Asian Hotels East owns the Hyatt Regency in Chennai and Kolkata . They have a case going on for allocation of land of 9000+ sq. metres in Juhu in Mumbai and they also own a free hold land in Orissa (Bhubaneshwar) for developing a luxury property there. These are shown at a book value of around 25 Cr but must definitely worth a lot more.

CMP : 280

Market Cap : 330 Cr, Consolidated Debt : ~ 120 Cr

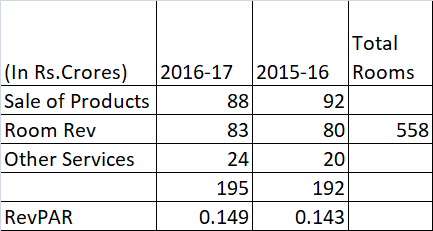

Annual Sales (Consolidated) : ~ 190 cr ( approx 50% each from the Chennai and Kolkata properties)

Total Rooms (5 Star category) - 233 (kolkata)+ 325 (chennai) = 558

Total Revenue - 190 Cr

Occupancy - 69%

Average cash flow from operating activity is over 35 Cr for last 3 years. Only because of high depreciation (30 Cr), the PAT looks low. One way to look at it is that the money was not well invested in the past - as return on investment is not great. Balance sheet size is ~ 1000 Cr (125 Cr is goodwill on consolidation though) , but market cap is only 330 Cr.

The operating cash flow can explode once the occupancy goes beyond 70% especially in Chennai

Potential triggers : Last Dec quarter there was disruption in the Chennai operations due to floods and last few quarters there was a drop in revenues due to the liquor ban. Inspite of this Revenue from rooms has improved .

I also had a couple of questions –

Does anyone know about current status of the liquor ban?

The room rate at both the hotels is below 7500 on the internet . However the GST rate levied is 28%. Can anyone explain this?

Risks :

Stock is illiquid and it will take time for a large investor to build a meaningful position.

Properties are in only 2 cities Chennai and Kolkata. Kolkata is getting a lot of new hotels starting this FY so prices/ occupancy will be under pressure

GST is charged on tariff rate. Eg. tariff rate 10,000/- and hotel giving the room at discounted price say 6000/- then gst will @ 28% on 6000/-. If tariff is say 7000/- and and hotel giving room at 5000/- then gst will be @ 18%.

Firstly thanks a lot for this finding . Let me add couple of point here.

Hyatt regency is a very established brand name in Kolkata . But I wonder why last few years of business haven’t taken off that much speed. We might need to look a lot deep insight into their operational process.

Hotels coming up in Kolkata is definitely a threat but the business opportunity has started to unwrap due a lot of govt initiative. Moreover the location of this hotel is in a very sweet spot. On the very EM bypass which directly connecting VIL road towards Airport within 20 mins. Also connecting Newtown/Rajarhat industrial area in a reachable distance of 15 mins.

Over the years we see growth of TAJ hotel in Kolkata mainly due to their contact with BCCI the same we have witnessed with ITC with their IPL tie-ups. We haven’t seen any such contract with Hyatt untill recently when the U-17 WC Football team stays their and mainly due to it’s adjacent YuavaBharati stadium. And we have also seen this kind of tournament’s coming up in near future. If it’s get’s a contract from ISL then it will be a great growth prospect for them. Also India is bidding for U-19 WC and Kolkata is having only one ground i.e. YuavaBharati of international stature which is just beside this Hotel we can expect a lot of new contracts which leads to the increase of occupancy.

No liquor ban in Kolkata yet.

It will be good if anyone can give some insight about the Chennai hotel as well. Also is there any management commentary details available about their recent operational inefficiency ? And their next plan of improvement.

Chennai F&B revenues plus room revenues should definitely improve in Dec quarter then.

Lets see if the Kolkata market sustains or has benefited from the FIFA U17 world cup also. Kolkata will definitely be under pressure with opening of new hotels.

List of Top Ten Shareholders other than Promoters and Directors is not available in Annual Report.

Company has substantial investment in subsidiaries and they are reporting consolidated loss since last four years. Pls share about working of their subsidiaries if anyone has any idea.

Asian Hotels East Ltd. FY18 Annual Report Notes

Kolkata hotel of the company did very well during the year and showed improvement in both sales and profitability. Chennai hotel performed very poorly with sales declining by 10% and a loss of Rs. 20 cr. approx which was mainly due to depreciation, hotel was cash surplus during the year. With Mcap of Rs. 315 cr., loan of 137 cr. and cash & liquid investments of Rs. 81 cr. company has an EV (Enterprise Value) of Rs. 371 cr. Valuations of the company looks cheap considering the cash flows and the book value of the company. Following are the highlights from Annual Report 2018.

Standalone Sales from Rooms = 43.82% and Food = 48.23%. Total sales = Rs. 102 cr.

Consolidated Sales from Rooms = 45.72% and Food = 44.44%. Total sales = Rs. 189 cr.

Room Keys: Kolkata = 246 and Chennai = 325. Total = 571 keys.

Capital Investment in GJS = Rs. 234.63 cr, Robust = Rs. 91 cr. and Regency = 25.79 cr.

Loan to GJS = 322 cr., Robust = 22 cr.

During the financial year 2017-18, Hyatt Regency Kolkata (the hotel) has been successful in securing major project-based business and could sustain its leading position in wedding related business in the city. As weddings prop up revenue, the hotel has been nearly successful in booking all the relevant wedding dates during the last year.

With reference to 100% subsidiary GJS Hotels Limited, the Company is awaiting sanction of drawings submitted to the Bhubaneswar Municipal Corporation and continues to engage in dialogue with the Government of Odisha for extension of time to start construction and complete the hotel project at the site.

As on date, the Company holds 91,652 Equity shares of Rs 10 each of its subsidiaries, Regency Convention Centre and Hotels Limited (RCC), representing 58.99% of the paid up capital of RCC. Principal assets of Regency Convention Centre and Hotels Limited (RCC) comprise of an interest in a piece of land near CSI Airport at Mumbai. The RCC has filed Suit No. 6846 of 1999 in the High Court of Judicature at Bombay against the Airports Authority of India (AAI) & Ors. for specific performance of the agreement to lease 31,000 sq.mtrs. of land at village-Sahar, Andheri (East), Mumbai in its favour for construction of a five star hotel cum convention centre.Deposit with high court Rs. 15 cr. We continue to engage in dialogues with the parties concerned and has been exploring opportunities to settle the disputes amicably. Your Board is hopeful of a positive outcome.

Your 100% subsidiary, Robust Hotels Private Limited (Chennai) was adversely affected during the period commencing from April, 2017 till August, 2017 due to reasons beyond the control of the management. The reasons include : liquor ban imposed by state government, delay in completion of metro rail work in front of the hotel and adverse market condition. In spite of the above, Hyatt Regency Chennai (Robust) managed to keep the Rev PAR at the same level as in the previous year 2016-17.During the financial year under review, the turnover was Rs. 88.43 crores as compared to 98.74 crores in the previous year and EBDITA was Rs. 22.07 crores as compared to Rs. 26.09 crores in the previous year. Your directors are hopeful of better performance of Robust in the current financial year.

Industry saw 1.4% occupancy growth over 2016, ADR grew 1.6% leading to 3.8% growth in Revpar (Revenue per available room).

This was mainly due to strong inbound traffic which crossed 10 million foreign arrivals, increase in GDP in the 3rd quarter with stable inflation growth leading to increase in money supply, which will also fuel the growth for 2018-19 estimated to be around 7.4% (in GDP) and also Kolkata being the FIFA headquarter city for u-17 FIFA world cup during Q4.

Opening of Biswa Bangla Art Convention Centre will attract large international conferences. Increased room and banquet demand will be supplemented by full swing opening of other competitor hotels. As a result, future market will be highly competitive.

In spite of the mishappenings in the year 2017 in Chennai, Robust Hotel witnessed an occupancy growth of 4.3% in the year 2017-18 accompanied by a minor increase of 0.4% in ARR. Occupancy rate was 69% in FY17 so occupancy rate for FY18 works out to be 72% which is quite good.

The Union Consumer Affairs Ministry’s guideline prohibiting the compulsory service charge also had an impact to the economic activity of the hotel.

Further, during the financial year 2017-18, discontinuation of duty free license has directly impacted margins by increasing the landing cost to the Company. Exorbitant increase of annual liquor license fees have also impacted the GOP.

Contingent Liability of Rs. 160 cr. as corporate guarantee for Robust Hotels Private Limited.

Asian Hotels has entered into a loan agreement with Kotak Mahindra Investments Limited

They’ve recently borrowed money, up to Rs. 500 crores, from Kotak Mahindra Investments Limited to purchase hotel assets.

The company has entered into a loan agreement with Kotak Mahindra Investments Limited, and they’ve provided details of the agreement in an attached document called “Annexure-A.”

The loan amount is Rs. 210 crores, and the agreement includes some terms and conditions related to the loan and the purchase of hotel assets.