Oracle has it’s biggest market in Middle East. Wild guess - they went there before SAP. Elsewhere, to my knowledge, SAP is dominant.

There are always dips available for buying excellent businesses if you believe in them and once in a while crashes to add more…I have bought some excellent businesses at double and even triple my initial buy price and at hindsight feel that was a good decision to buy them at such higher prices than buying anything else. Not recommending to buy Oracle now but just a perspective that its never too late to enter or add more for the right business…all the best

1 Like

Hey It was good to interact on oracle, thought to put some more etime and write my thoughts on your picks -

- ITC - It is not undervalued but indeed a good business to invest

- L&T - Again, I do not think it is undervalued considering the economy/infra situation and uncertainty. A fine business but look at it this way, even L&T wanted to derisk themself from infra and hence gave birth to LTI and LTTS and even LTFH…so why invest in a business for long term in which the company itself does not believe in as their business of future…

- TCS - Behemoth indeed. Mr Mukesh Ambani missed the IT services in 1970s, he is not going to miss the digital again. The way Jio is galloping makes you want more from these Indian IT companies. Still agree its a great company and has beaten stagnation many times before…to my surprises.

- OFSS - Decent company. MNC. Leader in a sub segment. I would definitely be a buyer in crashes and admit I too missed it. Not sure about buying now…

- Quick heal - I completely agree on your vision for cyber security but have huge doubts if a company like Quick Heal will fulfill those ambitions. It is not a market leader (pls correct me if wrong). With Windows 10, Apple and Linux…the operating systems are getting stronger day by day and more secure. Windows defender does a decent job as compared to some basic antiviruses. Also, if I am too much concerned about security, I wouldnt mind paying extra to get the best than settle for a second best.

- Delta - Never tracked, not aware

- IDFC First - It is not undervalued. There are specific reasons for its valuations. I had held it for a very very long time because of same reasons but Q after Q same story repeated itself. I lost significant opportunities and gained patience in IDFC First. Also realized that management likes saying same things every Q and I don’t like listening them anymore, so sold out.

- Thyrocare - This is a wonder company for me because many times when I listen or read about its founder, I wonder. Therefore, i stayed away so far, I maybe wrong.

- HDFC LTD. - Although best, still a lending NBFC. Hold for long term but with caution.

- Bata India - I think its a leader. Good Brand. As it is into retail stores (capital intensive if self owned), some risks maybe involved. Not tracked much.

- HDFC Bank - Been a good bank, but we must always remember it lends money so hod for long term with caution.

Disc: Above all are purely my thoughts and interpretations and I maybe totally wrong. Not a recommendation to buy/sell.

4 Likes

Thank you for the feedback!

Also I played out poker on adda52 it horrible games are fixed won’t last long time. You can see reviews all are saying it is a scam

when you have ITC+HDFC LMT you cover more than 10 business:)

Overall looks good for a good sleep. Can you share your allocation?

If you have HDFC Ltd then you can avoid HDFC Bank (also you have IDFC) - my personnel opinion

Thyrocare &OFSS are good value stocks

1 Like

Tcs & itc abt 17% each, L&T 12%, quickheal, delta and idfc bank around 8-9% each, thyrocare and ofss about 7% each and the rest is in hdfc twins. Bata is a very small position.

Looking forward to adding Ofss and xelpmoc.

I have some confusion - Oracle financial seems to be erstwhile iflex …does it include Oracle ERP for finance as well (Oracle FUSION etc.) and any part of database business or it is only the product i-flex?

To be honest, even I have doubts on the exact bifurcation of it’s business with parent entity.

Hi Ashish,

As I can see, half of your PF is of large cap/bluechip. No doubt they are leader of their field but there are cheaper way to invest in them through say Index fund & channelise your effort and research for finding better companies in small& mid cap space in growing sectors like pharma,chemical,IT,CRAMS etc etc. Of course , detail research & your circle of competency are essential to gain conviction.

Just my thought!!

2 Likes

Thank you for the advice!

Exited Quick heal. Looking to add more of Xelpmoc, also looking at Just Dial, there new addition JDMart looks exciting.

1 Like

Financial Services Solutions | Oracle I reckon everything under this link falls under OFSS. Annual report points to this link as well. There are some services for e.g. Oracle Financial Crime and Compliance Management Cloud Service. There are others too with pay-as-you-go pricing model. I am assuming they scale up and down as per usage just like AWS. Looks promising, I may be biased.

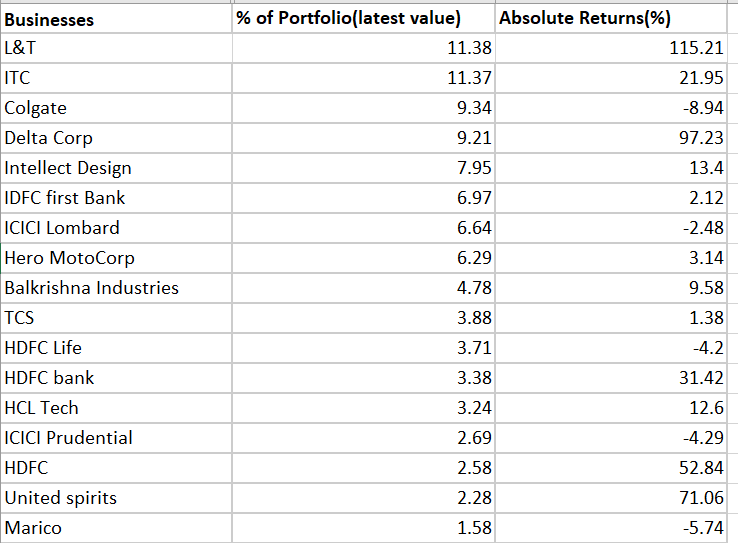

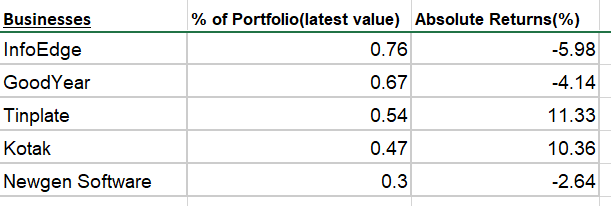

Latest Portfolio update:

Tracking below:

Please feel free to point out any chinks in the armor.

Thanks!!!

1 Like

However I might not be apt as per my experience but definitely can suggest few thoughts:

- Don’t know ITC, colgate and Marico doing in single portfolio and also being 2nd ,3rd larget positions respectively

- You are getting too heavy on insurance, I might agree post covid people will focus on these sector but I still feel you are getting very much optmistic

My sugestings:

1.Bajaj twins are missing ( my biggest mistake in my portfolio)

2.Try to bring infoedge as soon as possible when you feel comfortable with business - No chemicals and pharma , there might be chance that you are not much aware about these themes but what I learned from my past mistakes if you are not good at any sector atleast try to go with market leaders it won’t harm that much

Note: I am not that much experience and not really good at it, I just read and keep myself updated

My learnings are in this link: Novice Investor

1 Like

ITC is undervalued, but is value packed. Recent commentaries on the economic conclave and has beaten inflation concerns if you are not aware of the results without much of price hikes compared to its peers.

IDFC FIRST, you can hold it for a multibagger. I or We cant say how well it will turn up. See to the performance of Vaithiyanathanat ICICI and the financials after merger and growth in banking infra has gone through the roof. Execution has been vital from loan disbursal to tech adoption.

Its very well known Bata is going under.

If your are holding LTTS, guaranteeing a multi bagger is hard. They have several growth engines which goes with the economy and continue to hold.

TCS its a behemoth, but go for niche players. Rsystems, Xelpmoc, Tata elxsi etc.

Thankyou

The portfolio seems to be concentrated more on insurance, FMCG. ICICI insurance is just fine and the whole group seems to take over HDFC. Colgate is a great business, but not a great investment.

Hero i personally feel they haven’t come out of the pollution norm beat. Inflation is making it hard to progress. From bikes the rural population have started opting for cheap cars as income at the various areas increase in double digits because of IT. Not a fan of two wheeler companies. TVS is one with more growth i suppose.

thankyou