I Guess the below post would make some sense to what in know about ceramic industry that they have got USITC at the rate of 3.19%

Sorry for the new branch - it might help readers in efficient way

I Guess the below post would make some sense to what in know about ceramic industry that they have got USITC at the rate of 3.19%

Sorry for the new branch - it might help readers in efficient way

I have following questions:-

Disc:- No holding. Looking for opportunity

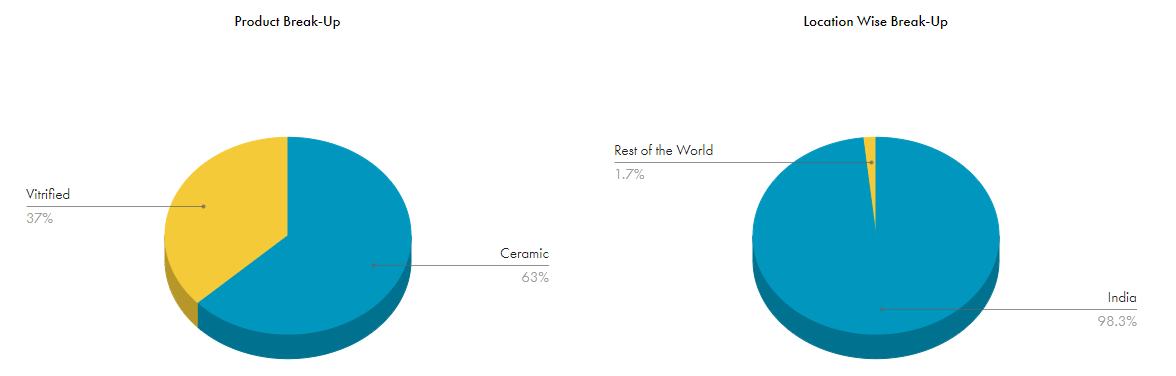

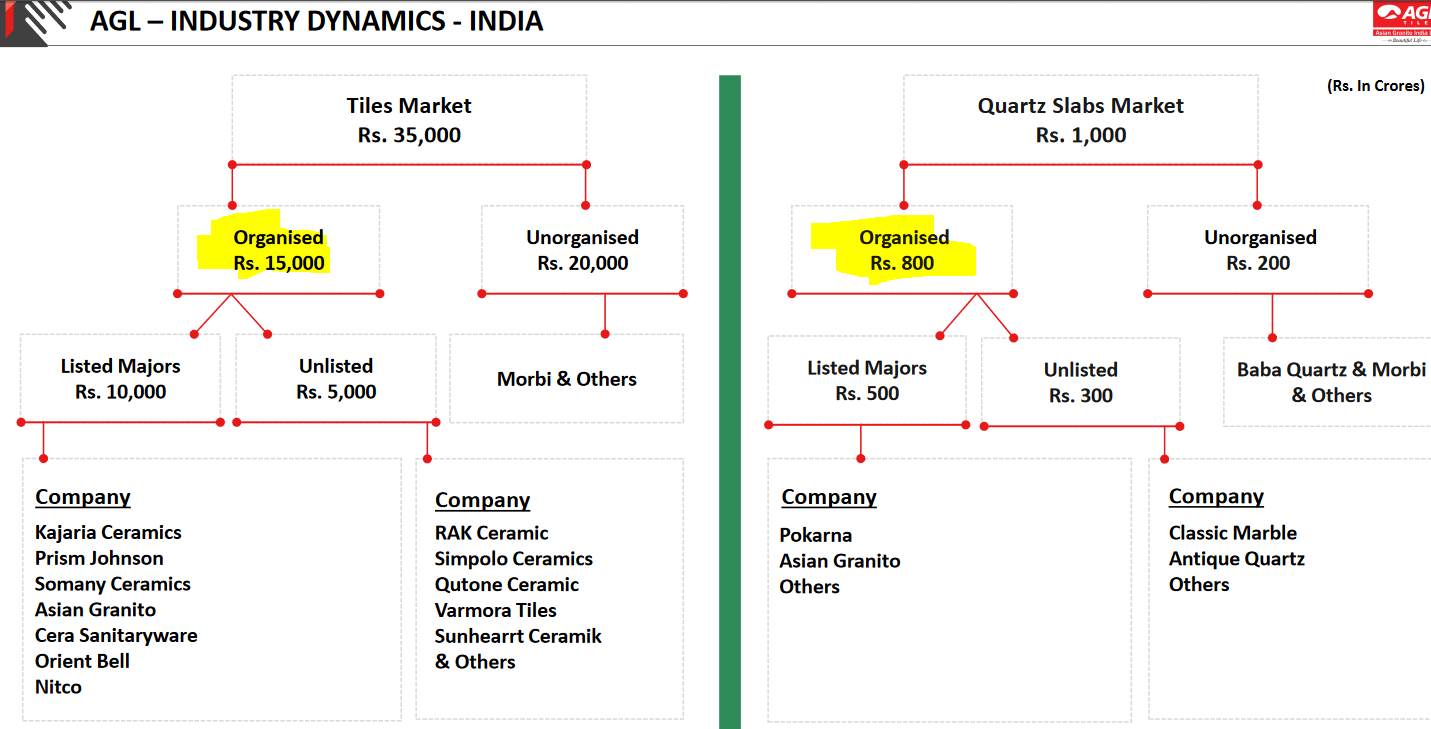

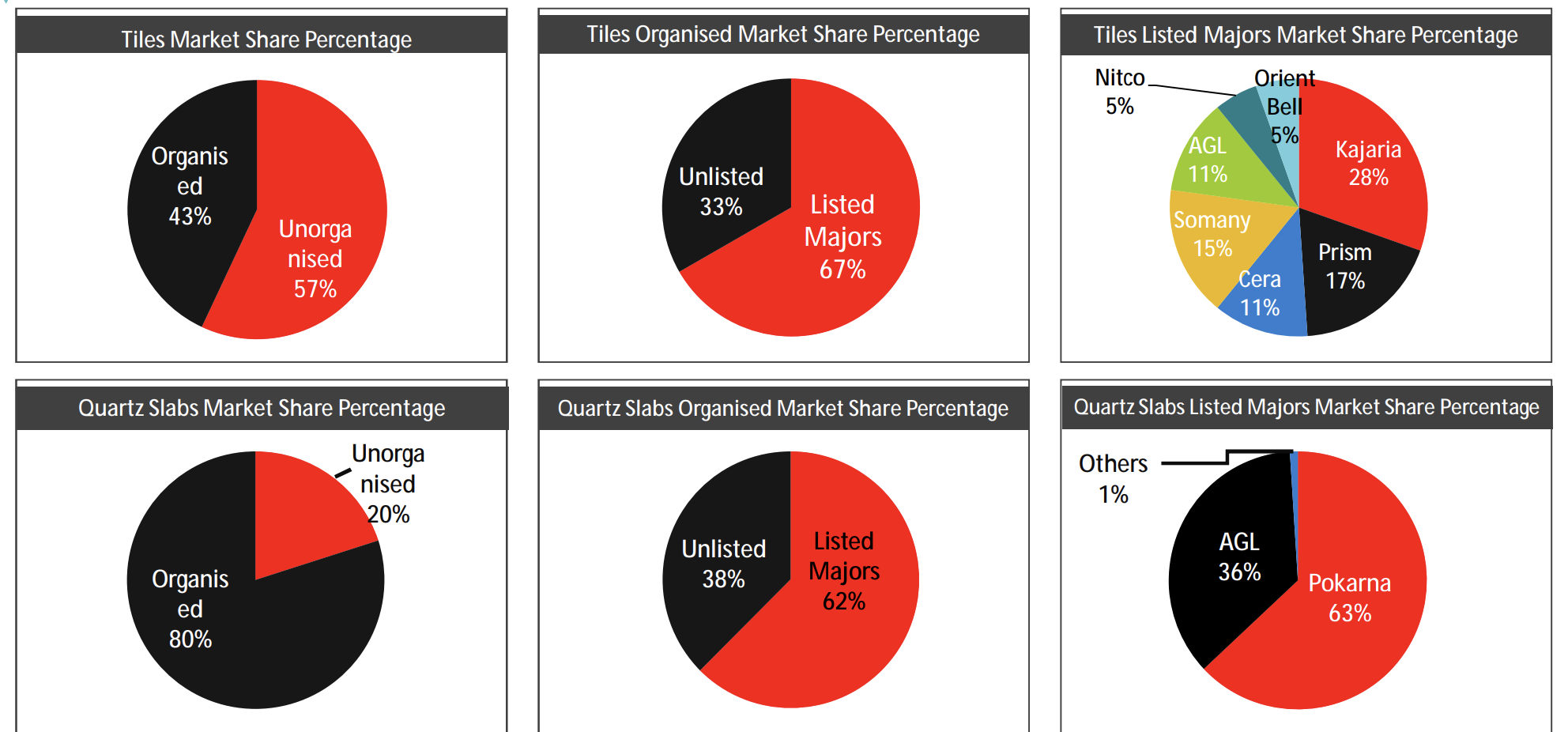

Just checked with the peers on Quartz : It seems Pokarna has the highest capacity of Quartz and majorly targeting USA because of their market share is high close to 68% market share only in USA.

When compared to Asian Granito it might do well - given a play of Quartz with having 43% market share where as their domestic share in Indian market stood high and export just stood about 15% last year

Asian Granito : Total shops in India 300+ (Major play tiles, faucet etc)

Quartz are very rarely in numbers

Pokarna : Major play tiles and especially Quartz

Other than Quartz

Orient Bell : Leading Tile Manufacturer in India with 1000 shops and quite dominant in price compared to all

Somany Ceramics : Next expensive one near to Kajaria with having larger capacity production and B2B also B2C player

Source : Tijori

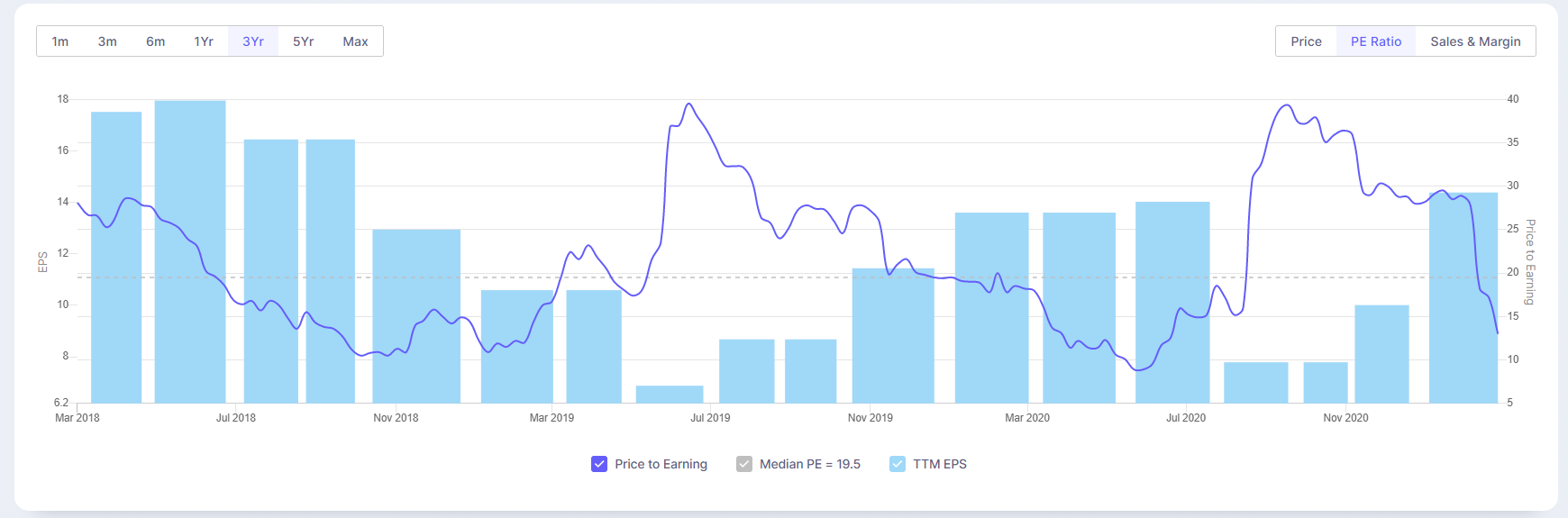

There has been a steep correction in prices and hence this good stock is available at cheaper valuation right now. The PE has been reduced from 30 level to 13, whereas there has not been any structural or fundamental change in the company.

This correction seems to be caused by the conversion of warrants to equity @175/Pc when the CMP was in the range of 250+. Can anyone help me how does this affect the market prices of a share?

AGL 20 Feb.pdf (471.4 KB)

There will be more dilution for existing shareholders (around 2%). Promoter issuing warrants have not been in the best interest of minority shareholders in the past.

It’s like issuing a long dated call options on your stock.

We would like to inform that the Company had passed special resolution in respect of Issue of Warrants, Convertible into Equity Shares on Preferential Basis at the Extraordinary General Meeting of the Members held on Friday, 05th April, 2019. Subsequently Company has received In-principle approval from the stock exchanges to allot 47,00,000 fully convertible warrants on Preferential Basis at Rs. 180/- (Rupees One Hundred Eighty only) each by way of passing circular resolution dated 09th September, 2019.

Now Company has received Letters from allottees for exercising their right of conversion of 7,50,000 warrants into equity shares as the balance amount of Rs. 10,12,50,000/- (Rupees Ten Crore Twelve Lakhs Fifty Thousand Only) at Rs. 135/- per warrant being 75% of balance amount is paid by said allottees.

THAT WAS THE ANNOUNCEMENT made over exchanges

Hope promoter restores his lost respect by doing right things here on. Also keep an eye for such warrant resolutions and vote against it.

I have been holding this stock since 2018 and did add more at 170 levels.

However, the instrinsic value of the share will remain same… right? These tricks by promotor seems manipulative.

The PE drop to 13 & P/B near to 1 gives a good entry point when the company is continuously profitable.

Asian Granito plans major debt reduction; To Focus on Asset Light and Capital Light business model

Highlights:

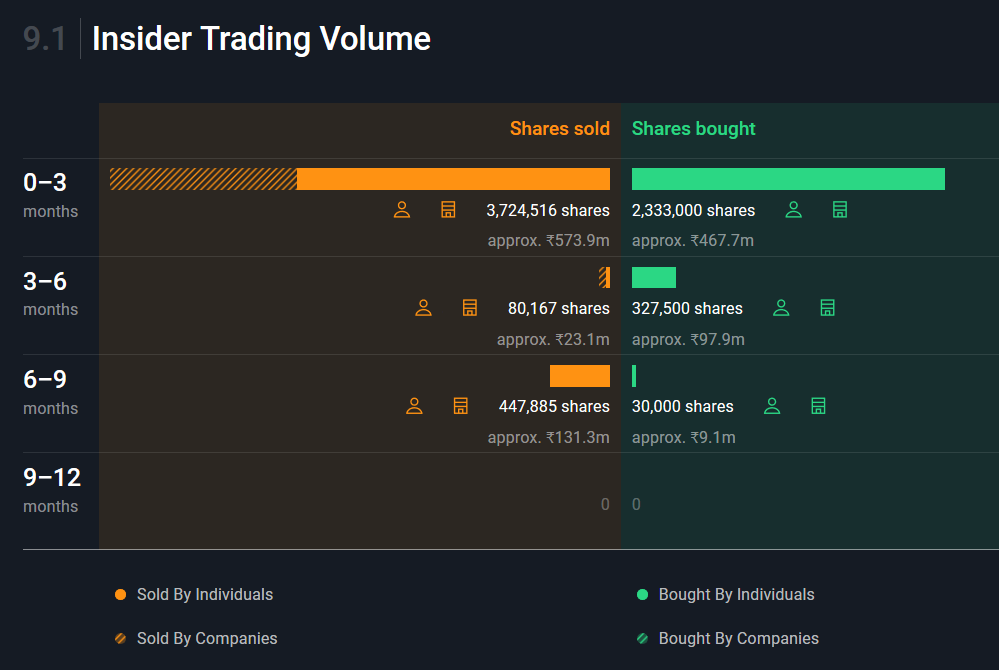

Does anyone have a thesis on the significant price correction? From insider trade transactions it looks like Kamlesh and Mukesh have been increasing their share (through warrant conversion) whereas other insiders have been net sellers. Though most of the warrants have been converted (some 35 L of 47 L) still the price continues to be range bound.

~~

Here is my estimate of where this stock is headed:

Very interesting talk by AGL’s Prafulla Gattani which talks about tailwinds for the industry in the coming quarters.

Disc.: invested, so my analysis could be biased

A couple of questions:

Disc: Not invested.

Well, I don’t have good answers to either of your questions but let me share my views anyway:

Price correction from around Rs 300 started around 1 Feb. On 20 Feb, the company informed about warrant issue at around Rs 180. How can we make sense of this price movement?

If you look at the transactions majority of the selling was done by insiders. My view is that promoter group didn’t have money at hand to exercise the warrants. They had already paid up 45 rupees per warrant in 2019 and didn’t want that investment go waste so it made sense to sell their current holding and use that money to exercise warrants (lest the share price tanked to below 135 rupees, in which case it would not have made sense).

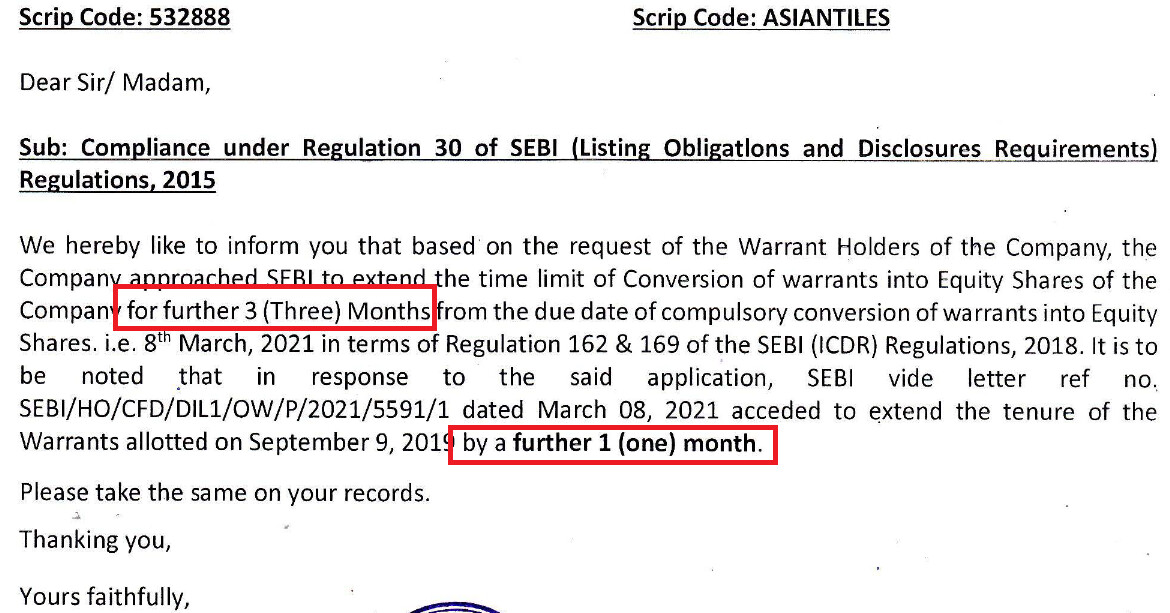

The initial letter that the management sent to SEBI (sometime in early March) had requested for an extension of deadline (for exercising warrants) by three months but eventually SEBI gave just one month extension. This kind of corroborates that there was a cash crunch.

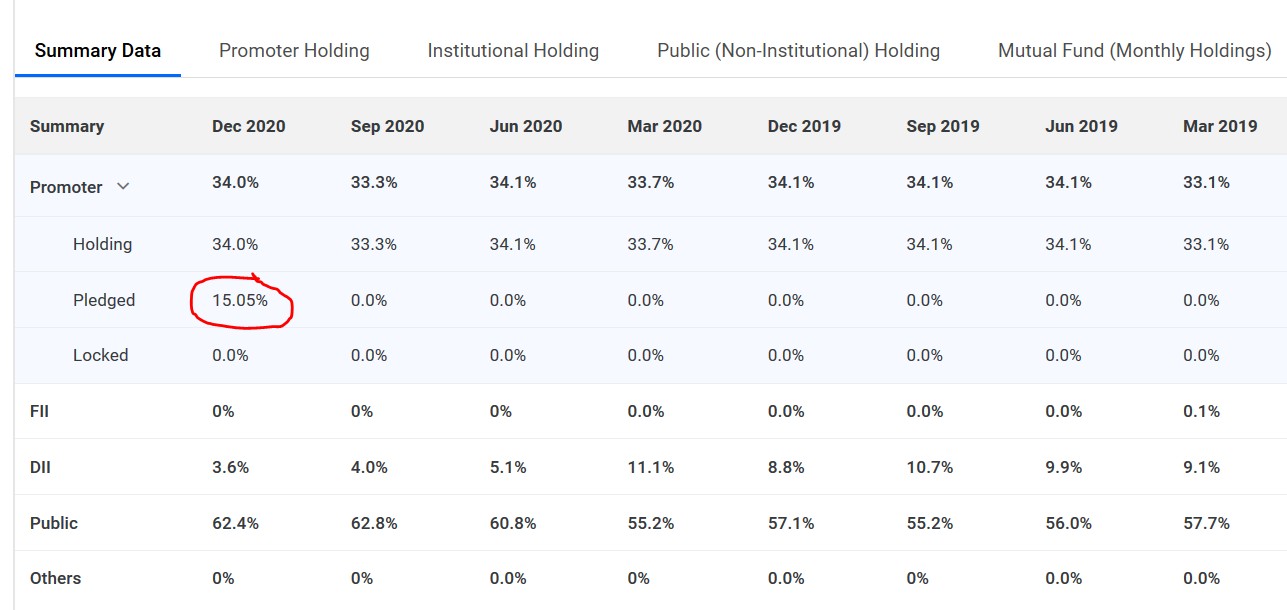

Further, the promoters pledged some of their shares recently which again points to the effort to raise cash for exercising warrants.

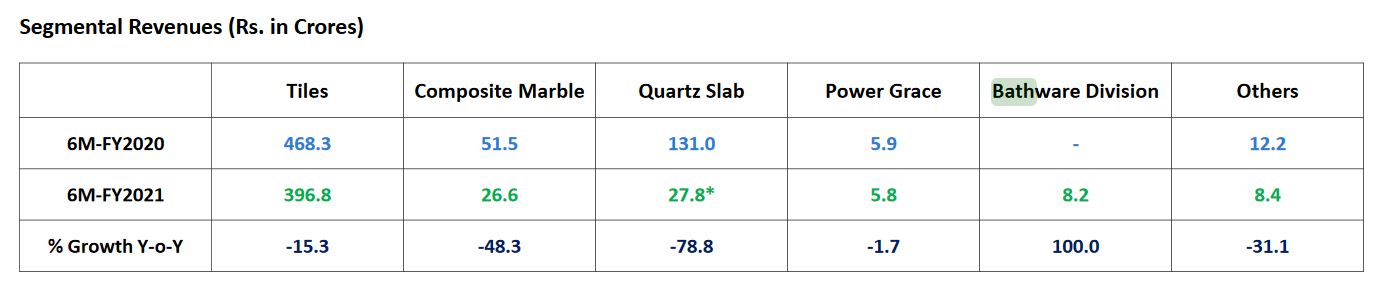

The company is looking to start a new tiles line. Given the bullish quartz/granite exports scenario, I would have expected them to focus on quartz/granite. Can we make sense of this? Is the company focusing on the domestic market?

Kamlesh Patel says in this interview (around 25 min into the interview) that Jan’21 and Feb’21 had a sharp uptick in sales, and that Mar’21 is showing a similar trend. Plus they are very aggressive on international sales. Well, we will soon know how Q4FY20 turned out to be.

Disc.: invested

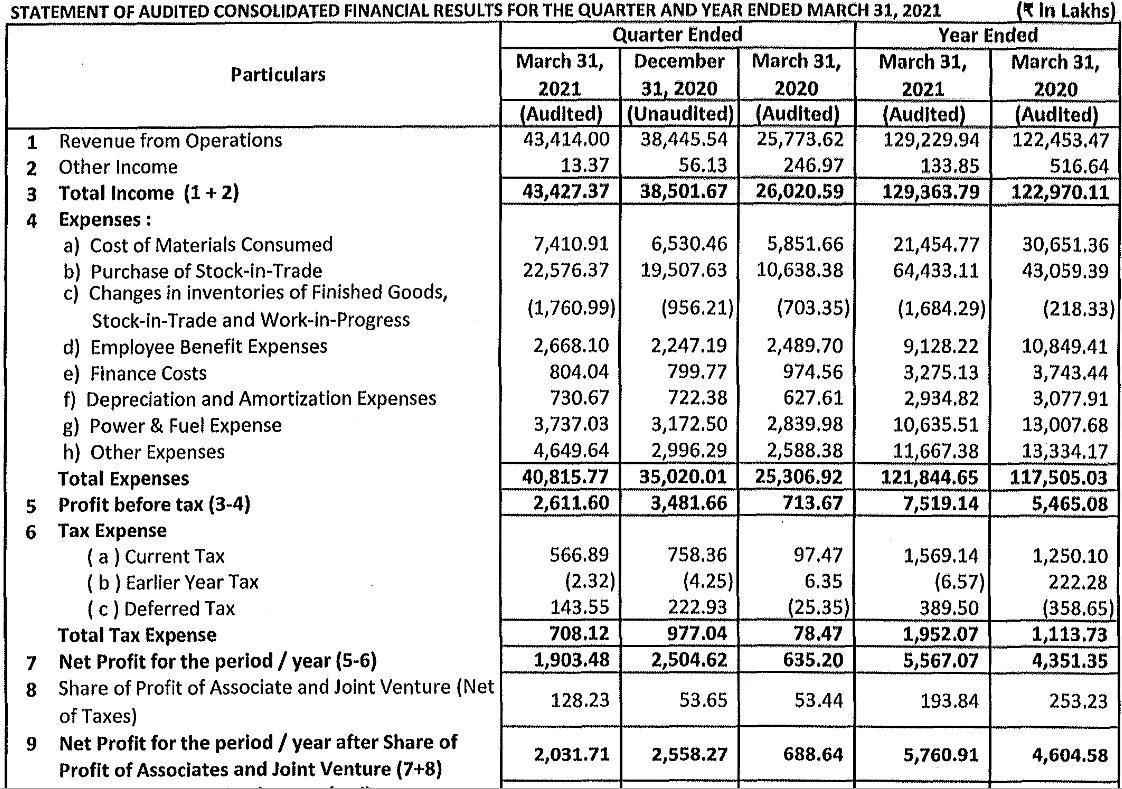

Results are out.

Disclosure: Invested.

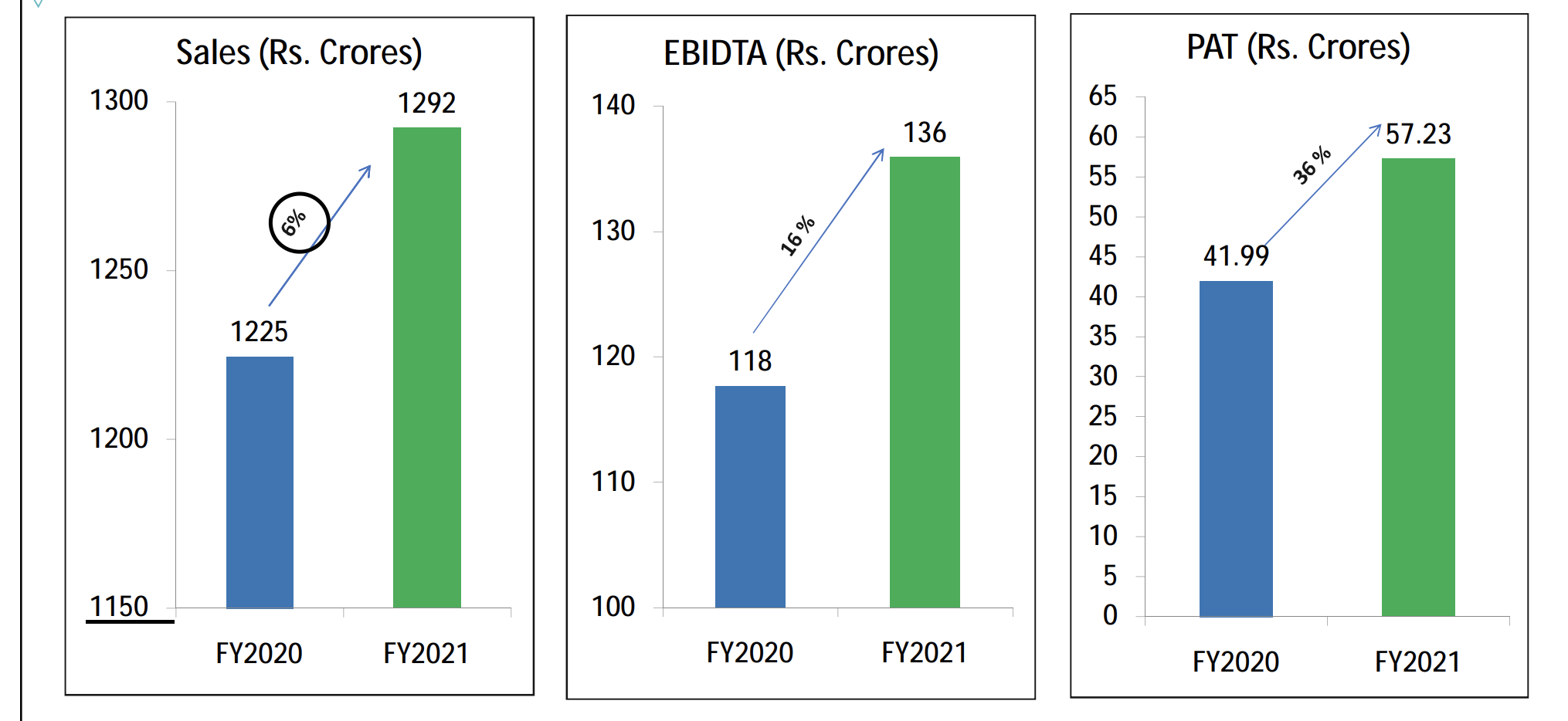

Good results posted by AGL – I am happy to see the top-line growth (both YoY and QoQ). A bit disappointed that bottom-line worsened QoQ.

Also, glad to see AGL focusing on core business –

Disc.: invested

Investor presentation of Asian Granito. Some points to note:

Things i didn’t like about the investor presentation:

agl investor presentation.pdf (2.7 MB)

HI all, I have just started tracking Asian Granito and I think this entire warrants situation has created an interesting opportunity for fresh investments.

I am concerned with the growing number of government contracts and the rise in receivables and debtor days over the past few quarters though. Debtor days are presently at 119 days which is a lot higher than all the peers: Somany is at 63 days, Cera at 67, Kajaria at 52, Orient bell at 57.

Warrants issue apart, I think this could be one of the reasons Asian Granite has been trading at relatively lower valuations than peers, in spite of optically performing as well or better than some peers on returns and growth parameters. This is likely the reason keping institutional investors away as well. Has the management addressed this issue in the recent past on concalls or interviews?

Watched ad. on cnbc aawaz? Proclaiming profit and eps of quarterly result? Don’t think its an ad of the product…but ad of co. shares…remember teledata few yrs. ago?

A big no no for me…

Just heard the q3 concall. Some questions that I am unclear on:

The management said immediately there is no more capex other than quartz line that is being added, and that 8-10% capaity increase is anticipated by FY 22 end in Morbi. They also said that growth outside of that is through asset light model and through outsourcing. That is what this press release from March 23rd also says.

Does anyone know exactly how this asset light model works and what are the economics of this process? What proportion of the business is presently outsourced / white labled?

Prima facie if AGL is marketing tiles whch are manufactured by someone else, it should be margin accretive as opposed to manufacturing themselves. Is this the case?

Also, is there any information on the concall for Q4 and full year too?

Prima facie if AGL is marketing tiles whch are manufactured by someone else, it should be margin accretive as opposed to manufacturing themselves. Is this the case?

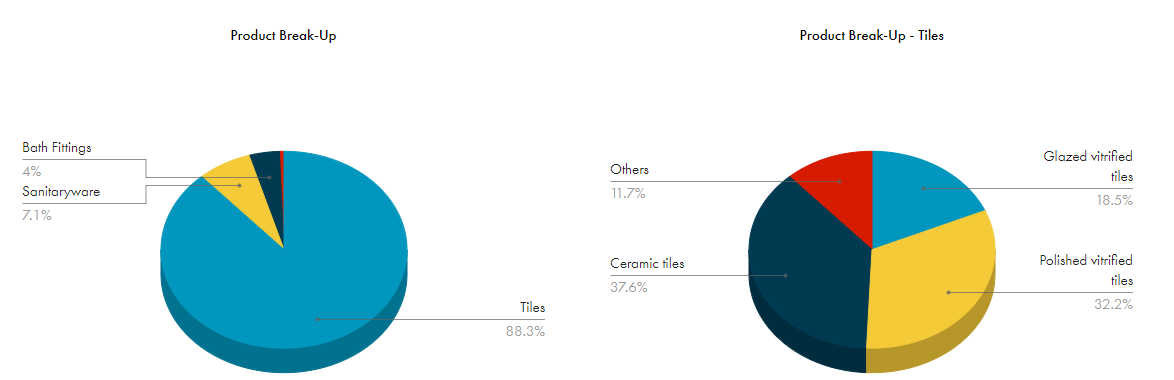

It’s not tiles just the bath fittings which are outsourced.

What proportion of the business is presently outsourced / white labled?

A safe assumption will be just the bath fittings business:

The company has been saying that they will grow with an asset-light model going forward. As I recall from memory, in one conf call, the management said they are already working on a grand scale (exporting to 100+ countries) and currently it is not possible to further expand the internal manufacturing operations (capacity utilization is 95% and they are adding some capacity). They did not give a clear view about the margins of the outsourced business. The company still has huge debt and personally I feel this may also be restricting the growth plans. I suspect the asset-light model may be a necessity at this point.

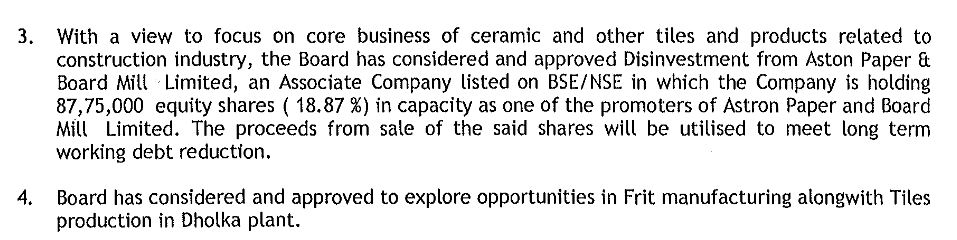

Selling stake in Astron Papers has not come at a particularly opportune time—the company looks a bit desperate to reduce the debt. An alternative viewpoint is that they are too bullish about the company growth going forward, which is why they want to quickly reduce debt. This is also supported by the increased promoter stake recently.