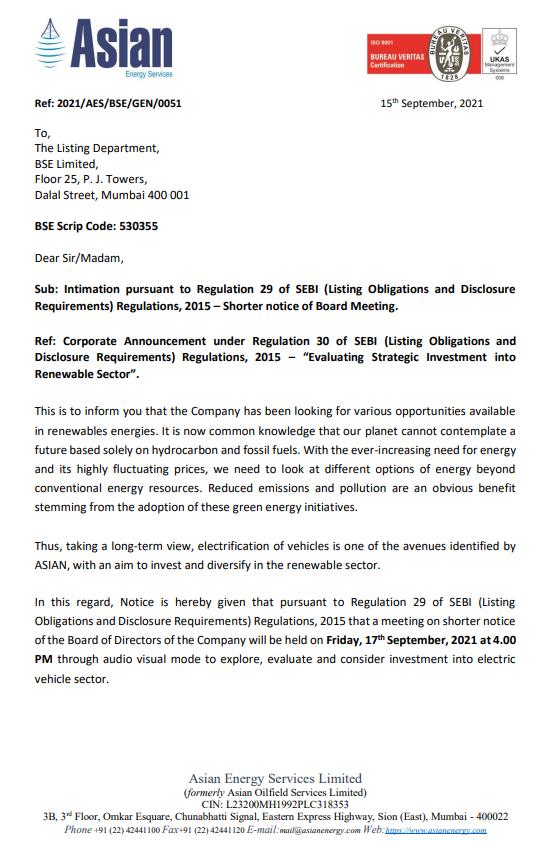

ASIAN had a very bad past with poor promoters, SEBI slapping a fine etc.

In FY 17 it was taken over by OILMAX and the turnaround is evident in the financials.

Company Analysis of last 10 years (Annual Report and Financials combined)

Mr. Gautam Gode is a Promoter Director of the Company and is also the director on Samara Indian Advisors Pvt. Ltd. Samara who fist invested in 2008, acquired a majority stake in Asian Oilfield and assumed management control from 2010 with 36.33% of shares.

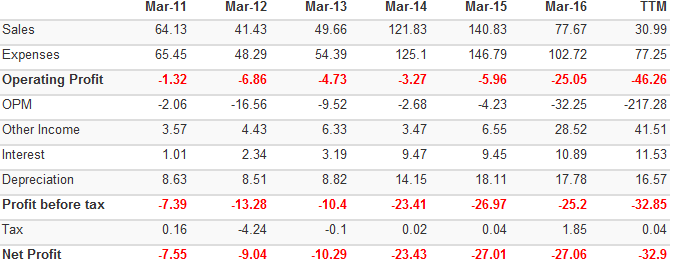

In FY 11, the company made considerable profits of Rs. 9.93 Cr v/s 3.39 cr the previous year, but almost 85% of this was wiped out due to “provisions for bad linter-corporate Loans” amounting to Rs. 7 Cr. That resulted in a net loss of approx. Rs. 7 cr. This is not considered good in terms of Management quality and intent.

From March 12 to March 17, the expenses were more than sales resulting in considerable losses every year. This indicates poor operations or orders taken at loss – both of which are not good management traits.

In FY 12, the company received only 2 orders that is indicated from low sales revenue. This year also saw a fall of crude oil process falling that impacted their order prospects. With low orders, company could not control expenses that stood at 115% of sales that resulted in considerable losses.

Sales were flat in FY13 at 49 Cr. This year, the company expanded to internationally. The management expected a top-line of 300Cr by 2016 – it was not even close at 78 Cr. The same factors resulted in poor order numbers. The same problem of Expenses being above sales existed, resulting in loss. The new management recruited last year doesn’t seem to work. Despite losses and poor performance, the salaries of key managerial executives increased 3 times from 42 lacs to 1.4 cr! Provision from intercorporate doubtful loan still exists in the books.

In FY 14, sales increased substantially from 49 cr to 122 cr. This is due to the new government focusing on Indian oil reserves exploration. However the expenses overshot revenues again resulting in losses. (Not Sure But looks like provision has been made to disappear; that is written off – sign of siphoning?). The company was fined 20 lacs by SEBI for not disclosing Samara taking up of shares in 2012.

In FY 15, the sales further increased to 140 cr but again the expenses overshot sales resulting in losses.

The same story of inefficiency despite good market and good orders continues till FY 17 when Oilmax took over Asian.

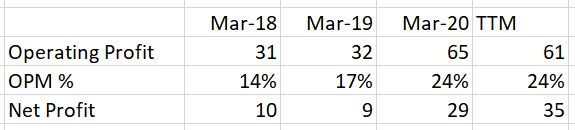

The new management has set out clear goals for strengthening the balance sheet and on cost control. This focus is heartening.

The management has a record of good consistent delivery without major delays. No penalties have been levied on the company. No fishy transactions or doubtful loans.

The result of excellent management is seen in the financial numbers post FY 17. This is the proof of pudding.

Attached is the full analysis

@bhaskarbora67, I have moved it here since this already existed. I’ll send comparison with alphabet shortly

Asian Oil Fields My Analysis_Version 5.00.pdf (165.8 KB)