Airtel bought 25 percent in Lavelle network.

ASM holds around 5 percent in Lavelle network.

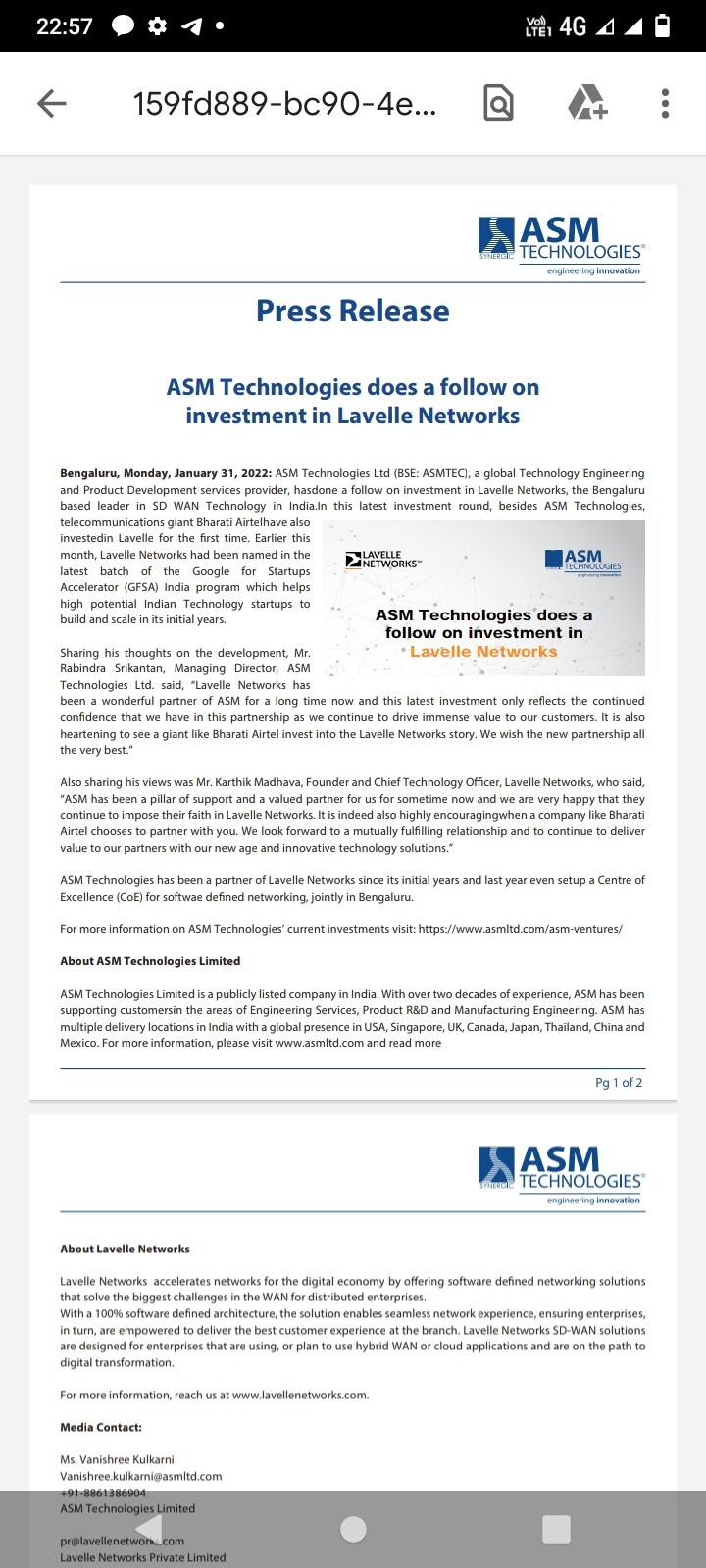

Big positive news for Lavelle network and ASM technology.

Airtel bought 25 percent in Lavelle network.

ASM holds around 5 percent in Lavelle network.

Big positive news for Lavelle network and ASM technology.

Asm tech does a follow on investment in Lavella networking along with Airtel.

A non IT company (Airtel) coming to driving seat bode well for ASM tech, as asm can continue to lead the software developmental work of this startup.

Asm tech Q3 result announced few days back.

Result looks average on profitability part.

Employee expense continue to scaleup & it affected margins and RM exp also shooted up in last quarter.

Other incom 3.8 cr helped to show decent PAT.

Segmental result shows DLM - design led manufacturing segment performing well recently. Most of the topline growth has come from this segment.

In their recent announcement they tied up for equipment manufacturing for semiconductor industries and Solar industries. Is there any idea how much revenue they are expecting from these two segments.

They just formed the JV, at this point of time we should ask how much money they are going to invest under this JV. That is the important thing , let us hope promoter conduct a concall so that we can ask all these.

What is so intresting is the background of the JV partner Hind High Vacuum pvt. This company is a very old company incubated under IISC bangalore and seems like have some capabilities in vacuum & thin film technology.As per below interview ISRO is one of their client.

This company had a solar division manufacturing solar modules which was divested to Swelect energy few years back.

Google to invest up to $1 billion in a partnership with Airtel as part of its Google for India Digitization Fund.Which includes equity investment as well as a corpus for potential commercial agreements. One month back Lavella networking was selected under google startup supporting programme.

Airtel also launching new product in association with Lavella networks.

Last 3-4 years Lavella have grown from a 5 cr base to 50 cr revenue. Now with the help of Airtel /Google this should continue to grow at similar pace in my opinion.

Asm tech remains a key operational and equity partner here, company website mentioned SD-WAN as a key networking service company provides.

Board of ASM Technologies approves rights issue up to Rs 11.50 cr | Business Standard News).

Rights Issue of 1share for every 10 shares held.

RIghts Issued at price of 115Rs per share.

Issue opens on 7th March

Right issue alottment of 10% of additional shares at 115 Rs is in best intrest of the existing shareholders.

But this is not the best thing to happen for the company. They could have easily raised 40-60 cr fund with the same dilution. But this is again in line with the company’s policy to continue to reward existing shareholders and protect their best intrest.

Iam not sure what is the best thing whether to protect the company’s intrest or shareholders intrest. Iam confused here.

Company also submitted an investor present.

Here they mention their two contradictory strategy of high dividend pay out & aquistion led growth.

As a minority shareholder and as an arm chair investor I can only say that so far promoter has done a great job and hoping for he continue to deliver in future.

68e6a1cf-b3e9-49d6-ad88-8f61489e3016 (3).pdf (1.2 MB)

Disclsoure : Continue to stay invested from very low levels inspite of volatility.

Yes, why paying high dividend at the same time raising fund through dilution?

Recent article on RV forms & Gears from Modern Manufacturing India magazine.

Few intresting insights.

Expanded business segments from automobile and heavy engineering to electronics & semiconductor verticals.

Company recently added large number of Japanese machining centres and allied equipments in phase 1 of a four phase expansion plan.

Asm tech has 1200 employees and dedicated team for designing of fixtures and special purpose equipments.

While anyone who has been monitoring this thread is well aware that ASM Technologies can stand to gain from the evolution of the semiconductor industry in India, I really wanted to do a deeper dive and confirm what exactly their level of expertise is in the space, and where in the value chain it is that they operate.

I drafted a short note covering what I found. I wish to add that after my research, I am even more bullish on the company. I wonder if larger players, who would have access to a larger client base, and can offer economies of scale to ASM are keeping tabs on this company.

Disclosure: Invested since June 2021, and I haven’t sold a single share.

2022.04.19 - ASM Technologies - A Snippet for Valupickr.pdf (1.0 MB)

Good report Ankit.

Appreciate your efforts.

But I feel you missed one key point with respect to semicon capabilities.

Asm tech has developed cloud based platforms, learning content and training modules for semicon industry. They also developed virtual chip fabrication labs (digital twin) where people can assemble and de-assemble equipments and see and understand operations.

Details here :

I am glad that you liked the report, Shanid!

I didn’t highlight the digital twinning work, because, to be honest, digital twin capabilities are to be expected as part of any half decent engineering services company. It would fall within ASM’s existing design and value engineering practice. Of course, the fact that they offer this would mean that they can go toe to toe with much larger engineering services companies, which is good news for us.

However, you make a very good point regarding the learning content and training modules that they offer. This conveys that ASM offers true thought leadership in the semiconductor industry!

This article gives a good perspective on why India need to build semiconductor equipment manufacturing facilities in our country.

@ankit_george , the report really provides a good snapshot of what ASM is into. I think what needs to be elaborated is how these expertise/capabilities (especially the ones in Semiconductor) fare wr.t. to those of the leading semiconductor players globally.

With the recent GOI push for bringing in investment in India for the semicon manufacturing and to make India a global hub for the same, there is no doubt that this industry will see some very big movement in next few years in India. But some of the points that come to my mind w.r.t ASM role.

@aspireinvestor , I am glad that you liked the report! While I am no expert in the semiconductor industry, I will take a stab at the three points that you have raised.

Foxconn is an electronics contract manufacturer, similar to a Dixon Technologies. They’re actively backward integrating, where they get more involved in chip/integrated circuit manufacturing (from “raw” silicon wafers). As this business gets further built out, they will play an increasingly foundational role in the semiconductor industry. ASM offers engineering services (design, protoptying, etc.), to companies that will build the equipment (and accompanying software, spares, etc.), which will be used in the plants that Foxconn and Vedanta plan to set up in India. For example, ASM offers services to a company like Applied Materials (a client as per the latest information I have), which then sells capital equipment to a Vedanta-Foxconn.

ASM has no intention to become an end-to-end semiconductor manufacturer. However, with the new joint venture with Hind High Vacuum, they are indirectly forward integrating, where they will start manufacturing some equipment that they design, instead of just offering design and prototyping services. The engineering research & development (ER&D) space, which ASM is in, has the potential to grow the same way that IT services grew in the past. I prefer these sorts of business models, as they’re capex light, and if well managed, they can generate much better margins (with less risk) than a capex heavy endeavour.

You’re spot on about where ASM is playing in the value chain! Whether it’s aircraft manufacturing, power plant design, automotive manufacturing, or any somewhat complicated manufacturing process, there are a host of suppliers, suppliers to suppliers, as well as service providers. As an investor, I prefer low capex business models, so I would rather put my money into an ASM Technologies, as opposed to a pure-play foundry (due to the high capex, cost overrruns, the payback time, the risk of overcapacity in the future, etc.). In addition, as a public investor in India, I don’t even have the option to invest in a company whose core business is in foundry/fab construction and operation.

Hope this reply helps!

ASM Tech recent annual report.

I promised myself (and others) that I would write an updated note on ASM Technologies after they shared their FY2022 Annual Report. While I am a few days late, I started on this note at 11 am this morning, and just finished it now. While I proofread the document once, please do excuse any typos, as I finished this document (attached) in one sitting.

Also, in case you are wondering why you should read this note, I have shared its Executive Summary below:

Anyone that is a veteran of the Indian stock market can vouch for the power of compounding interest and playing the long game, especially in a country like India that has a strong macroeconomic foundation and promising future prospects. Of course, sitting on any random stock for an indefinite amount of time does not do one any favours. The most profound long-term gains can be realized when you buy into a well-run company that is operating in an industry whose potential is yet to be fully understood and appreciated.

In terms of examples, imagine if you bought and held onto Bajaj Finance shares before the acronym NBFC became commonplace, or perhaps Info Edge shares before you got a high-speed Internet connection at home. How about buying Pidilite Industries shares the first time you used Fevicol?

While Internet penetration and the flow of information is at an all-time high, I still believe that there are multiple opportunities in their nascent stage that are yet to enter the public gaze. Any long-term investor in IT Services companies has no doubt probably enjoyed market beating returns for some time now. However, astute investors may have noticed that IT Services is a maturing industry. Forward-thinking firms in this industry have already started making meaningful strides in another emerging industry, Engineering, Research and Development (ER&D).

ER&D services are those that augment or manage processes that are associated with the creation of a product or service, as well as those associated with maximizing the life span and optimizing the yield associated with a product or asset. ER&D services can include engineering analysis, product design/co-design, product lifecycle management, and quality assurance, all the way to prototyping and manufacturing.

Courtesy of a good friend that I met while briefly working in venture capital (Hi Priyanka!), I was introduced to a company that is well positioned to take advantage of the rise of ER&D in India. The company is ASM Technologies, a microcap company at this point, with the following characteristics:

• FY21-FY22 Revenue Growth nearing 40%

• FY21-FY22 PAT Growth of ~62%

• 3-year Revenue CAGR of ~30%

• Trading at a measly 2.37 Market Cap/TTM Sales multiple

• Deep expertise in engineering services to the semiconductor industry

• JV partner in a newly launched entity that is manufacturing equipment for the semiconductor and solar industries

• Owner of a subsidiary that is one of Asia’s largest fixtures manufacturers

• Early investor in an SD WAN solutions provider (now 25% owned by Bharti Airtel)

There is a lot more that I can share, but it would require that you read the rest of the report. In my view, contingent on good execution, I am of the belief that this company’s stock price offers investors the opportunity for a 144% upside from current levels.

Hope you all enjoy this note!

Disclaimer: I am not SEBI registered. The information provided here is part of my personal due diligence prior to buying, deciding to keep holding, or selling a stock. Always consult your own financial advisor before making any decisions.

2022.06.27 - ASM Technologies - FY2022 Analysis and Thoughts.pdf (1.3 MB)