Asarfi Hospital is a 250 bedded multi-specialty hospital offering healthcare facilities to people for nearly two decades in Dhanbad, Jharkhand. The entity is Accredited by National Accreditation Board for Testing and Calibration Laboratories (NABL Accredited).

Pros:

EV/EBITDA is just 8.06 which is fairly low compared to its peers (avg. of 18, a discount of 2.23x)

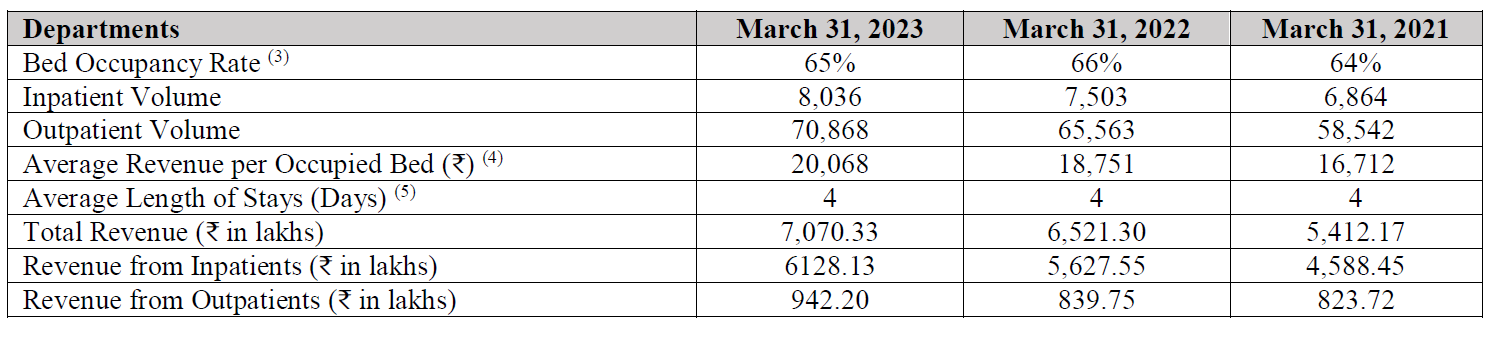

Sustainable avg. EBITDA margin of 16.5% in last 3 years

D/E is low at 0.4

Plans to open a cancer care hospital with IPO (no other cancer hospital in Dhanbad) and a medical college (very profitable side-business)

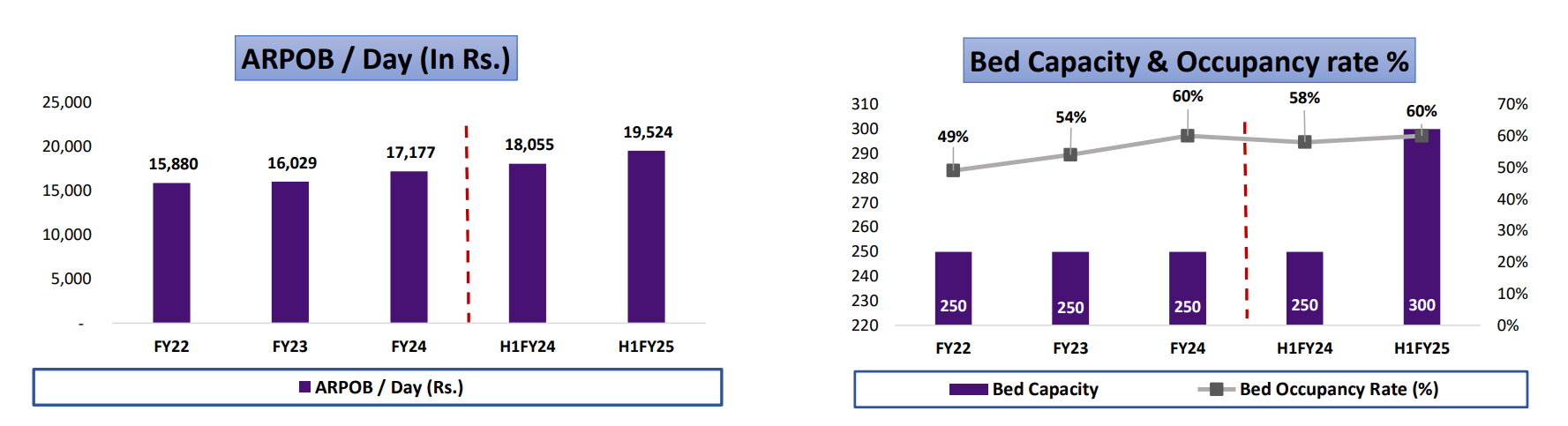

Steady 10% increase in ARPOB YoY

Bed occupancy rate is ~65% which is decent with avg. inpatient stay of 4 days.

Cons:

Land for building cancer hospital is currently in legal dispute in HC (They won the case in district court)

CFO from Operations was negative in FY-23 due to high trade receivables (not sure how that can happen in a hospital - someone please share insights)

Price to CFO in FY-22 was 5.6 which is expensive compared to its stated peers (avg. of 2.13)/ but the peers aren’t directly comparable

Overall seems like a safe bet for short to long-term (if they win the legal case which can get stuck).

why not artemis or kovai hospital over this ? artemis is available at 2.5x sale . Kovai at 3x a better brand , in high income state , visibility of expansion plan where as this being ultra small cap would be available at 2.25 x sales (adjusting grey market premium) .

Update on Asarfi post Q2FY25 results as well as some of my own thoughts:

Occupancy rate is at 60%. Ideally occupancy should be higher due to lack of hospitals in Jharkhand (they have some competitors in place). And they also face competition from West Bengal which is a medical tourism hub. Company has increased their catchment area to 10 districts.

Receivables being high in comparison with other hospitals –

Company has made a dedicated team to bring down the debtor days but it depends on the govt institutions (Coal India, Railways, Ayushman Bharat) as split is 50:50

Don’t need immediate equity dilution but this can become a constraint down the line

Cancer hospital – 74 Cr invested till date

FY25: 20 Cr sales (Sep run rate: 1.59 Cr)

FY26: 35 Cr sales. Management has also said that they want to achieve 6 Cr MRR in 2-2.5 years

Company will increase bed capacity to 150 in next 2 years with 1-2 Cr investment to primarily be eligible for subsidy of 12.5 Cr from Jharkhand govt under their scheme. This subsidy is yet to be received but application is processed

The additional 100 beds would primarily be added like general beds to gain the subsidy and the company will keep adding equipment from internal accruals over the years. Seems like this would impact ARPOB

ARPOB:

Multi-speciality - 19,958. Target over next 2 years – 25,000 (seem too ambitious)

Cancer hospital - 16,748. Target over next 2 years – 30,000

Land dispute for cancer hospital

Land taken on lease from govt. High court said that land is not the governments to give and awarded the land back to a private party.

The Supreme Court has ordered for fresh adjudication but as per management they have been removed as party to the suit and then it will take 10-15 years to resolve the case

However, here I am a a little skeptical. I read the SC judgement and the case has just been disposed of for re-adjudication. Nowhere is it mentioned that Asarfi won’t have to fight the case.

Land for Health research institution

Will be used for running allied courses like nursing

Primarily used for talent generation once they expand their hospital capacity

Limited revenue generation capabilities (looking at Kovai). But they aim to approach the govt in the future to allow them to create a medical college

Vision for next 10 years

400 own beds (main hosp + cancer) + 100 (new hospital acquisition) + 500 (O&M mode) = 1000

4% sales commission to be paid to hospital partner for O&M

Sales – 400 Cr with PAT – 50 Cr (30% PAT CAGR is very ambitious) → But then management clarified that they’re targeting 400 Cr revenue in next 4 years

Guidance from H1FY25 to FY26

Beds – 300 to 380

ARPOB – 19,524 to 19,823 (but this is not in line with their above guidance?)

Revenue growth – 18% (last 3 years, check if FY24 or H1 Wise) to 29% (next 2 years)

EBITDA margin – 21.4% to 23.7%

PAT margin growth – 7.7% to 11% → Essentially they’re claiming a PAT CAGR of ~87% over FY24!!

ROCE – 9% to 15%

Red flags or Areas of concern:

18 Cr Loans Disbursed in H1 FY25: I have written to the company secretary regarding this but so far haven’t received any response back.

To whom were the loans amounting to ₹18 crore disbursed?

What is the tenure of these loans?

Are these loans interest-bearing? If yes, what is the applicable rate?

Company has claimed to increase ARPOB by 25-30% over next two years in the concall but in the investor ppt they have hardly shown any expected growth.

One reason could be that management is expecting ARPOB on existing beds to increase but overall no. would decrease due to addition of 100 cancer beds for getting subsidy which would have minimal impact. The numbers make sense

Based on above commentary from promoters, I have taken the position given there is high volume and good delivery as well.

I am expecting FWD PE as 18 on low side with 100% yoy growth based on FY24, increasing arpob in cancer beds plus multi specialty beds as well. HNI and funds are there, high growth sector. Expecting PE to be around 30 for this industry and market cap.

Please let me know when you hear back on the 18cr loan.

Reply from Asarfi Management : 1. 18 Cr Loans Disbursed in H1 FY25.

To whom were the loans amounting to ₹18 crore disbursed?

Ans: Long Term Loans & Advances (Total: Rs. 13.55 Crores):

Advance to Ranchi Smart City Corp Limited: Rs. 13.09 Crores, given for the purchase of land at Ranchi, which was duly registered in October.

Loan to Subsidiary: Rs. 46.00 Lakhs, provided for establishing a university/college on the land.

Short Term Loans & Advances (Total: Rs. 4.84 Crores):

Advances to Employees and Staff: Rs. 0.01 Crore

Advances to Suppliers for Purchase of Machinery: Rs. 0.85 Crore

Refund from Income Tax Department for FY 2023-24: Rs. 2.39 Crores.

Advance Tax and TDS Deposited and Deducted as of 30.09.2024: Rs. 1.43 Crores.

*** What is the tenure of these loans?**

Ans: This loan & advances has no tenure as it is a kind of investment which is given to the subsidiary company for establishment a university/college purchasing land or for business expansion

*** Are these loans interest-bearing? If yes, what is the applicable rate?**

Ans: No

2. Also, in concall, management mentioned that they are expecting ARPOB on existing beds to increase but overall ARPOB would decrease due to the addition of 100 cancer beds.

Ans: To improve ARPOB we are making efforts to reduce ALOS. Revision of Rates of hospital Services is also due. After detailed analysis of coemption if we decide to increase the rates then the quoted numbers are definitely achievable for existing hospital and for Cancer hospital the communicated number is achievable.

What amount of subsidy will come to the company after reaching 150 cancer bed hospitals.

NABH Accreditation:

The company claims NABH accreditation on its website. However, I could not find the hospital listed in the NABH registry alongside other accredited hospitals in Jharkhand on the official NABH portal (Source).

ARPOB and Bed Occupancy Rates (FY22 and FY23):

The ARPOB and bed occupancy rates for FY22 and FY23 mentioned in the IPO RHP differ from those in the latest H1FY25 earnings report. Someone had asked this question in latest concall as well but no answer was given as the topic got diverted H1FY25 PPT

Operational Beds for ARPOB Calculation:

ARPOB calculation for FY22 to FY24 only makes sense if 227 operational beds are considered

Cancer Hospital Occupancy Rate (H1FY25):

On page 20 of the latest H1FY25 PPT, the occupancy rate for the cancer hospital (50 beds) is mentioned as both 25% and 57%. Again, this is not clearly answerable in transcript (I didn’t check audio)’

Promoter:

MD- Udai Pratap Singh, BTech + MBA (US), very young, no medical background. Just 16.5 lacs salary in FY24. Son of Nayan Prakash Singh, who is brother of Harendra Singh

CFO – Harendra Singh, ex-CEO, MBA from LBSIM, New Delhi. Just 34.5 lacs salary in FY24. Looks like he runs the show primarily, Udai is his nephew. Probably an MD in name only

Related party transactions

Company has some 1 Cr worth related party transactions with another promoter owned company (ASAP Impact Pvt Ltd).

Interestingly, this company also owns another hospital in Asarfi Hospital Ballia with 100 beds. Wonder why this is not under the listed entity