Looking all the action closely, I would be happy if they do it via QIP or PI mode rather than issuing Rights to existing shareholders. QIP/PI shall induce some interest. Not to say, Debentures/ bonds not good at all. QIP/PI if comes, shall be priced atleast 5% to 10% discount to CMP. Rest lies in future, lets see.

2 Likes

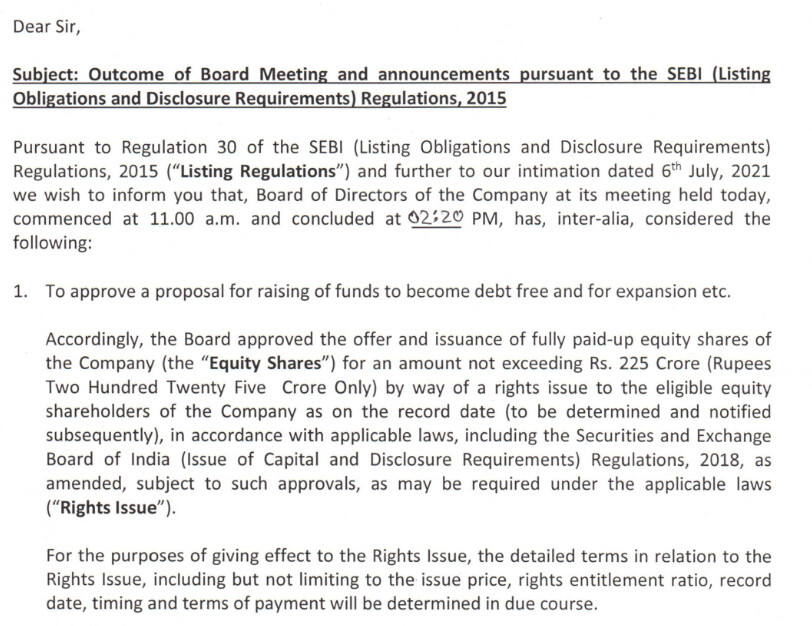

Rights issue by AGL – it’s never a dull day if you are invested in this stock.

Requesting seasoned boarders @Vineetjain111 @kalidasa @vikas_sinha to share their point-of-view:

++

4 Likes

Good line of questioning (very rare) from CNBC to company’s rep.

Grilled and burnt ![]()

7 Likes

One more interview from CFO

3 Likes

A few new takeaways from this interviews are

- Promoters will participate fully at the rights issue

- AGL have started meetings with fund houses advertising the rights issue

- The price for the right issue could be a lucrative one

- CFO openly admits the share price being lower than its right potential and suggests adding on stocks for long term. He called this stock as “long term horse”

Disc: I have been an investor since 2018 and continue to stay put

2 Likes

Investor Presentation for Rights issue

Recording of analyst meet held today (7th Sept)

Key points I noted:

- Promoters will fully subscribe the rights issue

- Tiles capacity will double from 1L sqmt to 2L sqmt in the next two years (largely through JVs/trading)

- Revenue to hit ~2000 Cr by end of FY23 (double digit revenue growth expected both in current FY and next FY)

- AGL has applied for re-rating already and will further will apply for re-rating after debt reduction later this year

- As a parting shot Kamlesh Patel said that by 2023 promoters’ stake will be 51%

2 Likes

Not interested in this company yet giving my view…

why they are showing lots of ad at moneycontrol.com? it seems to me they trying to boost stock price. red sign

5 Likes

They’ve been doing ads on CNBC as well for a long time. I think it’s reasonably well established that the promotors a bit shady, and so I don’t have a lot of faith in their claims of increasing shareholding.

The business however is likely to do well given the tailwinds in the sector, despite the promotors. I foresee margin expansion as well, so long as the promotors don’t tamper with the business. AGL is dirt cheap on every parameter, and if the promotors do live up to these promises, the retrating can be swift and sharp. Risk reward is for everyone to figure for themselves.

Disclosure: I had bought it in the 180s a few months back and sold out in a month with minor profits as I was uncomfortable with their shenanigans.

3 Likes

Yeah, even it got my attention bcz of their cheap valuation but dont want to put my money in any clearly visible shady companies… That’s how people ignore the signs in DHFL, Yes Bank and many other companies.

Wrote in June itself that company report is not good from internal sources, STAY AWAY was clear message. Now I am not even tracking this Company. Do not believe in what management say. Let them do it on ground then only invest. If Promoters increases stake to 51% , shall track again.

2 Likes

My guess is that most investors missed the following information contained in the last paragraph of a recent press release by the company:

There were some misconception posts the promoters holding coming down.The Company also wishes to clarify that Promoters are holding around 26.12%, and they will continue to hold at this level. The promoters will increase holdings when the situation demands. The promoters are also infusing funds by subscribing to the rights issue in their entitlements. The promoters sold some stake in the month May 2021, the funds of which were used by the promoter’s family in a Greenfield project called Adicon Ceramica LLP which will be manufacturing Large Format GVT tiles and AGL will be promoting that product in AGL brand on a substantial scale. This will be one of the unique plant in India, which will manufacture product which can generate heavy demand in the market. There are only few plants of similar type of products in Morbi, Gujarat. The production of the Adicon Ceramica LLP will start from July 2022. In Adicon Ceramica LLP, none of our promoters have any holding however, their family members have LLP holdings.

This seems to be a case of promoters milking the company in the following ways:

- A new Adicon Ceramica LLP held by the family of the promoters will use the AGL brand to sell its products. AGL itself has no holding in this LLP. Profit sharing between the two entities is anyone’s guess.

- Using company funds for share-market related advertisements. No idea how these make any sense. I mean who invests based on advertisements by the investable company itself?

The company is pretty transparent about how the promoters are going to milk the company for their own gains.

Disclosure: Tracking position.

15 Likes

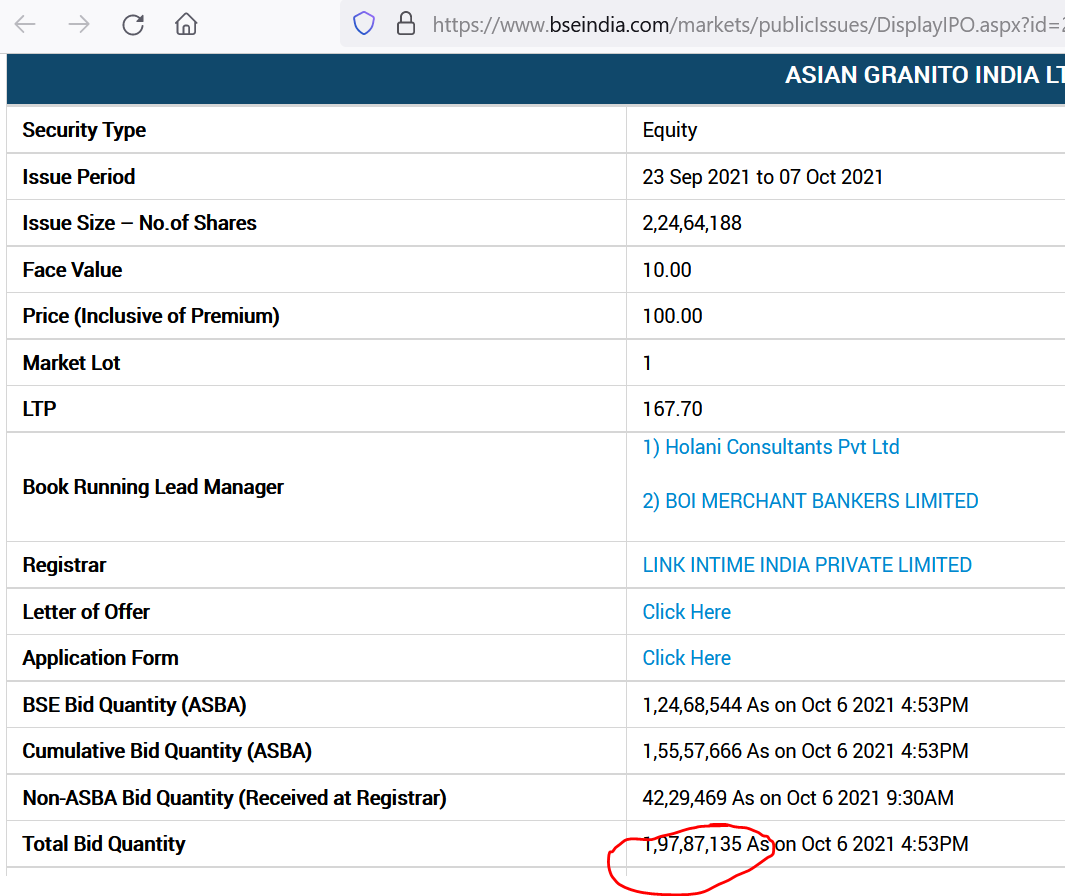

Rights Issue is ~90% subscribed with one more day to go.

3 Likes

Listing of new shares on 21-Oct-21.

https://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20211020-42

1 Like

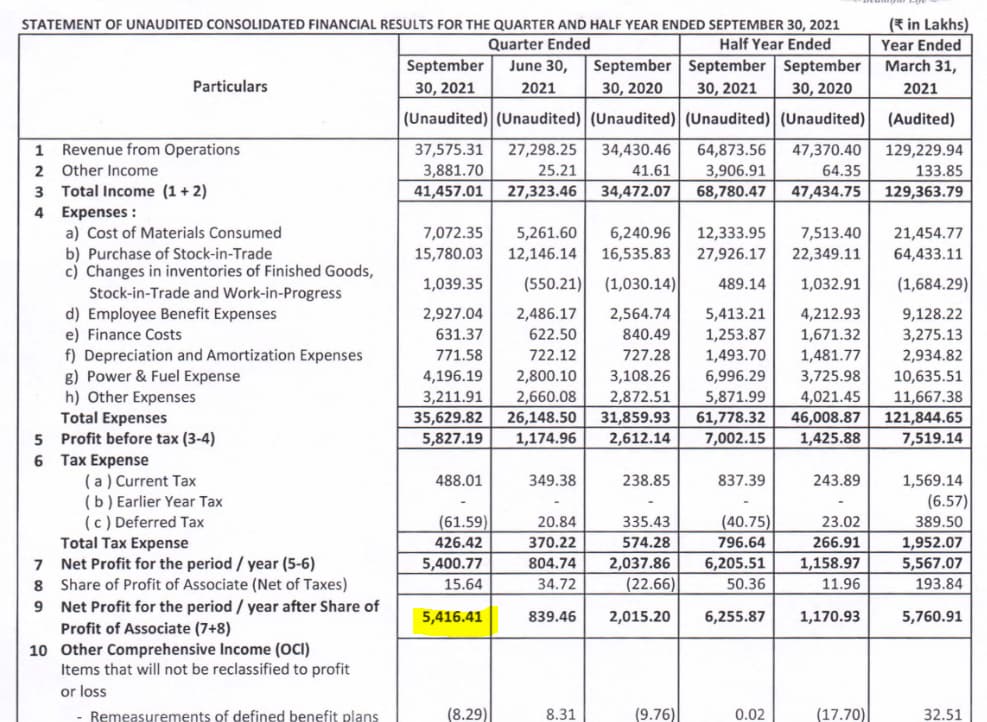

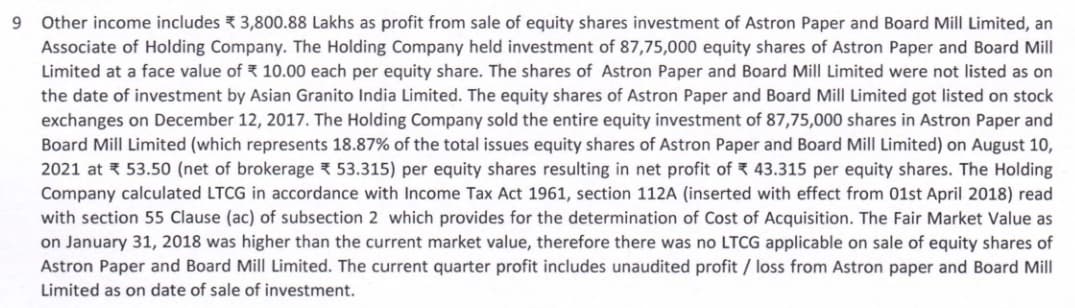

Q2FY22 results are looking ballistic primarily because of one-time sale of Astron Paper;

ex-Astron Paper-sale PAT should be ~16 Cr which is not that great.

Disc.: invested

4 Likes

Probably they must have gotten hit due to both lower exports (freight issues) and high gas prices. Revenue growth hints that tiles volume growth may have been tepid since the whole industry has been taking price hikes.

1 Like

1 Like

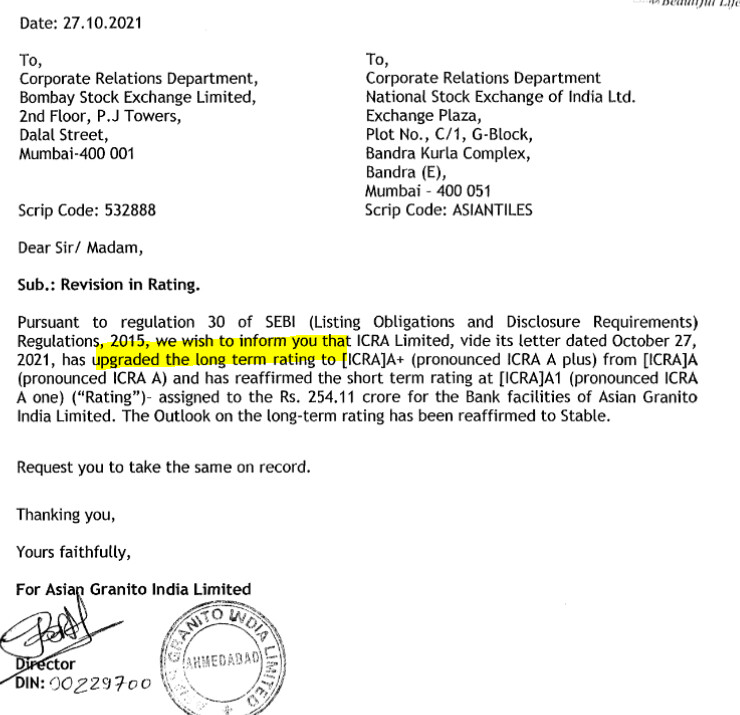

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=cda10c8f-24e9-48ce-87ea-c7cd57109e17

AGL raising another 500 cr via a fresh rights issue.

This looks strange for two reasons;

- They raised 224 cr via rights in Oct 2021 and that was supposed to be it

- Raising 500 cr when your mcap is 690 cr sounds preposterous

I have badly burnt my fingers in this stock; promoters have been upto one trick after another for the last one year.

On papers everything looks rosy. I have talked to multiple dealers and architects who also gave a positive review.

The big lesson I’ve learnt is: if something looks too good to be true then it probably is.

10 Likes

AGL promises that as an investor you will never have a dull day. AGL has incorporated three wholly owned subsidiaries in the last three weeks…and there is no communication from the management around this.

13-JAN-22: AGL SURFACES PRIVATE LIMITED

03-FEB-22: FUTURE CERAMIC PRIVATE LIMITED

07-FEB-22: AGL SANITARYWARE PRIVATE LIMITED

2 Likes