About

Incorporated in 1988, ASK Automotive Limited is a manufacturer of Advance Braking Systems for two-wheelers in India.[1]

Key Points

Market share [1] Ask Automotive is the largest manufacturer of brake-shoe and advanced braking (AB) systems for two-wheelers in India. The company had a market share of 50% in FY23 in terms of production volume for OEMs and the branded independent aftermarket (IAM)

Product Portfolio [2]

1) AB systems - 38% of Q1FY24 revenue

2) Aluminum lightweight precision (ALP) - 43%

3) Wheel Assembly - 13.5%

4) Safety control cables - 3.54%.

Manufacturing Facilities [3] As of June 2023, company has 15 manufacturing units spread across five states in India. The company commenced commercial manufacturing operations at its 16th manufacturing facility in Bhiwadi (Rajasthan) in July 2023. In addition, its Joint Venture operates one manufacturing facility in Gurugram, Haryana.

Clientelle [2] ASK Automotive supplies to Original Equipment Manufacturers like HMSI, HMCL, Suzuki, TVS, Yamaha, Bajaj, Royal Enfield, Denso, Magneti Marelli, and others. It also supplies in aftermarket and export market.

User Industries [2]

1) the automotive sector for 2Ws, three wheelers, passenger vehicles and commercial vehicles, and

2) the non-automotive sector for all-terrain vehicles (ATVs), power tools and outdoor equipment.

Technology Partners [3] The company has entered technology licensing arrangements with global companies such as:

1) A Japanese manufacturer of asbestos-free brake shoes supplying to 2W manufacturers globally;

2) NUCAP Industries Inc., Canada (NUCAP) – a global player in patented retention systems

3) Safety Control Cable Ind. Co- a SCC manufacturer serving automobile OEMs globally.

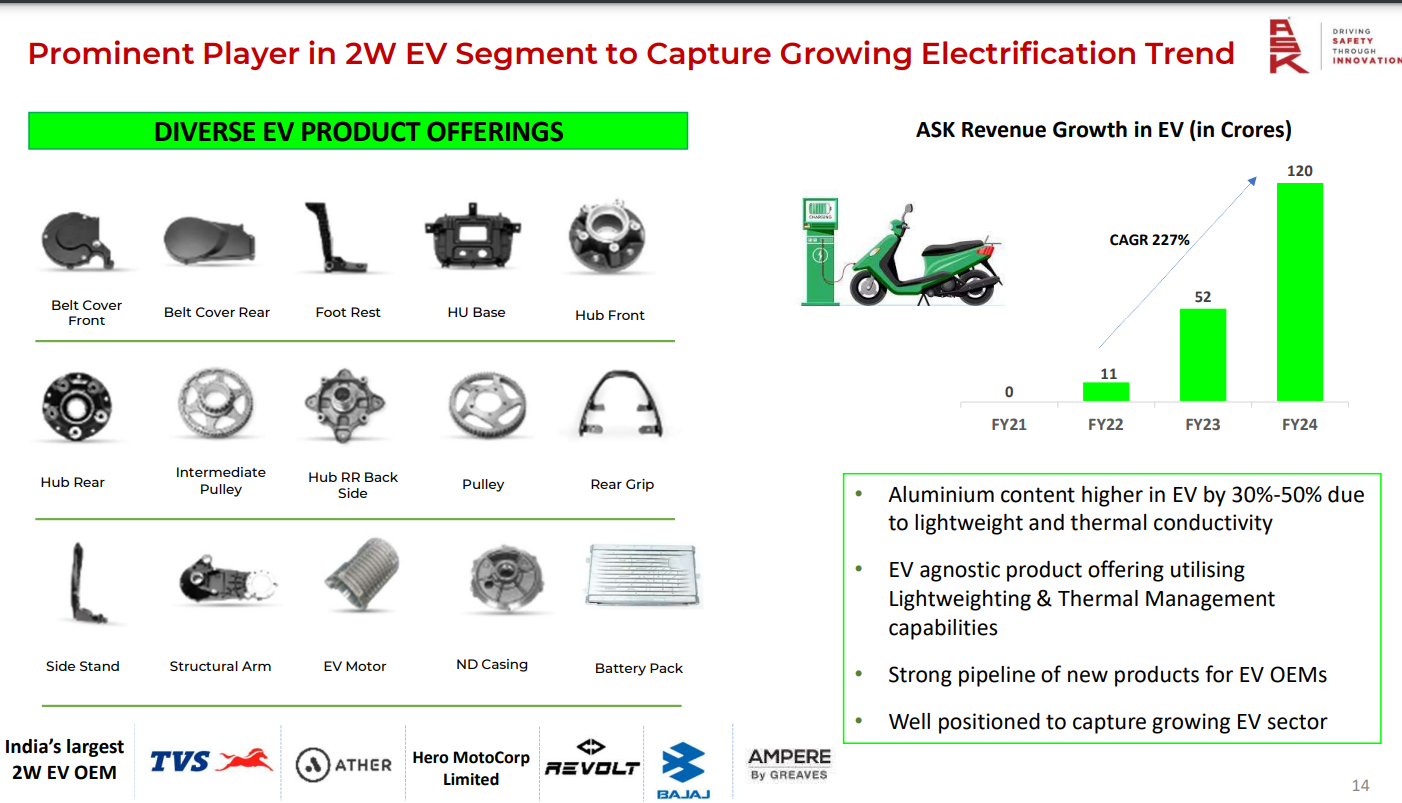

Focus on EV segment [4]

To leverage the expected growth in demand for 2W EVs, the company has 11 new programs under development for the EV sector that have been produced in Q2 FY24.

Revenue Concentration [5] The company derives more than 50% of its revenue from top three customers. It’s top Customer contributed 35% to FY23 revenues.

A significant portion of its revenue is attributable to the Indian two-wheeler automotive sector. In FY23, two-wheelers contributed 90.65% of its revenue.

IPO Details [6] Co. intends to raise 834 Crs through the IPO and the entire issue is an Offer for sale.

Their product portfolio :

Moreover they are expanding their foot print in EV segment as well and the growth in the EV is tremendous as we can see in their investor presentation.

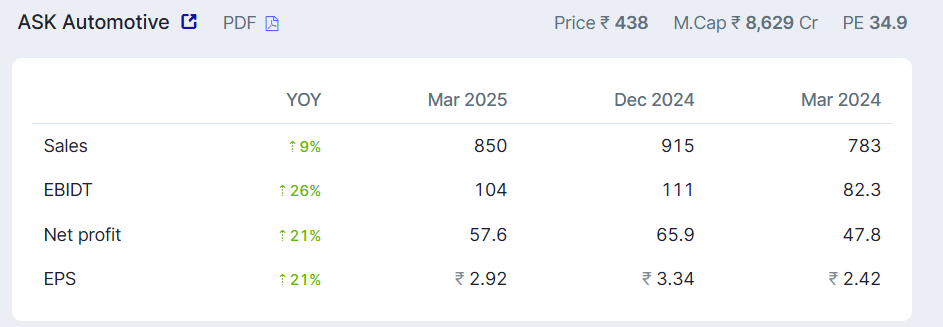

Some Key metrices

The PEG ratio is so high as it is recently listed company, which eventually will be re rated.

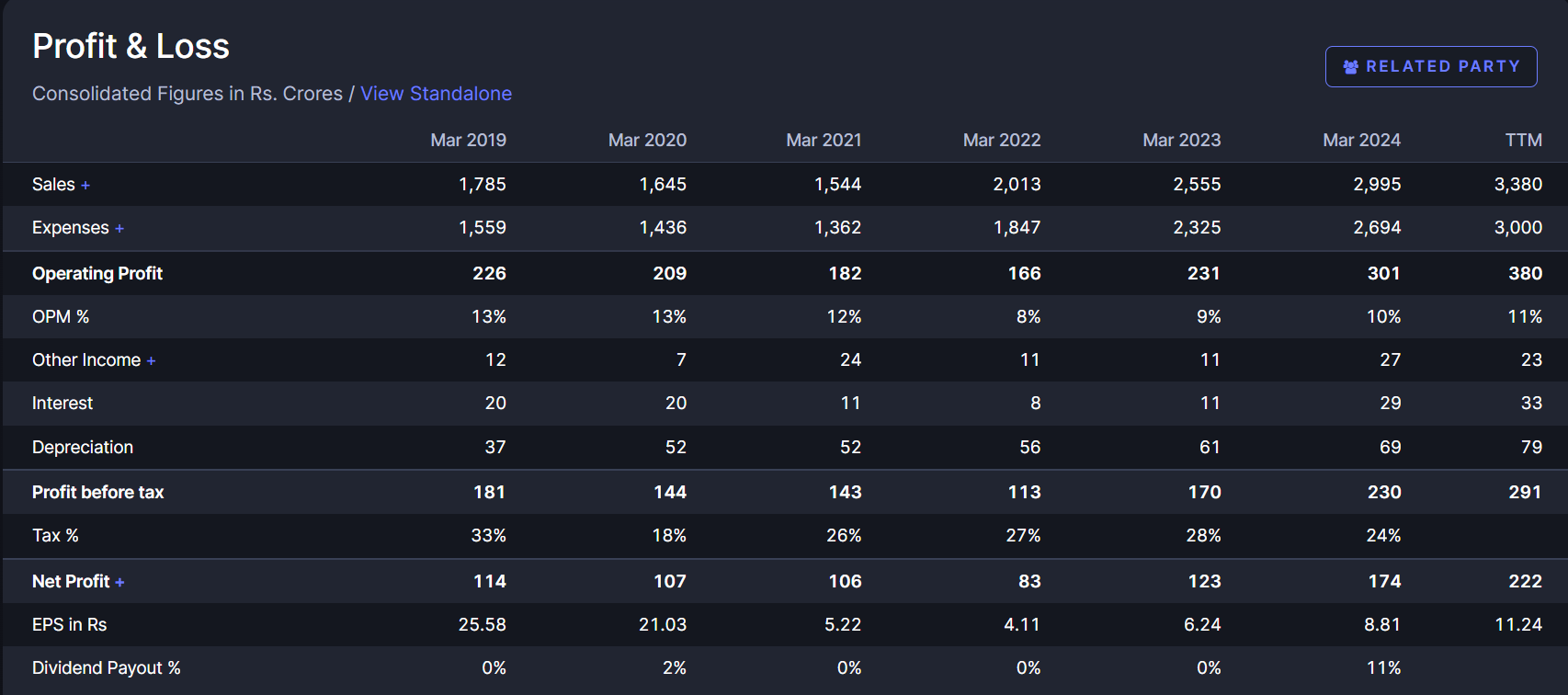

The company is seeking attention as it the largest player in 2W Advance breaking System which will lead to the pricing power and it will benefit the Margins. The margins are on a growing phase from past 3 years and I think it will improve more as the Automotive industry grows and their manufacturing plants run at their full pace.

The P&L statement is growing on a excellent pace with reporting their highest ever sales and profit.

The management is very much optimistic about increasing their exports in upcoming quarters. Since the economic slowdown in Europe and China dumping it has affected the exports of the company. But in upcoming quarters as the market reversal happens in Eurpoean market this will help Ask Automotive to grow their export market with growing margins.

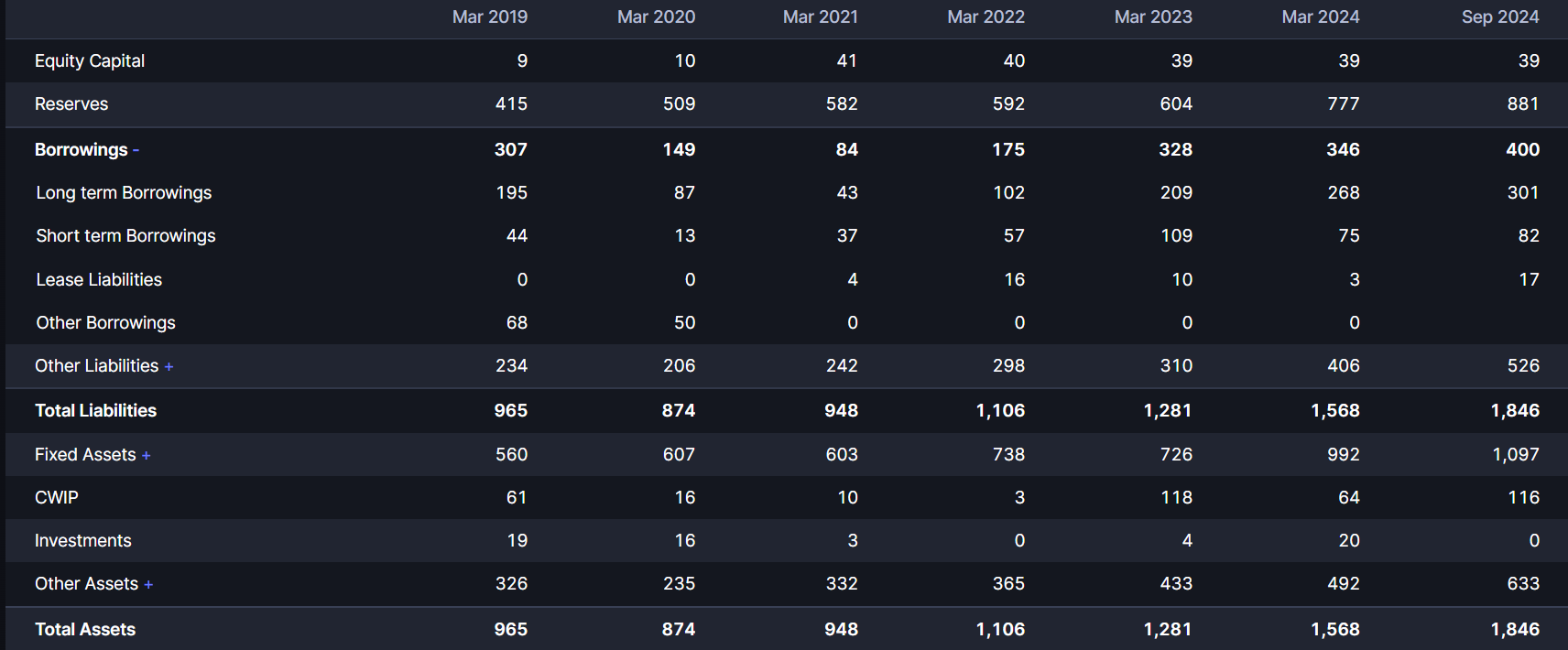

The borrowings are increasing which I think due to the CWIP as I can see Long Term Borrowing rise in their balance sheet.

Also the FII have taken a majority stake in this quarter and also DII have increased their stake all was offer for sale in the IPO as we can see:

In their recent concall they mentioned that the overall automotive grew at 9% in Q2 but TW grew at 12.5% which is great and being the majority player will help them a lot.

Concall Highlights Q2

Industry Overview:

- The automobile sector grew approximately 9% in Q2 FY25 compared to the same period last year, according to the SIAM report.

- The two-wheeler segment showed significant growth, with a 12.5% increase in Q2 FY25 and 15.8% in H1 FY25 year-on-year.

- Two-wheeler vehicle production reached 6.3 million in Q2 FY25, up from 5.6 million in Q2 FY24.

Financial Performance:

- ASK Automotive reported a revenue growth of 22% in Q2 FY25, with EBITDA increasing by 50% and PAT by 63% year-on-year.

- H1 FY25 results show a 26% revenue growth, 55% EBITDA growth, and 63% PAT growth compared to the same period last year.

- The company achieved the highest-ever absolute revenue and EBITDA in any quarter.

- EBITDA margins improved to 12.2% in Q2 FY25, 230 basis points higher than Q2 FY24.

Product Segment Performance:

- Advanced braking systems maintained market leadership with an 18% year-on-year growth.

- The aluminium light weighting precision solutions segment, which constitutes 45% of revenue, grew by 27%.

- Safety control cables also saw a healthy growth of 18%.

Capacity Expansion:

- The mega manufacturing facility at Karoli is expanding, with positive EBITDA margins now being generated.

- Construction of a new plant in Bengaluru is on schedule for operationalization in Q4 FY25.

- A solar power plant of 9.9 megawatts in Sirsa, Haryana, is nearing completion for captive consumption.

Future Outlook:

- Management is optimistic about maintaining growth momentum in the two-wheeler sector, especially during the festive season.

- The company aims to sustain EBITDA margins and gradually improve them in subsequent quarters.

New Developments:

- The alloy wheels business is progressing steadily, with the Bangalore plant expected to commence operations in Q4 FY25.

- Management is cautious about revenue expectations from the alloy wheel business, pending testing results.

- A new order worth over INR 75 crore is anticipated from Europe, expected to start in January next year.

Challenges:

- The export market, particularly in Europe, is facing demand issues due to inventory corrections by major customers.

- The commercial vehicle sector is underperforming, impacting the joint venture (JV) with FRAS-LE.

Margin Guidance:

- Management indicated that commodity price fluctuations are hedged, ensuring no adverse impact on margins.

- The Karoli plant has reached 45%-50% capacity utilization, contributing to improved margins.

Joint Ventures and Collaborations:

- The JV with AISIN Group is expected to commence operations in Q4 FY25, with a projected revenue potential of INR 100 crore to INR 150 crore per annum over the next three to five years.

Disc: These are just my views as this company got my eyes. Not invested but will look forward to invest if community helps to extract more information regarding Ask Automotive.