Thaks for your response @Apurva_Dubey. A follow up question:

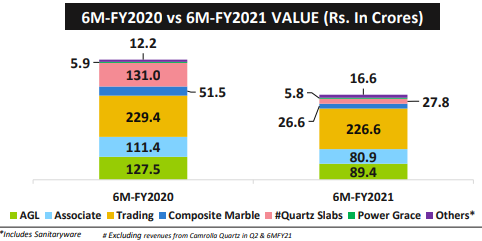

Below is a pic from the same presentation (a similar chart is available in Q4 presentation as well). This has revenues across AGL, Associate, Trading, Composite Marble, Quartz Slabs, Power Grace and Others. My guess was that Associates and Trading may form a large part of the outsourcing business and together that form a nearly 75% of the total business.

Can you help with what this figure actualy means? It doesn;t make much sense to me.

Yes in the Q3 concall someone asked about difference in EBIT between outsourced and self manufactured business and I think the management said they don’t have the figures handy. This is very important for us to know though as you correctly mentioned that asset light oursourcing will be the future for AGL and so the margin profile of this channel will decide the trajectory of overall margins.

If this is margin accretive, then we are looking at topline growth with margin expansion, which can be a very powerful rerating trigger. On the other hand if this is margin destructive, then there may be growth at lower margins - a value trap!

I think this, along with the receivables management are the key considerations for me here. Rest seems like noise.

@Vineetjain111 – that’s a very good observation and question that I don’t have an answer for. I went through the AR and didn’t find anything substantial to clarify this. Will write to Mr. Kalpesh Thanki for an answer -

It seems the competitors are also moving towards the outsourcing model. There is not much of a choice.

Will have to ask the company whether they have the information handy now.

Margin depends on the price they negotiate with their manufacturing partners, now and later on. Lower margins in the near term is not necessarily bad. Many companies work with low margins in order to maximize their cash flow in the long term.

Financial metrics as a whole (in particular the debtor days as you said) need to be improved. If they can generate higher return on capital, they can pay off their debt faster.

How do people usually play against operator manipulations in micro cap stocks? I think this stock is being subjected to price manipulation through short selling.

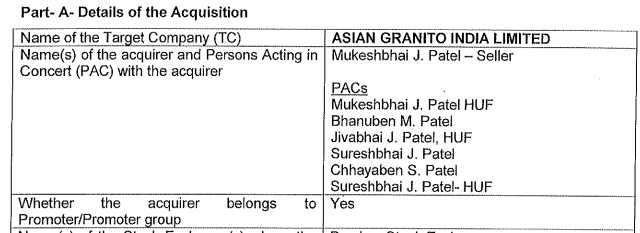

@Bihari_Lal_Pandey yes, even I want to know, can some one please help, and SureshBhai Jivabhai Patel is on the board of AGL why is he shorting the stock(I am not concerned of selling)

, and they are wasting company’s money by advertising in CNBC saying great results(not of products), I am not getting anything, weirdest investment i have ever made

Invested since April

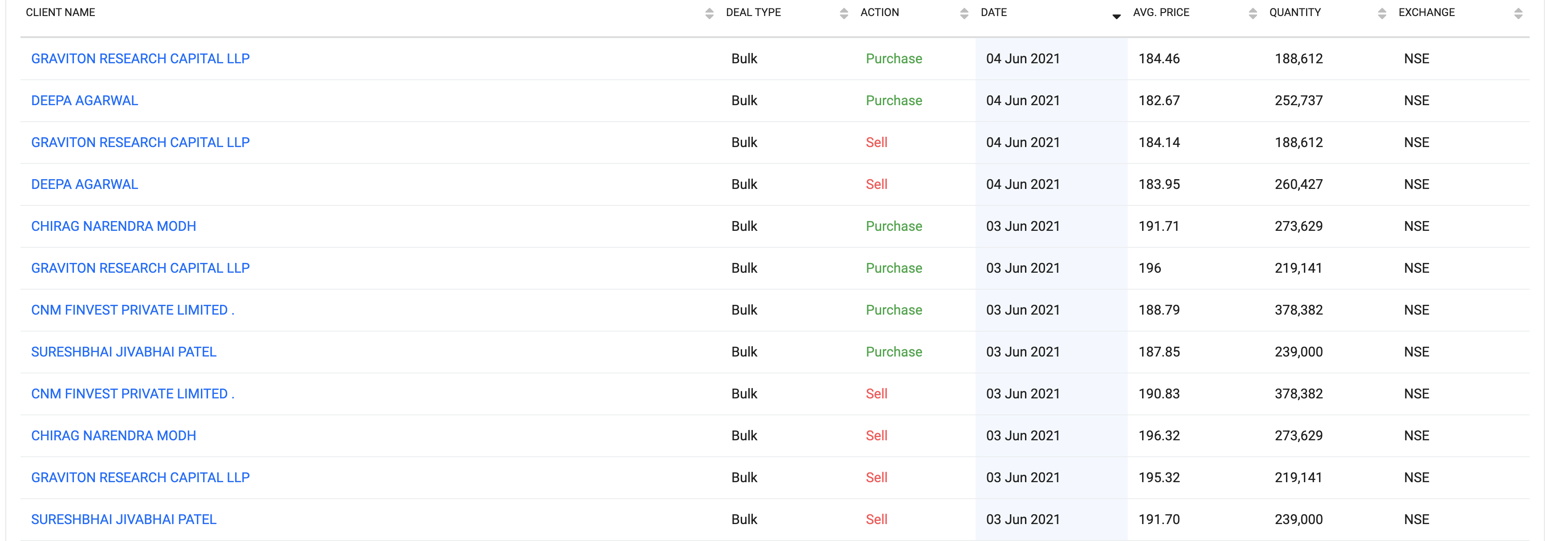

So apparently Suresh J Patel did some short selling of share (239000 shares) on 3rd June.

And actually sold shares on 4th June along with chhayaben patel.

This creates a bit of confusion if he wanted to dispose shares why didn’t he simply did it on 3rd June when it was getting a higher price. Does this mean he is expecting the price to drop further and add some. Would like to hear other thoughts.

In my view company is surely cheap when compared to it’s peers so downside should be limited in long term.

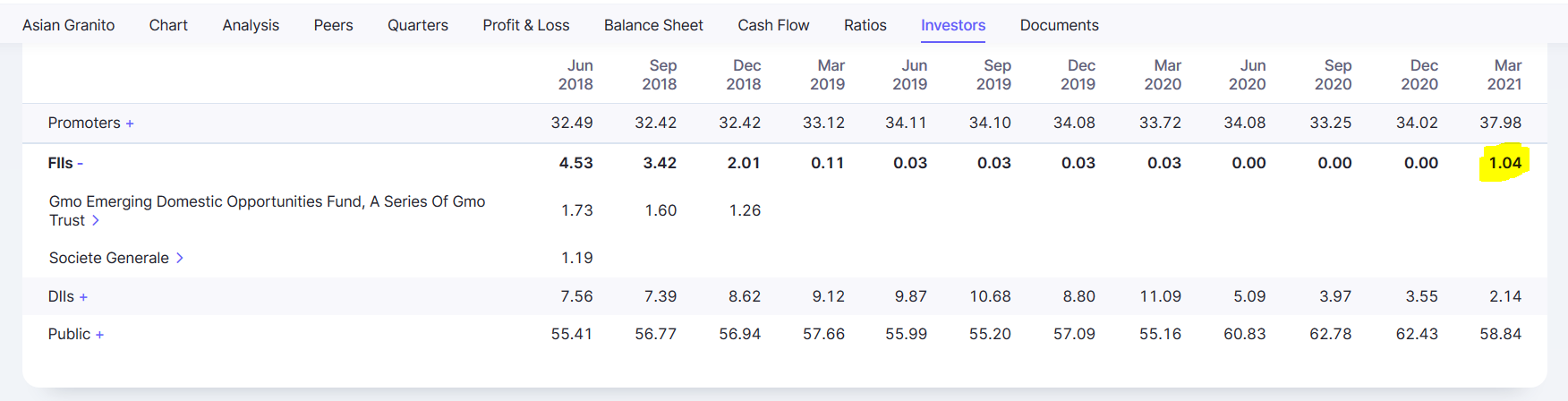

Looks like Sureshbhai Jivabhai Patel HUF and Chhayaben Sureshbhai Patel have been net sellers even in the March 21 quarter and possibly will continue disposing off their holding.

Sureshbhai Jivabhai Patel’s (not the HUF) shareholding has increased since Dec 2020 much more than the combined holding of Sureshbhai Jivabhai Patel HUF and Chhayaben Sureshbhai Patel. So, overall, the sum of the three promoter holdings has increased since Dec 2020.

So, overall not much concern, except in the short term.

Overall, there is too much going on in this stock. The company and the stock has the potential to do well over the next few quarters but the uncertainty level is high. Such stocks tend to eat the bandwidth of investors. For the new investors, the risk-reward ratio does not seem too favorable compared to many other opportunities in the market, at least before the Q1 FY22 results. However, for those having high conviction, this is a good opportunity.

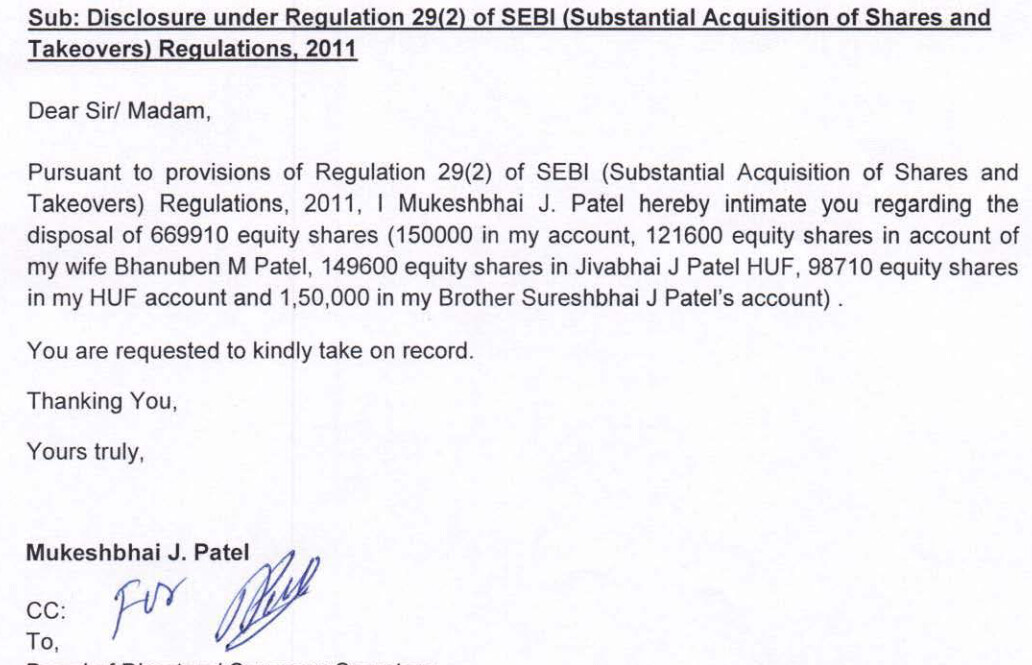

They’ve given an explanation to SEBI that the designated person “mistakenly” passed on wrong trading instruction to the broker, and that he is ready to face penal action as decided by the audit committee.

The whole situation is rather farcical. Lets see if the audit comitte does take some action after all. The market seems to have lost a lot of confidence in the promotors and management anyway over the past few months, and such acts adds to the cloud over their integrity. In this environment of uncertainty, it wold have been useful if the management did a year end concall to clear the air a bit.

Disclosure: Have taken a tracking position on Friday. May add to it on dips close to 160 as the future of the business looks to me but I want some more margin of safety.

I agree with your points. Just want to add what I believe happened:

They incorrectly sold from Sureshbhai Jivabhai Patel’s non-HUF holding when their intention was to sell from his HUF holding. Whether the mistake was from the broker’s side or not is anybody’s guess.

After the mis-selling was discovered, the SELL was compensated with a BUY of the same number (239,000) of stocks.

Subsequently, some holding from his HUF account was sold, on which there is no penal action. This means that there were no violations. This corroborates the above intention.

I have no way to prove this is what happened–this is purely my guess. If my guess is right, it looks like an honest mistake and is not much of concern. But, the company is truly in a farcical situation.

I am losing faith in my AGL thesis. The Jekyll Hyde nature of the management is troubling. Why is Mukesh Patel (MD) dumping his stake when AGL looks to be poised for a stellar future?

It is very strange. I can think of two possible explanations:

They need the funds for something else. This is the Occam’s razor option.

They amount sold is a little under 2% of total shares. Maybe they want to go back to the original shareholding they had prior to the March quarter. Most of the shares were bought at the bottom near the 140 mark, maybe it was always intended to be a trade by the promotors.

So while all of us are getting lured by the good story and cheap valuations, the promotors are busy making short term trading gains. Not sure how to to view this - at these valuations, there doesn’t seem to be much downside anyway over the medium to long term. But yes institutional investors will likely stay away from such a company.

Disclosure: Have a tracking position. Will observe price action over the next few days and decide whether to sell off.

I would apply the razor as @Vineetjain111 has suggested. The sale was maybe partly used to reduce one of the promotor entities pledges. The way I see it, the earlier transactions with warrants was to put money in the company.

Hope so. If they have used the funds to reduce pledge, I guess this will be communicated to the exchanges immediately, or will it be disclosed at the end of the quarter?

What I meant to say is that I see another promotor entity on 7 june, revoking pledge worth 0.66%, but they were not the parties to the sales. Speculating on a connection here? Yes, the revoke can be at a later date also.

And the selling continues. A total of 19.86 lakh shares have been sold by promotors (not counting the circular trades) over the past four trading sessions. That is nearly 6% of all outstanding shares for AGL. This means that the promotor holding is down to about 32% from 38% in March 2021. Compared to this, the total pledge revocation is only 0.66% in the same period.

Is this not very worrying?

I really don’t know what to make out of this. I guess there is no point panic selling at these levels anyway. Rather wait for some kind of a clarification in the next concall.

Hello, In all recent sell-off disclosures it appears that the promoters are re-shuffling the stakes within the family and between their respective HUF accounts.

I am speculating here: I believe it is being done to streamline the promoter shareholding. Right now there are 25 individuals/entities listed as promoters…which could be coming in the way of wooing large investors.