Recently, tax notice have been given to subsidiary (narma) of arman financial. Want an insight on governance issue and on integrity of promoters/management. Are they shareholder friendly??

Views will be appreciated.

Recently, tax notice have been given to subsidiary (narma) of arman financial. Want an insight on governance issue and on integrity of promoters/management. Are they shareholder friendly??

Views will be appreciated.

Does anyone have any hypothesis on recent price fall of the stock?

The Company will challenge the same based on strong

merits by way of filing its reply/ submissions, before the

relevant authorities. There is no impact on financial,

operation or other activities of the Company due to this

Order. The impact will be limited to the extent of final tax

liability as may be ascertained along with interest and

penalty, if any. This is as per the statement.

Rating is upgraded by CARE to A- from BBB+.

Well a 35% correction from recent highs. This is despite ratings upgrade. Is the tax notice really weighing down on the stock? Any other concrete reasons apart from the tax notice?

well this is purely my personal view , i may be totally biased.

I like the credit/lending business because of many reasons ,i think we all write 10 of them.

First when any country grows at 8% the biggest beneficieries will defenitely be lenders.

Second thing is the overall perception of indian PSU banks is changing , look at BS of all PSU banks in last 3 yrs.

Third thing is , The perception of RBI towards NBFC is also changing, look at the last 12months circumstances.

and also try to understand the kind of practice this NBFCs are doing.

Fourth factor is JIOs entry which impact may be less but not negligible.

Fifth, if u understand problem of CD ratio, the only solution is to go to villages and increase ur customers base, and obviously lend to micro finance customers.

tell me who will be looser of all this factors… …

Disc. Not invested in arman Holds Canara bank , JK bank & BOB

Market did not react positively even though the stock was moving sideways for some time. Can experts comment what could be concerns of market?

Disc: took a 0.7% position today and thinking pf increasing this high growth low NNPA NBFC

Overall, results do seem good. They have met guidance across all key metrics.

Only 2 minor concerns:

Note - Tracking as a potential investment candidate. So my views are biased.

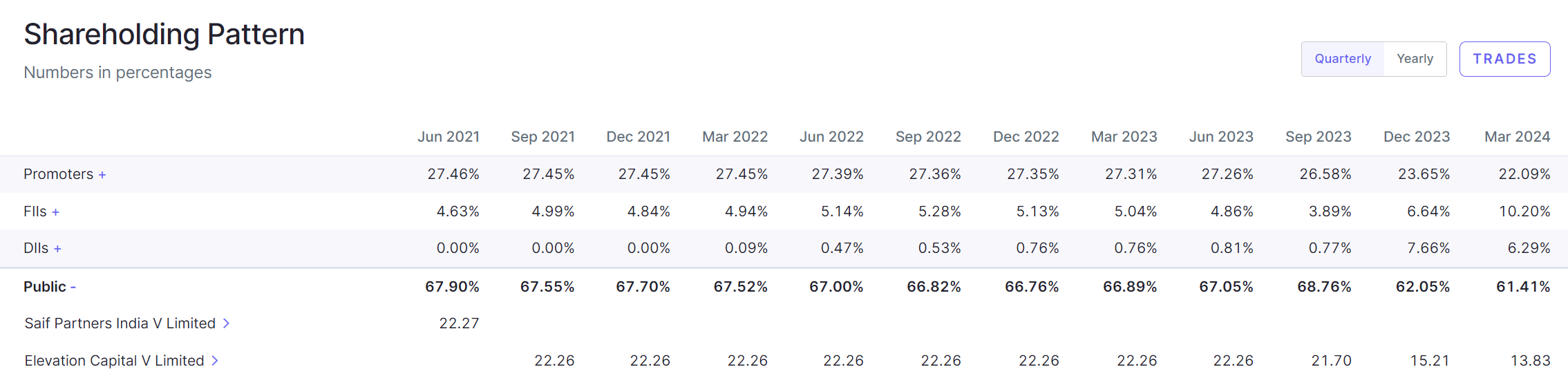

I believe Elevation Capital that owned ~20% of the company is winding down the fund. If they’re selling such a large stake via the open market, the stock will remain under pressure until they fully exit.

Outside of Arman, all MFI companies have corrected some 30-40% off highs from last year including Spandana and CreditAccess. I think a lot of people are waiting to hear about regulations from the RBI, and there have been concerns about asset quality in the industry.

I’m using this as an opportunity to add Arman at 2x FY25 BV, and Credit Access at 2.6x FY25 BV, but we’ll only know from numbers / channel checks if the best of the asset quality this cycle is behind us.

D: invested, transactions in the last 30 days.

Just check the history why this PE funds not holding their stake , why they r playing the rotation game.

1St why incofin sold it’s holding when they knows everything, better than any of us.

Correct me if I am wrong but my clear perception says now it’s purely aaja fasaja scheme from both PEs side and promotors side.

I already warned about the basic principals of business…

Disc.sold earlier.

according to me its not natural to exit the company at fraction of 1or 2years , look at the really solid businesses like warren buufet was invested in coca cola before our birth and story still continues, RJ invested in titan since 23 years and still holding 90% of his holding…

but the problem with arman is its invstors and promotors dont have confinent then how we small invsetors can jump on it…

conviction nam ki bhi koi cheez hoti he bhai…their promotors selling at every rise, PEs playing their own jugglery, MFI indutry itself suprise with numbers Arman growing ,

MAS ,Credit access yebhi samjte he business ko ,lekin grow sifr yahi kar rha he. or promotors bech rhe he…

Arman has the highest ROE amongst MFIs and this trend has more or less been sustained over the years. Can’t compare with MAS, which is more of a wholesaler for MFIs

Growth is more or less in line with CA and Satin, and on a smaller base. Arman grows its loan book conservatively, this has always been the case since Demonetization

Recent Growth has been driven by geographical and product expansion, into UP/Bihar new geographics and into MSME loans away from MFI, and now growing into LAP and Individual business loans. Management has been giving clear sequential numbers for each business in transcript and presentation.

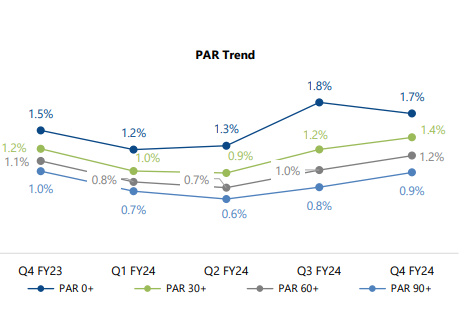

In terms of trends, you see PAR 30-90 has moved up for all MFIs. Below is trend for CA Grameen. This was predicted by Arman management 2 quarters ago

NIM is higher for Arman and cost to income ratio is lowest amongst Satin, CA

What needs to be watched is GNPA/NNPA

Saif has been invested since 2018, it’s very natural for PE funds to exit after a few years. Mud slinging on companies without any facts is something that should be avoided on this forum. It’s a cyclical business which will go through its own ups and downs. Doing 2 successful fund raises over last 18-24 months gives them enough capital to grow aum till 5k crores.

Disc: holding since last 3 years. Biased

Hi, I’m new here so sorry if I’m asking a stupid question, but how come a Lending business is cyclical? Aren’t they supposed to show secular growth? That’s what I believed that it’s an ever growing business which will be slowed down only for sudden rise in NPAs as a major setback.

Asset quality cycles

Nim cycles

Asset side cycles come from asset quality issues. Can be due to any macro event like Covid or demonetisation.

Liability side cycle will lead to Nim contraction. Can be due to tighter liquidity conditions. Eg: reduction in supply of commercial papers in 17-18 post IL&Fs or current challenge in deposit growth.

Check armans investor presentation and see the GNPA cycles. Business has done well over 2-4 year time gaps, but such cycles will be there in most of the financial cos

So after rate cuts the NIM will improve for lending business ryt? Because the NBFCs will be able to borrow on low rates and will get better margins in retail lending.

So by judging the collection efficiency numbers, what is your assessment for the credit cycle? Collection efficiency is down almost 150bps from around 98% to 96.5%ish. Can this be viewed as credit cycle turning? Or we should wait for a few quarters to actually see that in numbers? Thanks!

Can someone please help me understand this. What is the limit upto which a lender is allowed to lend? Is there a threshold D/E that these companies cannot breach?

QIP will lead to dilution of earnings inflating the PE of the company. Should we ignore PE ratio in finance companies.

Any help will be highly appreciated.