It highlights the importance of experience and prudence in the MFI business.

@DEBASHISH Sir I wanted to get your views on Arman, especially considering the current industry headwinds. The company has been known for its prudent approach to lending, but this time it seems their loan disbursements are growing despite the downturn in the industry. Additionally, their PAR (31-90) has been rising sharply, which raises some concerns.

The valuation has also corrected significantly recently, which has caught my attention. Given these factors, I’d really appreciate your perspective on whether you see this as a potential buying opportunity, or if there are risks that we should be mindful of. If you see value in it, I’d certainly be interested in exploring it further on my end as well.

Looking forward to hearing your thoughts

7 Likes

5 Likes

Book Value per Share: 824

Price/Book: 1.5 (lowest in last 10 years and similar to Covid bottom)

Debt/Equity: 1.5

GNPA: 3.74%

NNPA: 0.64%

Credit Cost: 99 Cr (4%, not annualized)

I am tracking this company from last 7 years. The company has frontloaded the provisions for NPA. I know the working style of Alok Patel (CEO). The biggest coushion is that D/E is very low. As and when cycle NPA cycle turns, a sharp recovery will be seen in lending because of low D/E.

Industry wide corrective measure have been started from last 2 quarters, which may start yielding results after next 2 quarters.

This is a heaven for contrarian crowd.

04/01/2025

11 Likes

Hi, from 30 August 2013 till 29 May 2014, the Price to Book of Arman Financial is being shown ranging between 0.4 to 0.5 in Screener.

From 1 April 2005 till 11 October 2013 (Almost 9 Years), the price reached from Rs 6.50 to only Rs 16.5, as per Screener.

If a full fledged recession occurs (I hope not), then there might be a lot of downside possible in the entire unsecured microfinance sector.

Disclosure: Views are personal and only for educational purposes. As of today, no personal holding in Arman Financial.

3 Likes

mfi industry was not popular during 2005, today the situation is different. once the cycle turns, you will see the difference. valuation is favourble, limited downside.

5 Likes

I have pointed some reasons earlier… That will work in favour of arman in tough time.

They created pool of good customers, means if customers have willingness to pay then there is no problem at all… They will renew the loan simple.

Disc. Not invested

1 Like

I didnt see your message earlier and hence my apology for delayed response .

Your return on share depends on at what price you bought (or kept adding ) and your allocation % .I have been invested in Arman for 8 years now .Have most of the time added during fall hence inspite of Arman down from all time high by more than 50% + my CAGR return on Arman in 8 years is 31% pa+ .I even added during this fall.

Coming to MFI cycle no one can predict when the cycle will turn .This time the problem is man made wherein the leverage at customer end is very high .RBI is after MFI ,on top of it the players have started becoming cautious and hence the cycle will rectify in few quarters .Hence if we take a longer view of 5 or 10 years( in my view its a cyclical industry hence have to have longer time horizon so as to NOT to play or project the cycle accurately in shorter time frame )we will make lot of money as bcos :

-

The PE & PBV is at its lowest in my investment horizon since I have been tracking & invested for last 8 years

-

Given Promoter background ,they know how to underwrite credit better than any MFI and hence would come out one of strongest in this cycle

3)They have raised money and DONT need money for next 2/3 years

4)If we do REVERSE DCF assuming we want to make 20% return pa for 5 /10 years at EXIT PE OF ONLY 12 ,market is assuming PAT growth of 5 % & 8% pa for 5/10 years -where in this market we will get this type of valuation ??

- Hence I am taking a contrarian view and will further buy

Discl : My views on Arman is biased bcos of my holdings ,please DO YOUR OWN due diligence

41 Likes

I remember everyone have been so bullish in this stock for last one year. Why the shareholding of promoters, FII and DII reducing continiously for last 1 year?

2 Likes

Yes, the last two quarters have been challenging. However, their profit has grown significantly from ₹3 crore in 2013 to 32, 94,&174 crore respectively over the past three years—a multifold increase. The trailing twelve-month (TTM) profit stands at ₹90 crore.

There hasn’t been any significant change in FII, DII, or promoter holdings, apart from some reshuffling in FII, which is a regular occurrence. And i don’t see not a much of a change in public holdings as 20.1% is already with HNI / Big institutions.

Here’s the percentage change in public holdings for each quarter:

| Quarter | Public Holding (%) | QoQ Change (%) |

|---|---|---|

| Mar 2022 | 67.52 | — |

| Jun 2022 | 67.00 | -0.77% |

| Sep 2022 | 66.82 | -0.27% |

| Dec 2022 | 66.76 | -0.09% |

| Mar 2023 | 66.89 | +0.19% |

| Jun 2023 | 67.05 | +0.24% |

| Sep 2023 | 68.76 | +2.55% |

| Dec 2023 | 62.05 | -9.76% |

| Mar 2024 | 61.41 | -1.03% |

| Jun 2024 | 66.56 | +8.40% |

| Sep 2024 | 68.01 | +2.18% |

| Dec 2024 | 71.44 | +5.04% |

| • | The biggest drop in public holdings was in Dec 2023 (-9.76%), possibly due to increased institutional buying. | |

|---|---|---|

| • | The highest increase happened in Jun 2024 (+8.40%), indicating a rise in public shareholding. | |

| • | Overall, public holdings increased significantly in 2024, reaching 71.44% in Dec 2024. |

I noticed a substantial expense under “Impairment losses on financial assets.” If anyone can provide insights on this, it would be helpful. My assumption is that it relates to non-recoverable assets.

As Debashish mentioned earlier, the MFI sector is currently facing a tough phase. However, market dynamics can shift unexpectedly, and the sector may recover sooner than expected.

As long-term investors, it’s important to stay informed about developments in the stocks we hold. However, a few weak quarters shouldn’t make us overly pessimistic about a company’s long-term potential.

Someone planning to enter in the stock can wait for one or two quarter to decide.

Note: Invested and Not biased, clearly telling everything from the experience gained over years. No recommendation pls.

3 Likes

In my opinion, MFI is a terribly slow-growing business because you have to always find new customers to lend to. The lending amount is very little, and you have to have a lot of feet on the ground for both collection and forward lending. Highly cyclical business as the customers can migrate to other parts of the country without notifying the lender; this business always gets affected by elections, uneven monsoons, and whatnot. Not to mention that every Tom Dick and Harry is doing microfinance nowadays; hence, the massive competition and unsecured nature of this business add a big risk on the top.

With this in backdrop, you just can’t make an institution out of it. Do you know any financial company that is worth calling an institution and is just doing microfinance? I believe MFIs existed since 2010 or so, and none of them are able to scale to a significant level. At some point in time, everyone has to pivot to a more stable and sensible business. With the current pain faced by the sector, I am quite skeptical about bank lending to MFIs.

Before deciding on what company to invest in, one should decide whether to really invest in this sector at all. In my honest opinion, MSME financing is a real opportunity, and all of these MFIs are somehow trying to build a book in that.

Disc: Not invested

5 Likes

I completely understand the skepticism around the MFI business model, as it indeed comes with high operational costs, customer churn, and cyclical risks. However, I’d like to offer a broader perspective:

1. Microfinance is a Slow-Growing Model, but It’s Essential

Yes, MFIs require constant customer acquisition , but they serve an essential financial inclusion role by catering to the unbanked and underbanked population, which mainstream banks often avoid.

Despite the low ticket size, the model works on high volume & strong repayment discipline (~98% collection efficiency in top MFIs).

2. Scale & Sustainability – Can an MFI Become an Institution?

While pure-play MFIs have limitations, several institutions have successfully scaled up:

Below are few examples:

• Bandhan Bank – Started as an MFI and became a universal bank with a ₹1.5 lakh crore+ loan book.

• CreditAccess Grameen – India’s largest NBFC-MFI with a ₹21,000+ crore AUM.

• Ujjivan SFB & Equitas SFB – Transitioned into small finance banks to achieve scale & stability .

MFIs can evolve into larger financial institutions by diversifying into MSME, housing finance, and other lending verticals.

3. Competition & Unsecured Lending Risks

Yes, competition is rising, but experienced MFIs mitigate risks through:

• Group lending models ensuring social pressure for repayments.

• Regional expertise & branch networks for better collections.

• AI & data-driven risk assessment to improve credit quality.

Not all microfinance is equal – well-run MFIs maintain lower NPAs than many NBFCs in unsecured lending.

4. Arman’s Positioning – Why It Stands Out?

Hybrid Model – Unlike pure MFIs, Arman Financial Services also operates in MSME lending and vehicle finance , providing a diversified revenue stream .

Well-managed risk – Strong underwriting and collections have helped Arman maintain lower NPAs than industry averages until good quarters.

Growth beyond MFI – Their MSME & two-wheeler lending business is growing faster , reducing dependency on microfinance alone.

5. MSME vs MFI – The Real Opportunity?

Agree that MSME lending is a huge opportunity, but most MFIs already recognize this and are actively expanding into it.

Arman’s MSME business is expected to scale significantly, making it a well-balanced financial player rather than just an MFI.

5 Likes

While you maybe right about the tough aspects and sustainability of the old MFI model, we need to see where this lending segment is going. Ever since DEMON, the old JLG model has shown its weakness in times of widespread stress in the economy, whether the catalyst is exogenous or endogenous, micro or macro doesn’t matter. The group liability breaks down when everyone is under stress.

The JLG model was very similar to the new Credit card (CC) business, the lenders would start newly acquired customers with very low amounts of credit to gauge their repayment ability, motivation and discipline. Once a repayment relationship was established the good customers were graduated to an expanding relationship.

Today the JLG model has just become a funnel for separating the wheat from the chaff, the graduating customer after their 3rd or 4th cycle moves on to bigger individual, business, and home loans. I would hazard a guess that those who graduate from the JLG model are more entrepreneurial and industrious and this helps in growing the relationship. Yes, there may be a loophole here for evergreening by the lenders but it seems highly improbable that a lot of relationships graduate from an 8k credit to an 8 lacs loan amount on just evergreening. If it does, then this would just be a big Ponzi scheme by the lenders in pursuit of valuations.

There is a lot of competition for prime lending, and the middle segment, even for the bottom segment the competition is heating up. There is value to be found/grabbed/created here but it’s just harder. There is also the risk of these bottom-up lending institutions painstakingly growing the relationship to a bigger size and bigger banks just taking the cream away when the time is right with no investment. Access to credit bureau data just levels the playing field for all lenders and the database is only going to get more extensive as the years pass.

For these lenders to become institutions, they need growth, growth is fueled by capital raising, and capital raising requires trust, confidence, and stable ROA to fuel a healthy PB above 1 so that each capital raise is value accretive from the start. Unfortunately, when the sector was initially listed everyone was enamoured by the growth and high ROEs and granted even 5x valuations to MFIs. At one point Bandhan was the most expensive bank in the world. Now these lenders even struggle to a steady state PB of 1.5. The reason is that the market is unsure of what the full cycle ROA/ROE for this business is, and unless the investors get a concrete idea of this they won’t have the confidence to invest in these lenders for the longer term and impart valuations required for institutionalization.

Currently, the sector is indeed a long shot, if things go right, there will be lots of value creation for the believers and if not at current undemanding valuations the risk of capital loss is low and at worse one may get away with low returns. An asymmetric bet if you will.

9 Likes

Arman Financial Basis for Confidence in Bottoming Out:

-

Improving Credit Cycle Trends: Improving trends in the credit cycle during December 2024 and January 2025, with stabilizing 0 DPD (Days Past Due) flow forward rates.

-

In December 2024, the 0 DPD flow forward rate was 98.03%, and in January 2025, it was 98.15%.

-

The 0 DPD flow forward rate in February 2025 was about 35 to 40 bps ahead of the previous month on a month-to-date basis.

-

CGFMU Enrollment: Arman is enrolled in the Credit Guarantee Fund for Micro Units (CGFMU), providing a guarantee cover for disbursements.

-

Approximately Rs. 200 crores of disbursements in quarter three have a guarantee cover through the CGFMU.

Future Expectations:

-

Potential Bottoming Out: Management feels that they have “probably reached the bottom”.

-

Expected Improvements: Improvements are anticipated from Q1 onwards, though it will take a few quarters to fully recover.

-

No Pushing Forward: The management has stated that they are not pushing anything forward for FY26.

-

Focus on Disbursement Improvements: While growth may take time, disbursements are expected to improve in Q4.

-

Long-Term Strategy: The company remains confident in its ability to navigate industry challenges and position Arman for long-term sustainable growth.

9 Likes

Bandhan likely to see more pain in next quarter as per reports. Not directly link to Arman, but gives rough idea how other MFI are going to perform in next quarter. Disclaimer: Holding Arman, Credit Access.

2 Likes

Can anyone share their view on the recent sale of stressed loan portfolio of around Rs 186cr for a consideration of Rs 37cr. Will this be considered as a balance sheet write-off which will not reflect on P&L or this is the loss the company has to book in this quarter?

I believe most of the amount has already been provisioned in the balance sheet. If the actual amount exceeds the provisioned amount, it will be written back, and vice versa.

Also, ques for experienced folks- did Arman do a similar write-off during covid time and other tough times or this is the first time its happening? If first time- then it’s a bigger worry tbh

2 Likes

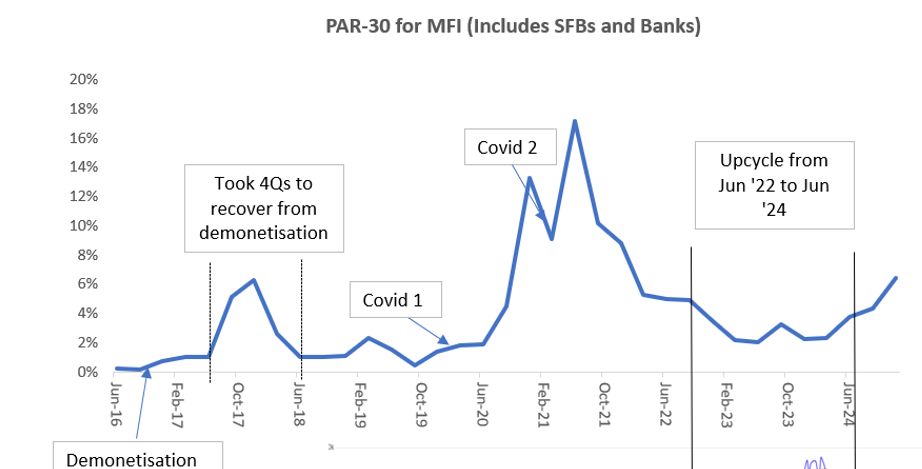

This seems like an attractive valuation to enter the stock. Historically has traded between 3-3.5x PB and currently available at 1.6x.

The loan tenure is ~24 months for MFI loans. In the current downcycle, weakness was visible from April '24 onwards, so we are halfway into the cycle. Historically, it has taken 3-4 quarters for things to improve.

Source : Sa-dhan

- AFSL has never reported a negative RoE annually since it started the MFI business. Despite the credit costs being high in the last 3 quarter and 25Q3 being negative RoE, we can expect things to be better than what they were during covid. So the Book value is preserved.

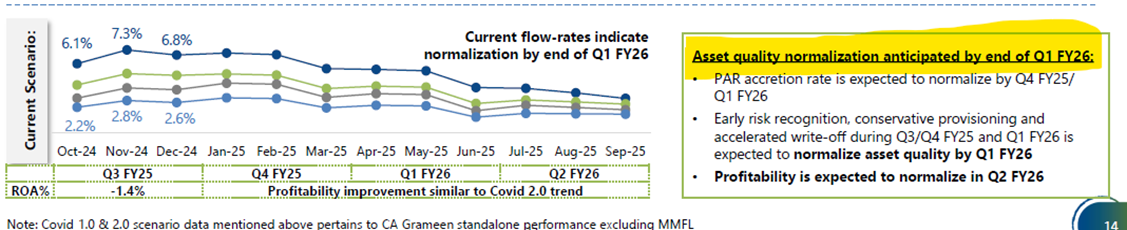

- CreditAccess management expects things to improve from 1Q26.

Source: CreditAccess Grameen 25Q3 pres

-

A recap on what caused the crisis:

Overleveraging

106% CAGR between '22 and '24 in no. of ‘other’ lenders which should include fintech companies etc.

Source : Sa-dhan -

Despite aggressive provisioning in the last 3 quarters, the company maintains a CRAR of 39% as of Dec '24 and 1.35x Debt/Equity, so sufficient buffer for further provisioning, as well as doubling the AUM once the cycle turns.

-

There could be another 1-2 quarters of weak nos. If going forward the credit costs are in the 2-2.5% range for MFI industry (vs 1% pre-covid), maybe it will not get lofty 4-4.5x PB multiples. However, it does look attractive as things stand.

Discl : Invested

18 Likes

Q4FY25 Conference Call Summary

- Namra had lower profits y-o-y, also showed marginal loss in the Q4. The lack of the performance was due to higher provisioning.

- They believe the growth in the microfinance sector will only be back when the industry deleverages and adapts to the changing rural economy.

- Two strategic changes

- Completely separate the credit and recovery function from the branch operations.

- New structure called BCMs who will control approving or rejecting loans. There is a 3x difference between early delinquencies in BCM originated customers versus non-BCM ones.

- Traditionally, MFI worked on the foundation of JLG models and population-based credit decisioning frameworks, however, the data shows that it doesn’t work adequately. Now they are going to evaluate each customer individually which helps them assess the loan quality in a more granular manner.

- This also helps eliminate the issue in MFI where same person has to decide the disbursement as well as the approval of the loan.

- This approach will increase the operating costs which is better than having higher credit cost. Opex cost will increase by 1%.

- Field officers will continue to handle regular collections and early stage delinquencies while higher delinquencies will be taken over by the Recovery officer.

- Currently implemented in 140 of the 391 branches, the remaining will be covered by Q2FY26.

- The asset quality of loans disbursed under the new system have shown encouraging numbers.

- Completely separate the credit and recovery function from the branch operations.

- 34% of their MFI loans are covered under CGFMU with more covered each quarter. They might drop CGFMU for their own credit risk management system, if the internal credit performance becomes stable.

- Fully compliant with the new guardrails as of March end. It is a temporary fix and not a long term fix for the problem.

- Zero bucket collection efficiency for the quarter stood at about 98.5% and improved to 98.8% in March, showing an improvement over Q3.

- The dip in repayment rates has stopped, Zero-DPD bucket rates went from 97.3% in November to 98.8% in March.

- Not yet confident of strongly growing the MFI book, will revaluate it in the coming quarter. No ROE guidance right now either. The other businesses which now make 30% of the loan book, they are confident in it’s growth.

- 1% of their book is exposed to Karnataka (stable currently). Rajasthan and Gujarat are showing the maximum stress in the book.

- Growth is not the priority at this point. They plan to maintain the current portfolio size for the next 2 quarters, will focus on growth post that.

- Industry portfolio has gone from a high of 4.5 lakh crore in December to about 3.7 lakh crore in March due to the different attempts to deleverage the segment (by guardrail for example).

- 76% of all MFI loans disbursed went to borrowers with credit scores of greater than 600 which are considered top customers.

- 22% rejection rate from inquiry to actual disbursement in MFI and 75% for MSME for March.

- There hasn’t been any income growth in rural economy while the debt in each household has grown by 40-50%

- Absolute number in accelerated provisioning will decrease however due to denominator effect, the % provisioning may look optically higher going forward.

- 23% of their MFI customers have 3+ active lenders, newer loans have been skewed towards lower X lenders at household level. They are not tracking this number too much as they have not seen much correlation.

- Peak attrition rate of 68% which they want to bring down to 40% by H1 of the FY.

- Industry wide slowdown in April and May due to Guardrail 2.0, Zero-DPD stabilized but definitely not improving as expected.

- Sold 185 crores bad loans to ARC which they valued at ~35 crores. 95% of the loans have already been written off so any recovery will straight go as direct income.

- Reasons for sharp opex rise include more general staff hiring, increase in travel allowance, more incentives, hiring recovery staff and BCM which are more expensive, disbursement slowdown.

- Only 5-6% of the MFI graduate customers are MSME customers. They might launch a pilot in late Q1 or Q2 for individual loan product for MF customers.

- They expect standalone profitability in MFI segment by Q2 FY26 but not any guidance.

This was a fantastic and insightful concall. My notes won’t do any justice to the different aspects discussed. I will highly recommend everyone tracking this company to go through the concall atleast once.

Disclaimer: Studying, tracking very closely

31 Likes