Latest credit rating report gives excellent pointers towards the capex and other things. Few important points.

. Revenue is expected to improve in FY 22 with stable margins on the back of increased orders from existing customers.

. Total capex planned is 50 cr for next two years. In this 15 cr will be funded through equity and 35 cr will be funded from debt. Capex will take two years time and revenue to start flowing from FY 2024.

3 . Semi conductor and networking are two segments contribute majorly to the revenue. Technological advances are very high in these segments so companies continue to invest heavily in RnD, this gives the recurring revenue stream to ASM tech.

Company allready announced right issue for a 15 cr fund raising. Given the long gestation period of capex what I feel is this may not be normal capex by an IT company. May be a foray into manufacturing thing. Promoter remain tight lipped and focusing his job in hand, so we can only guess what is coming up.

Cyient Q2 result is out few days back and some insights from their investor presentation.

Design led manufacturing-DLM is one of the key segement for them other than IT , digital and Engg RnD services. Company experiencing strong tailwinds for this segment and H1 business grown 20% yoy. Company seeing more and more business moving out of China, china+1 is benefiting them and expecting this segment to grow 15-20% for rest of the year.

If we carefully go through the AR of ASM tech we can see them mentioning about DLM in few places.

The article ended on a promising note…

We are in 2021 end.

This is what the management had to say in their 2021 AR:

“SmartFix 4.0 is an industrial AI solution offering a potent combination of world-class hardware, software and data analytics to increase manufacturing yield and throughput. With a robust global client base and a host of strategic partnerships with multiple OEMs, SmartFix is set to deliver value over the next two years.”

Revenue 47.7 cr 15% up qoq 50% up yoy.

Ebitda 7.2 cr 40 % up qoq 50% up yoy.

Ebitda% 15.5% consistently improving

PAT 4 cr 30% up qoq 70% up yoy.

EPS 4 Rs

Interim dividend 2.5 Rs

These numbers indicates that this smallcap IT company with niche capabilities and skills with 25 years of un-interrupted dividend track record has entered into a growth stage.

Non current assets increased from 36.2 cr to 43 cr , including a cwip of 2.9 cr.

(Some expansion happening ??? )

Borrowings increased from 35 cr to 40 cr.

Receivables increased from 30 cr to 38 cr.

Employee expense again up 7% qoq.

H1 Revenue is 89 cr and PAT of 7.7 cr,

base case we can expect the company to do 170-180 cr revenue and 13-15 cr PAT for this financial year. Stock trades at 18-20 PE of expected FY 22 EPS.

In my opinion, this company is a sort of baby version of Tata Elxsi, offering value-added engineering services. It is still trading at a very cheap valuation. If they increase revenue consistently by 10% every quarter, and improve margins, this company ought to trade closer to 4x revenue, instead of ~2x revenue today.

The reason it is trading at cheap valuations is because the it engineering services field is getting crowded. Smaller firms need to show consistent growth yoy. ASM has not been able to bring in profits at the same rate as it’s revenue has improved.

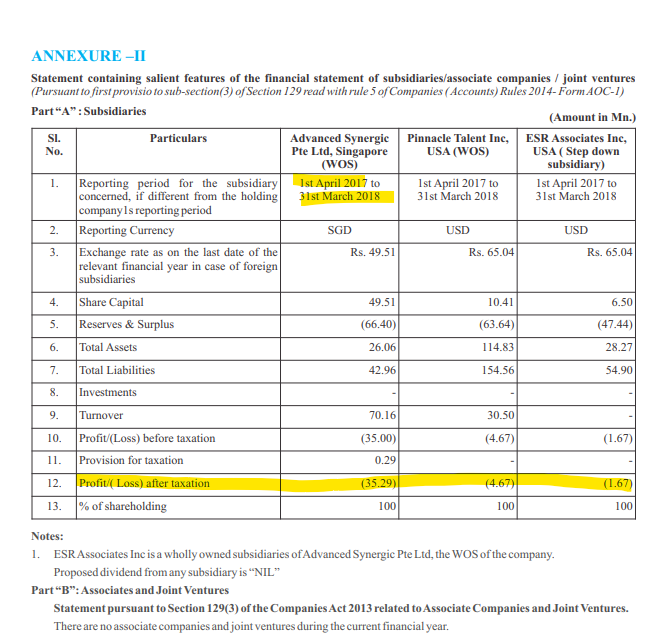

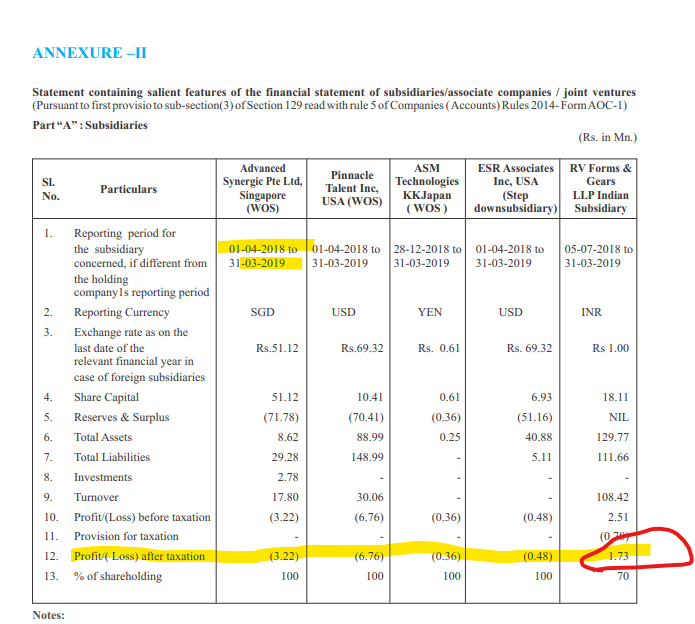

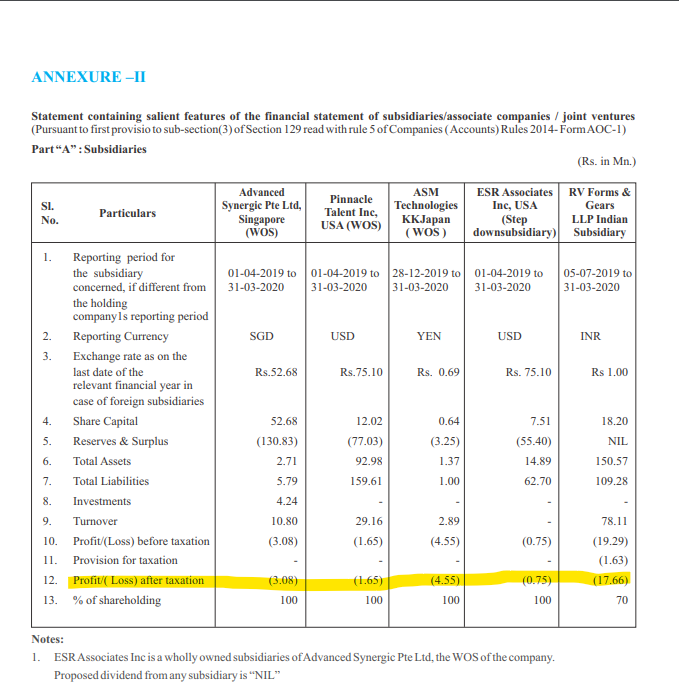

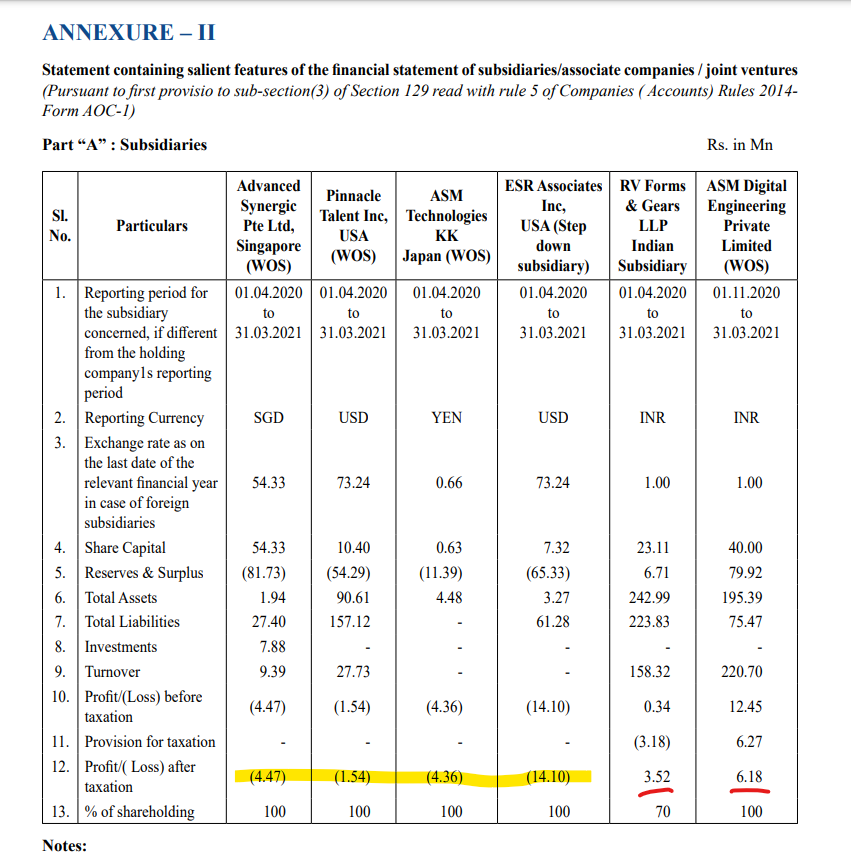

Another important point in the results was the complete erosion of subsidiaries in Japan and USA. This, it seems has compelled them to raise capital via rights issue.

I see future in forms and gears and an able leadership can go a long way in making ASM a high growth company. It’s dividend policy is a good comfort for the investors.

Subsidiaries in UK and Japan all put up to support the company to scale up revenue, these subsidiaries working as a marketing or sales centres. Japan is a newly added geography as per AGM note.

And company raising equity through right issue has nothing to do with these subsidiaries. It is for a capex which is planned for next year.

EnggRnD is a crowded space is an interesting view. The entire market size for india is going to tripple in next 5-7 years and targets to reach 100 bn USD size. There are multiple tailwinds here like

Technological advances (EV, ADAS etc.)

China +1 theme ( Yes China+1 is not just for chemicals)

Make in India - Especially segments like electronics, semi conductor etc.

Companies with capabilities and international collaborations to gain more from these tailwinds.

“ASM has over 2000+ Person years of experience in serving reputed Semiconductor Equipment Manufacturing Companies. ASM has the expertise and understanding of design and development of System and Sub Systems of PVD, CVD, RTP, Etch, CMP and Inspection tools”.

This is from the company website.

One of their major client is Applied materials, it is a semi conductor equipment manufacturing company based out at USA and having Indian operations. We have discussed few things about this company in this thread. Please see it.

So far forms gear contributed very very minimal revenue , ASM Digial (semcon ) contributing a bit

Being a such a small player not a focussed play, there are into everything (ofcourse they git into their service offering value chain )

There are investor presentation . earnings calls to understand more about the management guidance and the path that they have taken for the inorganic growth.

Sharing wealth is good but not cost effective, instead they should have used the money for growth instead of going for rights issue to raise further capital or triggered a tax efficient buy back.

No doubt they are into Industry 4.0 related stuff, IIOT, ERnd, Automotives , Networks and Security

Very hard to track each and very tiny thing that they are doing and on qoq basis…

I think things are turning around here, this quarter consolidated entity generated 2.5 cr ebitda for the first time. I feel RV forms and Asm digital has specialised niche and should do well from here from the very low base of the scale.

Example RV forms grown 100% yoy in FY 21 inspite of the covid lockdown of two months (it is a manufacturing company).

Too many things to handle for a smallcap company

Nothing to say on this.

Distributing Dividend without re-investing in company

Last 3 years he paid out 50-70% of profit as dividend and he aquired 2 companies and simultaneously took stake in few startups and initiated multiple collaborations. He has done all these things and revenue also became 2x meanwhile. If he is executing beautifully why should I complain about dividends.

No investor presentation or concalls

This is infact a negative I expect they will correct it in near future.