Asahi India Glass Limited (AIS)

Company Background

Asahi India Glass Limited (AIS) is one of the largest integrated glass solutions company in India and the biggest player in the automotive glass market and the second largest player in the float glass market. It has a market share of over 75% in the automotive passenger vehicle glass market and is a supplier to all the major automobile companies.

The company ventured into float glass business in 2001 through acquisition of Flat Glass India Limited in 2001. Subsequently in 2003 the company was merged with Asahi India Glass.

The company is present in the following segments:

- Automotive glass products : The various types of glass range from laminated windshields, tempered glass for sidelites and backlites to a range of value-added glasses like Solar control, Acoustic, De-fogger, Head-up display, etc…

- Architectural glass products : The architectural product range includes clear, tinted, solar control & heat reflective glass, mirrors, frosted and back painted glass, along with a range of value added solutions in privacy, safety and acoustics.

- AIS Windshield Expert : India’s first and largest car windscreen repair & replacement network in India with presence across 45+ cities with 90+ conveniently located service centers.

- AIS Glasxperts : The company provides of lifestyle solutions in glass whose offerings span privacy, aesthetics, security, acoustic, energy-efficiency and door and window solutions.

- AIS Windows : A range of High Performance uPVC, wood and aluminium door and window solutions that include Acoustic, Privacy, Energy efficiency and Safety & Security solutions.

Business Model

-

The glass market is entirely B2B at present. The two segments in which AIS operates work differently:

- Architectural Glass: Higher competition and fight for volumes

- Automotive Glass: Lower competition and strict minimum quality requirements

-

The key raw materials in making float & automotive glass include

- Silica Sand

- Limestone & Soda Ash

- Power & Fuel

- Poly vinyl Butyral

-

The company has five glass plants as following:

-

Bawal (Haryana) (Automotive)

-

Roorkee (Uttarakhand) (Float)

-

Chennai (Tamil Nadu) (Automotive)

-

Taloja (Maharashtra) (Float)

-

Patan (Gujarat) (Automotive)

Segmental Overview

- The company operates in two segments

- Automotive Glass

- Float Glass

- As on March 2019 the segmental contribution from the two segments is as presented below

- Automotive: 60%

- Float Glass: 39%

- The historical revenues from the following segments have been attached in the sheet below

Subsidiaries

- The management has been talking about setting up a B2C business through its subsidiaries since 2010

- It operates in the B2C segment through the following subsidiaries named:

- AIS Glass Solutions Limited

- GX Glass Sales & Services Private Limited

- Integrated Glass Materials Inc.

- The performance of these subsidiaries is provided in the sheet below:

The performance of these subsidiaries presents a very grim picture over the last 10 years.

Neither have they been able to scale up revenues meaningfully, nor are they profitable.

Promoters

AIS was setup as a joint venture between the Labroo family, Asahi Glass Co. Ltd. And Maruti Suzuki India Limited in 1984. The current shareholding structure stands as per below:

- Labroo & Family: 20.96%

- Maruti Suzuki: 11.11%

- Asahi Glass Co: 22.21%

Promoter Pledge

Of the total promoter holding 6.77% is pledged of which Mr. Sanjay Labroo (MD) and Mr. Brij Mohan Labroo (Chairman) has pledged 46.24% and 11.78% of their shareholding respectively.

Competitors

- Saint Gobain

- Gujarat Guardian

- Sisecam Flat Glass

Industry

- The automotive and construction industry are the two largest influencers for the glass industry

- Asahi India Glass is the leader in automotive glass while Saint Gobain is the leader in float glass capacity in India

- The architectural glass industry comprises of float glass and processing glass. The float glass industry comprises of 5 players while the processing glass industry is highly competitive with over 200 players

- The float glass industry is expected to grow at a rate of 8-10% from here

- Two specific concerns for the industry in India remain:

- Creating minimum standards around energy efficiency in building construction

- Protecting domestic players from dumping by countries where major costs are heavily subsidised

- The technology for tempering glass through toughening is a freely available technology requiring very small investment and hence many small players have appeared for the same

- The automotive glass market is expected to grow at a rate similar to automobile growth rate in India

- Since power & fuel is a major raw material for making glass the company continues to face threat from imports out of countries where power cost is cheap

- The company seems to have limited pricing power . Here is what the management mentioned in the Annual Report of 2013

“The costs increased by over 50% over last 3 years. However the industry could only increase selling price by 10%.”

Capital History

- The company has never diluted equity to raise external capital throughout its entire history of operations

- The company has issued bonus shares 3 times in 1997, 2001 and 2005

- There was an amalgamation in 2003 that led to share capital increasing by 59.63 lakh shares

- There was a rights issue in 2013 to provide equity support to the company

Here is what the promoter had mentioned in the annual report of 2014:

“We have invested for growth from the beginning using debt to conserve equity , but within judicious parameters, which could be sustained by our performance. Maybe our track record of 20+ years, duly adjusted for a conservative outlook, gave us the confidence to continue as in the past in this most capital intensive industry.”

Debt

The management had mentioned in 2010 that it will use debt consciously. However due to capital intensive nature of business debt will always remain on company’s books

Auditors

The auditors of the company “VSSA & Associates” are auditors to two other listed companies:

- ISF Limited

- Perfectpac Limited

Capacity Expansion History

- The company has recently commissioned a new truck and bus furnace in Chennai.

- The company is setting up a sub assembly unit in Andhra Pradesh for Kia Motors

- In 2018 the company completed the refurbishment of its Taloja plant with a cold repair of the furnace

- In 2004 the company had embarked upon a capacity expansion of Rs 1100 crores

- Capacity addition under 2004 capex

- Auto plant at Chennai

- Auto plant at Roorkee

- Expansion of automotive capacities at Bawal

- Float Glass plant at Roorkee

- Processed glass capacities at Chennai, Bawal, Roorkee & Taloja

- Recently it has setup an automotive glass plant in Gujarat to cater exclusively for Maruti at a cost of Rs 600 crores.

Troubles

The company had gone for a major capacity expansion in during 2004-07 period and in 2008 when the global economy collapsed the company had gone into losses due to excess leverage

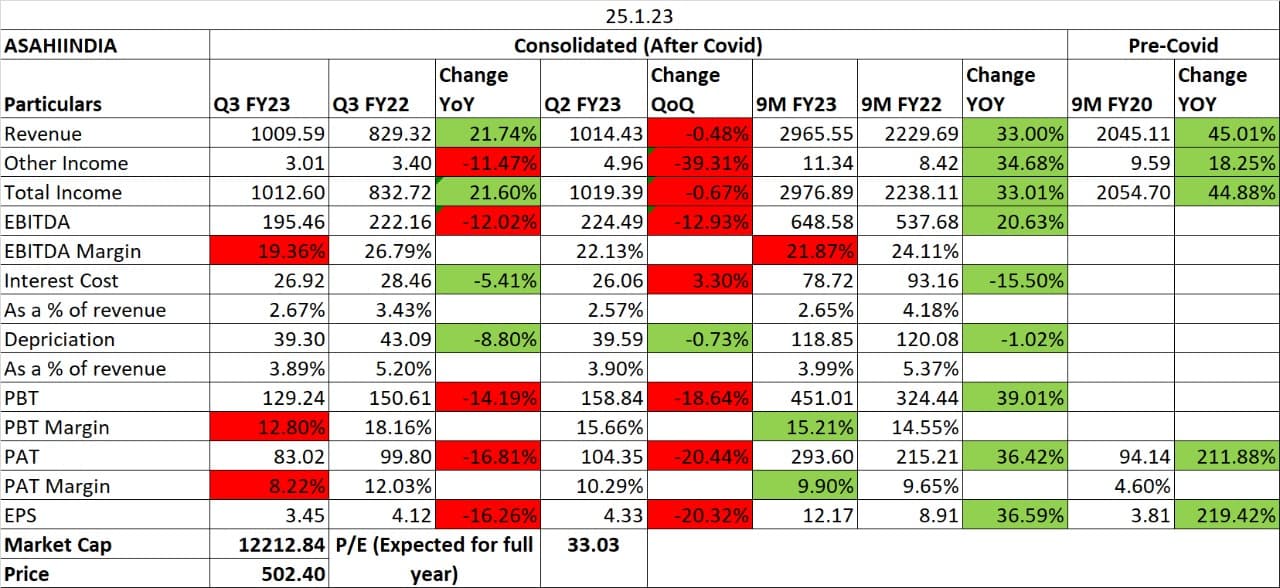

Financials

Here are my observations on the detailed financials of the company:

-

The company has grown sales at a CAGR of 15.5% over the last 22 years

-

The company was posting losses on a net level during 2009-2014. This was due to interest burden, forex losses on ECB loan and lower capacity utilisation

-

Post 2014 the EPS is up by 4 times while the company has also started paying off dividends since 2017

-

The net margins have gone from 2.4% to 6.6% from 2015 – 2019. The company posted losses in four out of six years from 2009-2014. Prior to that net margins were positive but volatile

-

The company’s ROE have been in double digits since 2015 post which it started making profit’s on a net level

-

The company has spent Rs 1242 crores on capex over 2016-2019. Similarly the company had spent Rs 1451 crores on capex over 2005-09

-

The company’s cumulative CFO during 2005-09 when it had spent Rs 1451 crores on capacity additions was Rs 187 crores while during 2016 – 2019 the company has generated cumulative CFO of Rs 1516 crores and spent Rs 1242 crores on capex

-

The share capital increased in 2014 due to a rights issue when the company raised Rs 250 crores to reduce debt on balance sheet

-

The capacity addition during 2005-09 was done via External Commercial Borrowings and subsequent devaluation of rupee resulted into forex losses for the company

-

Since 1997:

- Cumulative EBITDA: Rs 4216 crores

- Cumulative cash flow from operations: Rs 2458 crores

- Cumulative Capex: Rs 3393 crores

- Cumulative Free Cash Flow: Rs 919 crores (Negative)

-

Cash Flow

- The company’s operating cash flow looks much improved since 2017 partly because of good operational profitability and partly because it stopped deducting interest expenditure from operational cash flows and started deducting it under financing

- The company’s operating cash flow looks much improved since 2017 partly because of good operational profitability and partly because it stopped deducting interest expenditure from operational cash flows and started deducting it under financing

-

Working Capital

- The business operates on average working capital of around 20% to sales for over two decades

-

A detailed working of the financials is provided in the sheet below

Gross Margins

The gross margin profile has been updated in the sheet below

Dividends

- The company had not paid any dividends during 2008-2015 when it was facing financial trouble

- It restarted dividends from 2016

Peers

Since Saint Gobain is the biggest peer for Asahi India I have collated major points said by the Saint Gobain management about the float glass industry in India

- The company has spent Rs 1200 crores for setting up a new float glass unit and aims to grow sales by 10% over next 10 years

- India offers great long term prospects as consumption of glass is very low

- With addition of new capacity the company will now have total capacity of 140 million sq foot of glass

- In 2018 the company clocked sales of Rs 7000 crores

https://www.thehindubusinessline.com/companies/saint-gobain-invests-1200-cr-in-3-projects/article26114039.ece January 2019

- The Indian operations currently contribute less than 1% of the global turnover of the company

- Started own manufacturing facility in the country in 2000 with a float glass plant in Chennai

- The company has a market share of 50% in the float glass market with the rest 50% divided amongst the rest four players

- Market size in India for float glass is 2 million tonnes and growing at 7-8% annum

Saint-Gobain is fast moving into the B2C space: Will it succeed? | Business Standard News February 2019

Saint Gobain will set up a float glass unit in Vizag with investments of over Rs 2000 crores

Saint-Gobain setting up glass unit in Vizag - The Hindu BusinessLine March 2019

- India is fastest glass market in the world and the company estimates to grow its revenue by 8% in a decade

- About 60% of Saint Gobain’s revenue from India comes from flat glass business

Saint-Gobain sees confluence of growth drivers in India, says B Santhanam - BusinessToday March 2018

- India is the number one priority for Saint Gobain, even more than China

- Over the last 3 years the company has spent all of its profits into capex in the country

India’s growth picture is as clear as glass for Saint Gobain - The Economic Times Feb 2018

- Expanding facilities in Chennai and adding another float glass line

- The expansion will lead to a 35% increase in capacity and take the total capacity to 1.2 million tonne

- The company is planning to offer more solutions for automotive and architectural products

- The Indian glass market is growing at 8%

- The Indian facility has become very big so some value added products are being exported to other countries as well

India'S Glass Market Growing Only At 8 Percent, Saint-Gobain To Focus On Automotive And Architectural Solutions, Says Ceo February 2019

Future Plans

- Creating more product for commercial vehicles like railways, off highway vehicles, trucks, city trains and tractors

- The company has spent Rs 600 crores on its new automotive plant in Gujarat which will cater to Maruti and have capacity of 2.4 million windshields and tempered glass each at full capacity

- The company continues to face huge competition from peers who also see demand rising and have been adding capacities to benefit from the same

News

- Government has initiated a probe into alleged subsidy in a particular glass category called clear float glass from Malaysia

- The probe is looking into how much is the domestic industry being impacted by subsidies and if found true would recommend countervailing duties on imports from Malaysia

- Companies in India filing the issue

- Asahi India Glass

- Saint Gobain

- Sisecam Flat Glass India

- Gold Plus Glass Industry

India Starts Probe Into Alleged Subsidy on Clear Float Glass by Malaysia October 2019

- Gautam Thapar (CG Power) a close friend of Asahi India CEO Sanjay Labroo who was his junior in Doon School and is also on board of BILT

- He is also a close friend of Tarun Tahiliani who is also in the promoter list of Asahi India Glass

https://www.outlookbusiness.com/the-big-story/lead-story/fall-from-grace-5399 September 2019

- Asahi India Glass forms a JV with some industry executives to acquire precision engineering business of Timex Group

- The JV will be named Scopofy Components Pvt Ltd.

Asahi India Glass forms JV to acquire Timex unit | VCCircle December 2017

- Investment of Rs 700 crores planned till 2022 of which Rs 550 crores will be for new plant in Gujarat

- In phase one plant will have capacity of 1.2 million units and by next phase the plant will have capacity of 2.4 million which will be completed by 2022

- The company intends to have a capacity of 8 million units by 2022

Asahi India Glass to invest Rs 700 crore in next five years - Times of India September 2017

- Asahi Glass to buyout Indian partner’s stake in the company to take a majority stake

- The deal is expected to happen between Rs 475-525 per share

- Both the promoters currently hold equal stake in the company at 22% each. The Indian partners hold the stake in multiple individual names

Asahi Glass in talks to buy out partner Labroo in Indian JV - The Economic Times September 2017

Disclaimer: No holdings in the stock. This is an introduction post on the company. Have started evaluating considering the recent fall in the stock price and the strong MNC parentage and leadership position in automotive segment. All the financials have been taken from Ace Equity database.