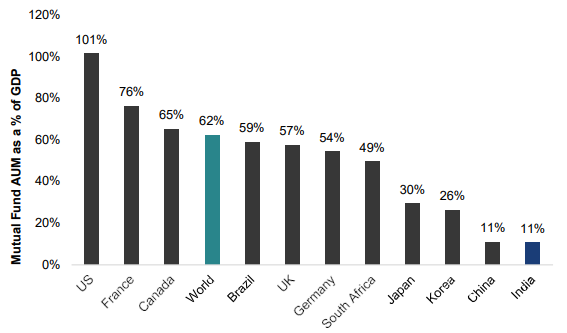

India is one of the least penetrated markets in the world. Penetration is typically measured as the AUM with Mutual funds to GDP. In India this is now at around 12%-13%.

This is nowhere near the level of penetration some of the more developed economies in the world have.

And this will change, primarily because of 3-4 factors.

- Overall market expansion - % coverage of the overall population. Formalisation of the economy will make financial inclusiveness for a much larger population possible.

- Growth in financial assets as a % of overall household savings will increase due to the rather slim investment opportunities that gold and real estate offer.

- GDP per capita will grow - Meaning people will get paid more and hence save more.

- Awareness of financial products and the long term wealth creation potential of equity oriented schemes will increase.

Should the Indian economy continue to grow at 7% levels for the next 10 years, GDP of India will be about USD$5 Trillion in 2025. Assuming the penetration of mutual funds increase from 13% of GDP to 25% of GDP, total AUM under this industry will be $1.25Trillion or about 85 Trillion rupees (4X growth compared to where we are today). That is a CAGR of 15% over the next 10 years.

Profitability Drivers

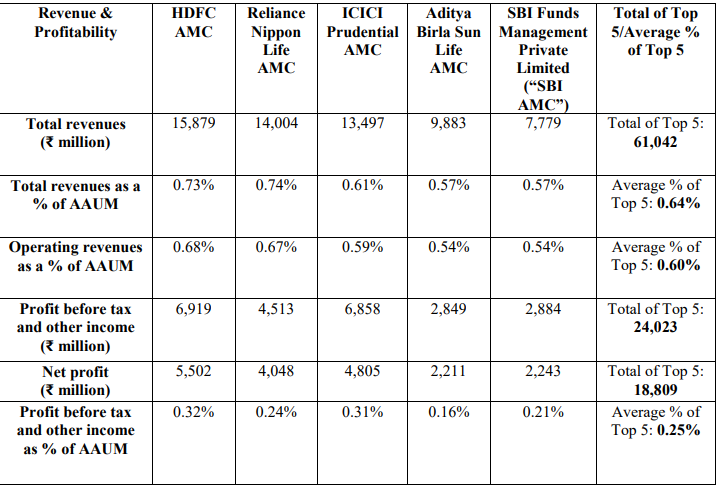

- From a unit economics perspective, equity funds earn the highest fee. So larger the share of equity oriented AUM, better the profitability. This table below from the Crisil research report gives an excellent view. PMS funds also earn a significantly higher fee compared to mutual funds. However, even for the largest player today PMS is only about 2.5% of the overall portfolio. So I do not know the exact extent to which PMS services can impact revenue growth/profitability growth for a mid to large sized player.

HDFC AMC leads the pack in terms of profitability simply because of the better mix between equity and non-equity oriented schemes. While HDFC’s overall market share is about 13%, it has the highest market share of 17% of actively managed equity funds.

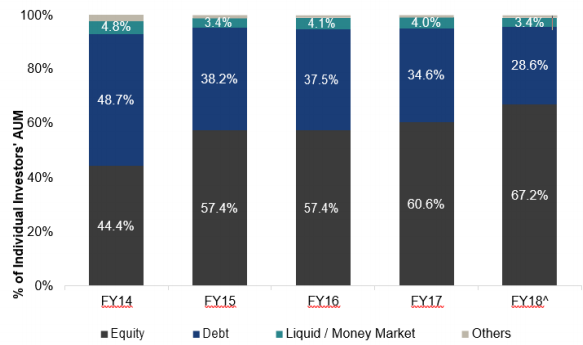

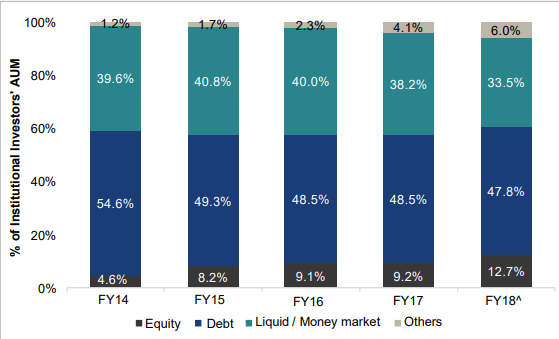

- The mix between the type of customers the AMC has plays a key role as well in determining profitability. Institutional customers tend to have shorter holding periods and are mostly invested in money market funds or short term debt funds (which makes sense because corporate funds will need to be called back when there is a business requirement). Individual investors on the other end are invested for the long run.

- Source of funds play a very important role in determining cost structure of these businesses. Direct funds tend to have no intermediaries/distributors and hence require no sales commissions to be paid out. However, distribution network are vital to expanding reach and to create brand recognition.

Risks

The fundamentals of the asset management industry is especially prone to the vagaries of Mr.Market. The industry primarily makes money out of fees on the AUM.

- Any under performance at an individual company level/de-rating of funds will lead to reduction in AUM and consequently reduction in overall revenue/profits.

- At an industry level, bear markets typically cause investors to pull out of equity markets and run for safety. So from a correlation perspective, AMCs will have a perfect Beta score of 1 with the index. But over a period of 25 years, the trend is only one way.

- Congruence of interests - I have read reports that ICICI Pru AMC bailed out the listing of ICICI securities and this is an area of grave concern. Incidents like this can have adverse effects from 2 perspectives - a)Consumer confidence goes down b)The industry opens itself up to a lot of scrutiny by the regulator.

- Speaking of regulator, government agencies can be notoriously active. They have however done good things over the last several years by influencing organisations like EPFO to invest in equity schemes (15% of their total assets), incentivising AMC’s to attract funds from B-15/B-30 (Top-15/Beyond-15 cities) by charging a higher fee, enforcing investments on creating awareness in the market by mandating AMCs’ spend etc.

I am still researching on what makes individual businesses successful in this space and what some of the long term critical success factors are (right to play, right to win). I will post updates soon after. Comments/thoughts/additional research/insights most welcome. I am a novice investor, so any help is appreciated.

Thanks!

Note : There are only 2 listed companies in pure play asset management today, Reliance AMC (which got listed recently) and HDFC AMC (which gets listed on the 6th of August). IIFL is going to list their 3 arms as three different companies on the exchange this year and their AMC is one of them. So not a lot of players are public. However, this might also change.

Disclaimer : This is not an investment advise, I have no investments either in any of the above mutual funds or on any of the listed AMCs.