Hi ,

I have been investing for the last 6 years & i’m a silent reader in valuepickr for almost 4 years.I’m working in MNC & investing part-time . Most of my readings for indian market are from valuepickr

My portfolio is listed below

| stock |

category |

percentage allocation |

investment rationale |

Risks |

| HDFC bank |

financials |

10% |

consistent compounder, 20% growth YOY like clock work, low npa (historicaly), 50% of loan book is retail |

Covid impact on loan npa , credit card ban by RBI, tech outage |

| Manappuram finance |

|

8% |

No:2 player in gold finance (zero npa in gold ) , valuations looks cheap |

MFI book is risky + banks & fintech players trying to have pie on gold finance |

| muthoot finance |

|

8% |

No:1 player in gold finance (zero npa in gold ) |

banks & fintech players trying to have pie on gold finance |

| KPIT |

IT/ER&D |

14% |

self driving & electrification of automobiles is the emerging industry . KPIT have tie up with some of the big car brands in europe for ADAS, powertrain etc. only other listed firm in india is tata elxsi |

solutions have to be at par with Tesla, Google waymo for ADAS |

| intellect design(recent entry) |

IT/BFSI |

10% |

One of the few IT product companies listed in India . Saas + AMC (recurring revenue with not much expense) is already at 40% of revenue. IGCB & IGTB is in monetization phase. ISEEC is yet to win big deals. As intelect wins more deals , operating leverage will kick in & eps will grow very quickly . management guided for 10% revenue growth & 30% eps growth for next 2-3 years (my estimates are even higher). Global peers are trading at much higher valuations |

operating leverage will kick in only if they are able to win more deals . Licensing revenue means revenue growth is lumpy |

| Mastek (recent entry) |

IT |

4% |

Digital transformation + cloud . Acqusition of evosys ( oracle cloud player) helps in cross selling. Management is honest & transparent. |

?? |

| Borosil (SIP) |

consumer durable |

7% |

honest management . Growing opalware business + growing consumer durables business . Looking for 15-20% CAGR |

Covid impact & lockdown on business |

| V guard |

consumer durable |

7% |

growing electical/ electrical business. Entry into new business segments in consumer durables every year (water heater, cooktop, air cooler etc ) . Expecting 15-20% cagr |

high competition |

| granules (recent entry after correction) |

|

4% |

bulk drug manufacturer. Trying to have formulations which should improve margins going forward.management looking for 20% revenue & PAT growth . PE looks cheap compared to growth projections |

raw material price increase on bulk drugs |

| US portfolio |

|

|

|

|

| Alpahabet |

|

15% |

search +youtube + hardware+ playstore is contributing to the earnings now. 3rd biggest player in cloud & growing fast (40% almost) but now running at a loss. Google Cloud should turn profitable in a few years.Lot of unmonetized assets like WAYMO ( self driving) , google maps , android , fitbit acquisition. Leading player in AI (Deep mind) |

?? |

| salesforce |

|

7% |

No :1 cloud CRM player . Plans to grow revenue by 100% by 2025. cheaper compared to other cloud players in P/S ratio because of nearterm impact on earnings due to slack acquisition |

Lots of acquistions by salesforce which is a major risk |

| wisdom tree cloud etf ( recent entry) |

|

6% |

cloud is the growing segment in IT |

valuations are very high |

please give your views & suggestions .

Thanks

Arun

Hi Arun, Thank you for sharing. I am also in the same boat. Just a quick question, how do you invest in the US Stock Markets?

Thank You,

Karan Khanna

Hi Karan , You can start a trading account through ameritrade or etrade for investing in US.

I’m investing through etrade as i also have a corporate account with them (for RSU).

Groww also started US stock trading , if my information is correct.

1 Like

Quarterly result update:

Mastek :

• 40 new clients in Q1FY22 . Total client count was 651 (LTM) as compared to 639 (LTM) in Q4FY21.

• 12 month order backlog was Rs 1,177.7 crore ($158.4mn) as on 30th June, 2021 as compared to Rs 1,130.4 crore ($154.6mn) in Q4FY21 (constant currency growth 2.1% Q-o-Q & 45.5% Y-o-Y)

• Net Cash balance is Rs 702.9 crore as on 30th June, 2021 as compared to Rs 588.6 crore on 31st March, 2021

• 510 headcount added during the quarter (net of attrition)

Disclosure: Added more (1%) on day after result at 2520 range . 5% of my pf (avg price 2219)

KPIT :

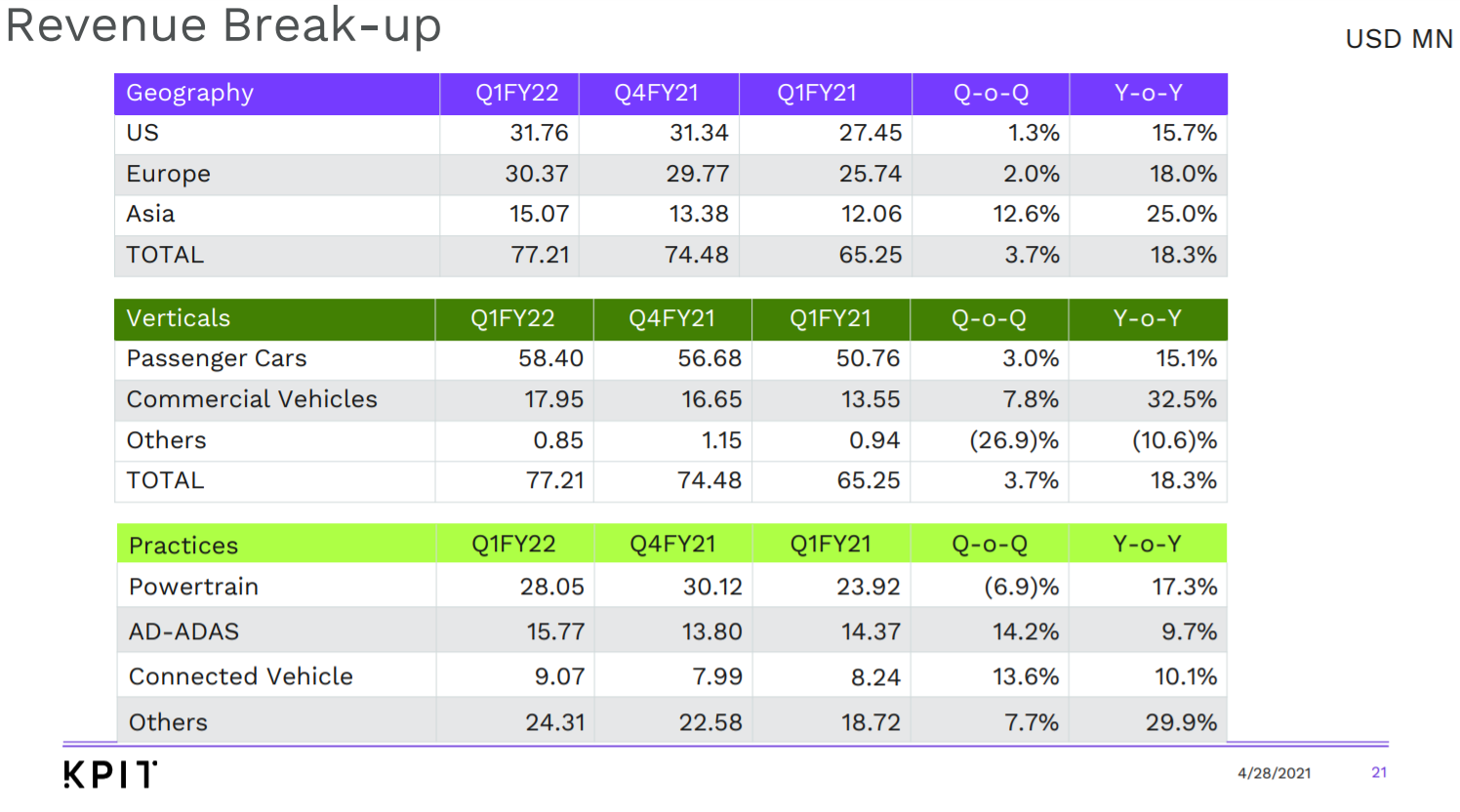

Q1FY22 USD Revenue grows 18.3% YoY & 4.3% QoQ.

PAT growth 150 % YoY & 14% QoQ.

employee count increased from 6564 to 6806 YoY (proxy for growth in service IT company)

Guidance : mid teens revenue growth & 16.5% - 17% ebitda margin which is significantly higher than 14.3% & 15.7% margins in Q2,Q3 FY21… which means PAT should grow by at least 25-30% in next 2 quarters YoY.

Growth across business segments:

Disclosure: Trimmed 35% of my allocation to KPIT in last quarter. 9% of my pf . Avg price 78.

Intellect:

revenue up by 18% YoY, EBITDA up by 48% YoY , Net Profit up by 73% YoY

License Revenue up by 32% YoY, AMC Revenue up by 8% YoY, SaaS revenue up by 102% YoY.

AMC + SaaS at ~40% of revenue (revenue recurring every year without much work)

10 Digital led wins including 5 large Digital Transformation deal wins.

Guidance:

Revenue: Mid-high teens revenue growth

Earnings : 25-30% growth trajectory

Ebitda Margin : 25 to 30%

Disclosure : 12% of PF . avg price : 742

1 Like

Exited KPIT completely as valuation seems stretched around 650 during January end(was exiting partially from 240 onwards. (looking back exiting KPIT at 240 onwards was a mistake . i was early … but gradual sell off as well as gradual buys help me average out the fluctuations & help me capture the upside to some extent . 50% of my stake was sold in january at 650 when i thought valuation was stretched much beyond i was comfortable).

Adding money to intellect design but very slowly as it crossed my 10% limit . Max portfolio allocation limit is 15% & intellect is inching slowly towards that. So buying only during significant corrections like that seen in early march .

Started positions in US facing etfs:

Motilal oswal nasdaq100 : 8%

MAFANG : 4%

US equity has corrected more than india & is now comparatively reasonably valued .Will add more if there is more correction.

Started positions in FB around $220 …

I feel FB is cheap even with IOS headwinds .

FB Positives :

** Buybacks have accelerated & they will be buying back at these cheap valuations.*

** FB has a FCF of $40 billion even with heavy spending on metaverse & virtual reality & apple headwinds.*

** Whatsapp monetization not yet started (they can easily convert it into super app + payment gateway + ecommerce etc)*

** Instagram is the most popular social media website for millenials & GenZ…*

** Fb is morphing into a ecommerce site (similar to craigslist) with facebook market place & FB groups .*

** optionality with metaverse & VR/AR ecosystem*

cash position : 20% of net worth ( My networth is fully in equity + cash + RSU from company i work… very bold … keeping significant portion in cash to prevent from being going bankrupt  )

)

(waiting for correction on nasdaq otherwise will keep in cash as buffer).

Posting after so long.

Nothing much changed in Portfolio .

New Additions :

-

PI industries over the last 1 year (avg ~ 3400).cheap due to news on pyroxi molecule (38% revenue) competition . PI is diversifying with new molecules as well as into pharma.(~8% of portfolio)

-

Narayana hrudayalaya over last 2 months (avg ~ 1250). Somehow i missed the hospital sector .Narayana will have muted growth over next 2 years but has one of the best promoter (Dr. Devi Shetty).Will average this stock up/down over next 2 years.

-

ICICI bank (avg ~950). The banking sector seems very cheap

-

PPFAS (over last 9 months (NAV avg ~62) . Only active mutual fund i have invested . Best value investors in India at present IMHO.

Selling KPIT 2 years ago seems wrong decision in hindsight .

US portfolio (including RSU) went through a rollercoaster.

Averaged NASDAQ100 index funds/MAFANG through trough but in hindsight couldnt put enough money to backup the conviction (~15% of portfolio)(no new investment after march 2023 due to change in tax rules)

Meta was down big time but went through pain (couldnt add more at lows since i was fully invested) & now it seems good days are back .

Indian portfolio

Added more HDFC bank over last 6 months (avg ~ 1470). HDFC merger seems painful & may take few quarters for EPS growth.

Intellect & Mastek are growing at decent pace as expected. Valuation seems a bit stretched though.

Borosil had few hiccups this year but should pickup now .

V-guard margins are impacted in last 2 years… should recover in this year .

Gold finance companies (Muthoot & manappuram ) struggled last few years due to high competition from banks & it seems worst is over .

Exited Granules recently with decent returns.

CASH : 25% of portfolio