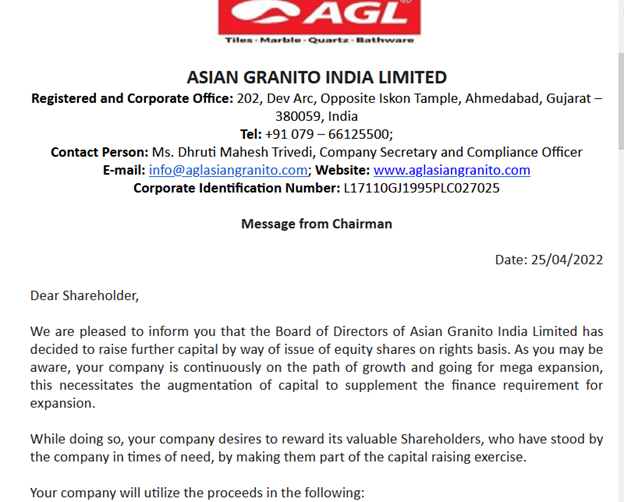

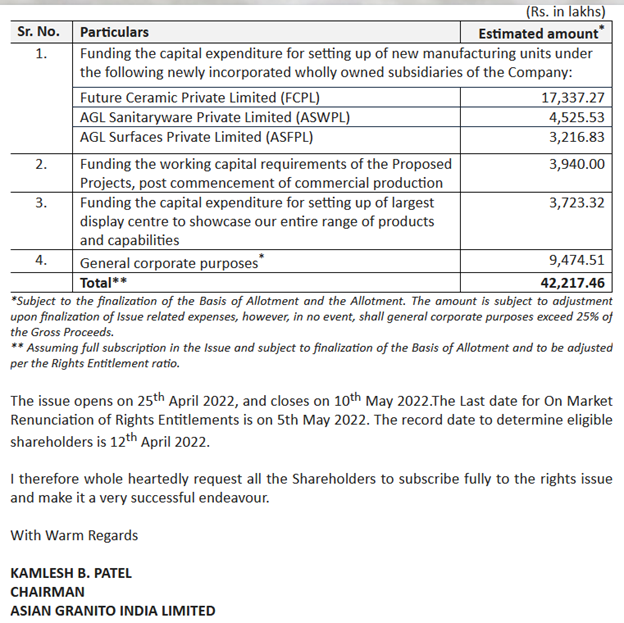

AGL’s rights issue (redux!) opened today, and thanks to all the antics and tricks pulled by promoters in the last 1 year, the issue was locked in lower circuit through the day.

Today (April 25th) evening the chairman sends a note exhorting shareholders to subscribe to the issue:

Does anyone know what happens when a rights issue falls through – what happens to those shareholders who didn’t sell their rights and wanted to subscribe.

Disc.: invested and negatively biased

Any updates on what happened after IT raids finished?

I have some small number of shares of Asian Granito and so track it once in a while. It has been almost 2 months since raid was done and there is not initiation from company nor IT dept has made any statement. such things can happen only in India !!

Siphoned funds being shown as losses now. 60 crore loss!!! Like it’s even possible. Sebi sleeping like always.

5F0D5866_6F32_4160_8C65_0EB161859966_150223.pdf (379.7 KB)

Any views on how this can shape up

Negative news I guess but doesnt really matter, there was 0 chance of a hostile takeover by Kajaria once Asian granito promoters succeded with the controversial preferential issue.

Asian granito promoters are fraud, there is no doubt regarding that. The company would be 3-4x in hands of any other promoter.

Disclosure: No Position

Any update further for company

Can anyone make sense of what financial acrobatics are happening as part of this restructuring? To me the promoters look more like investment bankers than tile makers in pulling off something as complex as this.

The restructuring of Asian Granito India Limited (AGIL) involves a series of complex transactions aimed at consolidating various private entities under the umbrella of the listed company. While the stated rationale for this move includes operational efficiencies and growth opportunities, the details of the transaction raise questions about the potential benefits for public shareholders. Let’s break down the financial acrobatics involved:

● Demergers and Mergers: Scheme I of the restructuring involves demerging tile manufacturing undertakings of three privately held companies (Affil Vitrified Private Limited, Ivanta Ceramics Industries Private Limited, and Crystal Ceramic Industries Limited) into separate wholly-owned subsidiaries of AGIL. Additionally, AGL Industries Limited, an existing subsidiary of AGIL, will be merged into another wholly-owned subsidiary, Amazoone Ceramics Limited.

● Slump Sale: The Marbles & Quartz Division of AGIL will be sold to Amazoone Ceramics Limited via a slump sale.

● Share Swap and Cash Consideration: The demergers involve complex share swap ratios, resulting in the issuance of new AGIL shares to the shareholders of the demerged companies. The slump sale, on the other hand, will be settled through cash consideration of Rs. 102 Crores.

● Impact on Share Capital and Ownership: The restructuring will more than double AGIL’s paid-up share capital. This will significantly dilute the existing public shareholding from 66.47% to 32.97%, while the promoter’s stake will increase from 33.52% to 44.32%.

The complexity of these transactions, involving multiple entities, share swaps, and cash considerations, does lend credence to the view that the promoters are engaging in sophisticated financial manoeuvring.

_________________________________________________________________________

Here’s why this raises concerns:

● Dilution of Public Shareholding: The significant dilution of public shareholding raises concerns about the potential loss of value for existing shareholders. While they will receive new AGIL shares, the increased share capital could potentially lead to a decrease in earnings per share (EPS) and return on capital employed (ROCE).

● Lack of Clarity on Financial Performance: The sources indicate that the private entities being consolidated are currently not profitable or are generating only meager profits. The lack of detailed financial information makes it difficult to assess the true impact of these entities on AGIL’s overall financial performance post-restructuring.

● Potential for Related Party Transactions: Although one of the stated objectives of the restructuring is to avoid related party transactions, the fact that the promoters will have a controlling stake in the consolidated entity raises concerns about the potential for future related party dealings.

In conclusion, while the promoters may argue that the restructuring is aimed at creating a larger and more efficient entity, the intricate financial maneuvers involved, coupled with the lack of transparency regarding the financial performance of the private entities, warrants skepticism. The significant dilution of public shareholding and the potential for future related party transactions raise valid concerns about the true beneficiaries of this restructuring.

For further deep dive: https://notebooklm.google.com/notebook/446b0262-30df-4479-ba43-ddfb7b613078/audio

Also keep a watch as timings of such news tends to come at the time where bigger institution wants to kick out small retailers ![]()

Accumulation Phase:

Note: This is not a recommendation, just my personal viewpoint. I may be incorrect.

Total Valuation of AVPL:

From the previous calculation, the valuation of AVPL is approximately ₹9.16 crore based on the EBITDA multiple approach for FY2023 at 4X EBITDA.

Here’s the breakdown:

Given:

- Swap ratio from the earlier part of the conversation: 1 AGL share = 1.52 AVPL shares

- AGL Market Capitalization: ₹711.67 crore

- AVPL Valuation: ₹9.16 crore

1. Calculate the Total Value of AVPL:

As discussed, AVPL’s value is ₹9.16 crore.

2. Number of AGL Shares for AVPL:

We need to calculate how many AGL shares AVPL will receive in exchange for its value of ₹9.16 crore. Since 1 AGL share = 1.52 AVPL shares, we need to find the equivalent number of AGL shares that AVPL will receive based on the swap ratio.

First, we need to find out how many shares of AVPL correspond to ₹9.16 crore:

Number of AVPL Shares=AVPL ValuationPrice of AVPL Share\text{Number of AVPL Shares} = \frac{\text{AVPL Valuation}}{\text{Price of AVPL Share}}

If the price of AVPL shares is taken as ₹5 (from the previous calculations), the number of AVPL shares will be:

Number of AVPL Shares=9.16 crore5=1.832 crore shares of AVPL\text{Number of AVPL Shares} = \frac{9.16, \text{crore}}{5} = 1.832, \text{crore shares of AVPL}

Now, since 1 AGL share is equivalent to 1.52 AVPL shares, we can calculate the number of AGL shares that AVPL will receive:

Number of AGL Shares for AVPL=1.832 crore1.52=1.204 crore shares of AGL\text{Number of AGL Shares for AVPL} = \frac{1.832, \text{crore}}{1.52} = 1.204, \text{crore shares of AGL}

3. Find the Price of AGL Shares:

Now, let’s calculate the price of AGL shares at which this swap occurs. The total value of AVPL’s AGL shares would be ₹9.16 crore. Using the total number of shares AVPL would receive (1.204 crore), we can determine the price per AGL share:

Price per AGL Share=AVPL ValuationNumber of AGL Shares for AVPL=9.16 crore1.204 crore=₹7.61 per AGL share\text{Price per AGL Share} = \frac{\text{AVPL Valuation}}{\text{Number of AGL Shares for AVPL}} = \frac{9.16, \text{crore}}{1.204, \text{crore}} = ₹7.61 , \text{per AGL share}

Conclusion:

At a swap ratio of 1 AGL share = 1.52 AVPL shares, AVPL would receive AGL shares at an approximate price of ₹7.61 per share.

This is a simplified estimation based on the swap ratio and available data. The actual share price of AGL in the market (₹70) is much higher, which suggests that the market may value AVPL at a much lower rate, possibly reflecting the financial challenges and valuation difference between the two entities.

Correct me if I am wrong

The number of frauds agl promoters have done lolll. They seems to be addicted to making money through this way. 2 Rights issue diluting company to 4x. Pocketing all the money and now this loll

AGL received a 67 crore tax notice (FY 16 to FY 20)!! Certain expenses have been disallowed. They certainly show many fake expenses.

Now just consider this hypothetically!!

The company earns 300 crore.

Now consider

Scenerio A : No Fraud, 30 percent tax (old tax), 90 crore tax, 210 crore for shareholders.

Scenerio B:

Shows 150 crores in fake expenses (diverted to promoters!). Promoters earn 150 crore. Company earns about (105 crore, 45 crore tax).

ITR dept flags this, applies penalty and asks for 67 crore of taxes for this.

End result → Shareholders earn 38 crore (instead of 210), promoters make 150 cr doing nothing!!

And ofcourse ITR dept got it dues, so they arent gonna gruel the promoters!! Everyone happy…

An analysis by chatgpt deep research

Asian Granito Fraud.pdf (614.9 KB)

@Shubham_Jain1 Nice work! I’m assuming this is deep research? What prompt did you use and how did you feesd it all the older data?