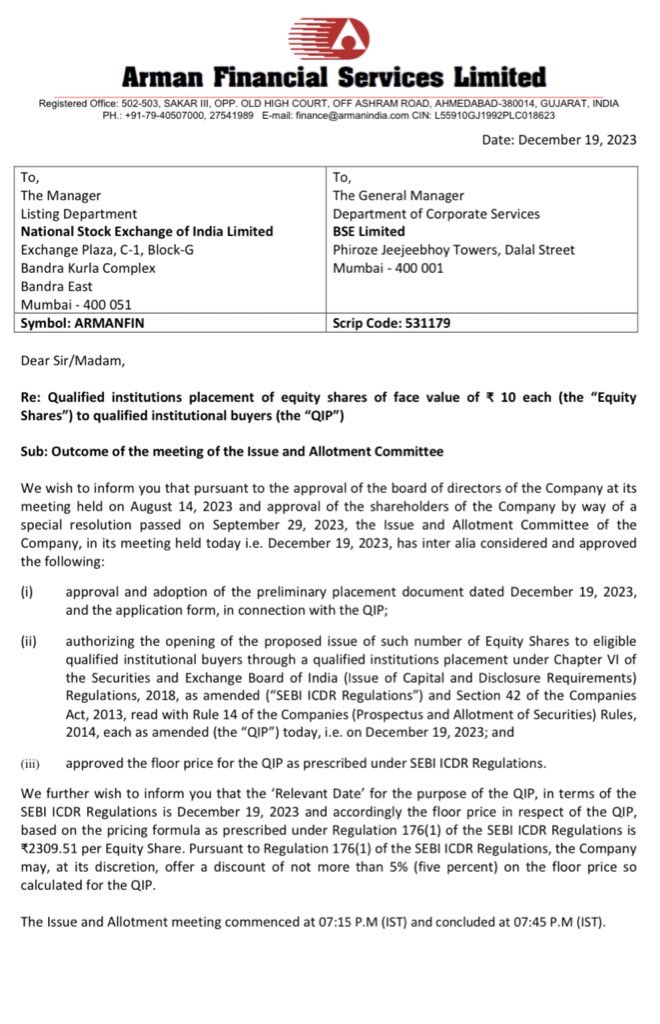

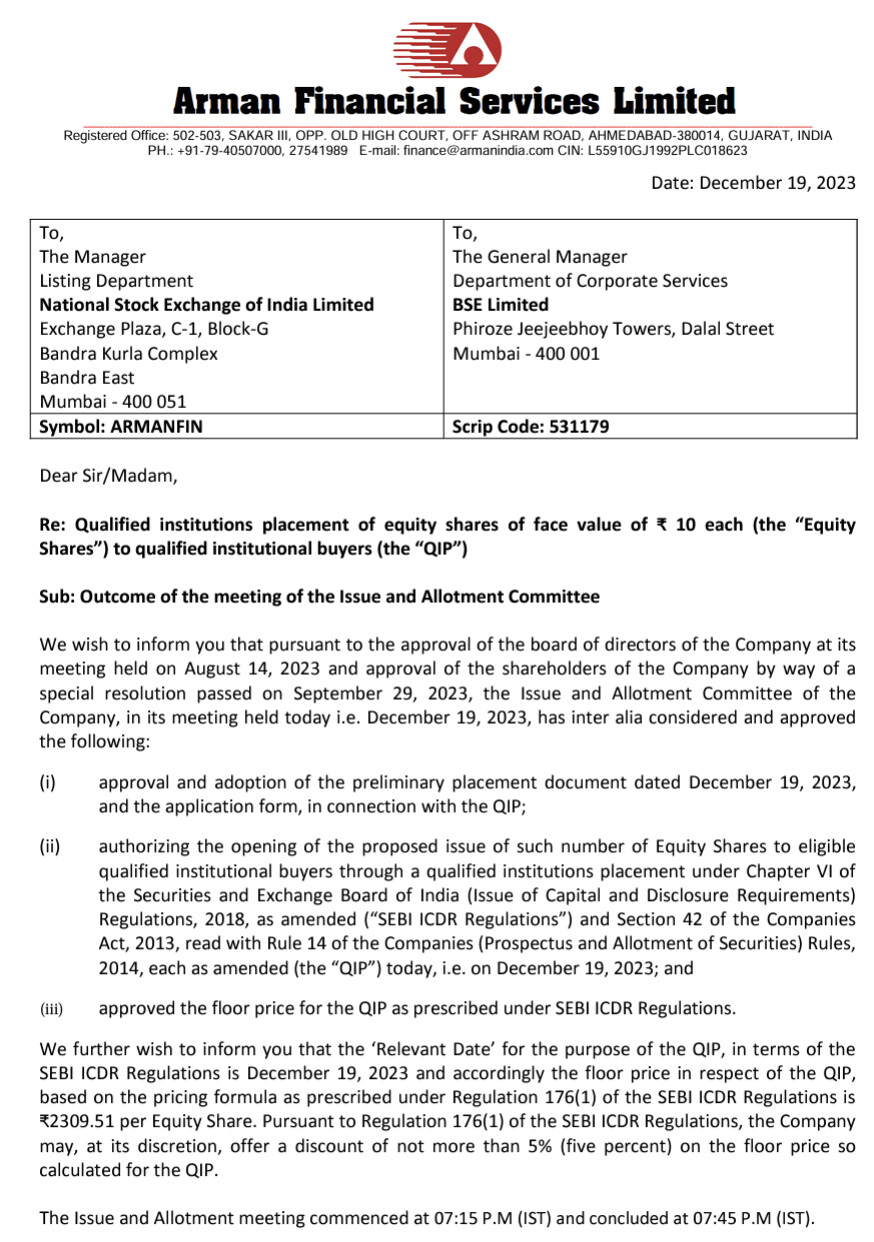

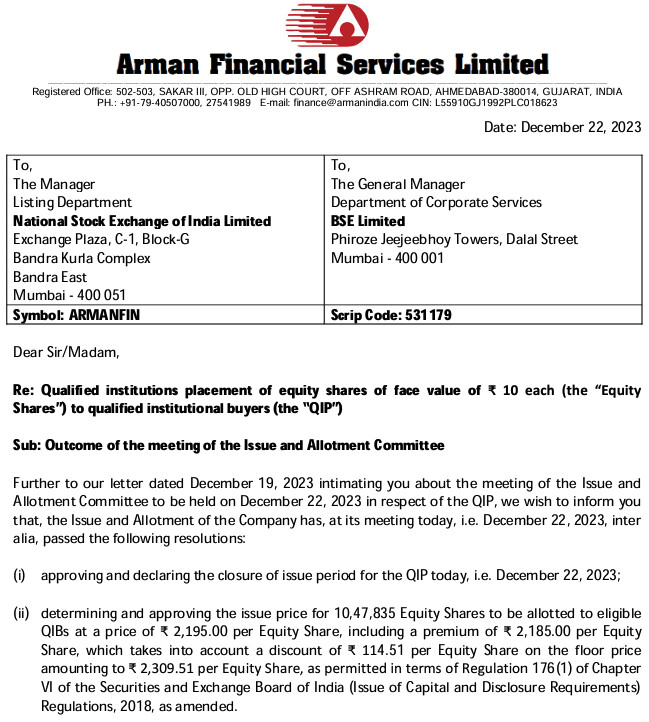

QIP announced by Arman Financial

1 Like

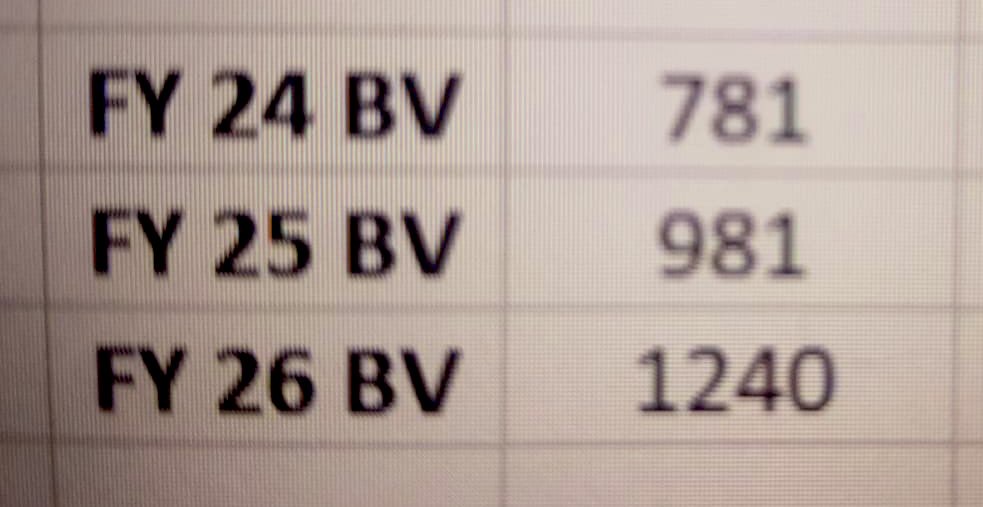

Book Value per share jump

https://x.com/ishmohit1/status/1737141255413416181?s=46&t=Am0XGIAZR4xg3ZqcxYwxeg

1 Like

whats the implication of this QIP on company’s future earning growth and eps? can someone please throw some color to it?

This increases their equity. A lender is allowed to lend many times more money as compared to its equity. For example before QIP their equity was around 500 crores. And they were lending more than 2000 crores. So now QIP has happened for 230 crores. This would allow them to lend more than 3000 crores now as their equity would go up to 730 crores.

And the more you can lend, the more you can earn. That is how QIPs help lenders.

8 Likes

Recently, armans promoter are selling their shares quarter on quarter. Can anyone throw some light on this issue and why they are selling despite perfect quarter results and very strong future guidance.

2 Likes

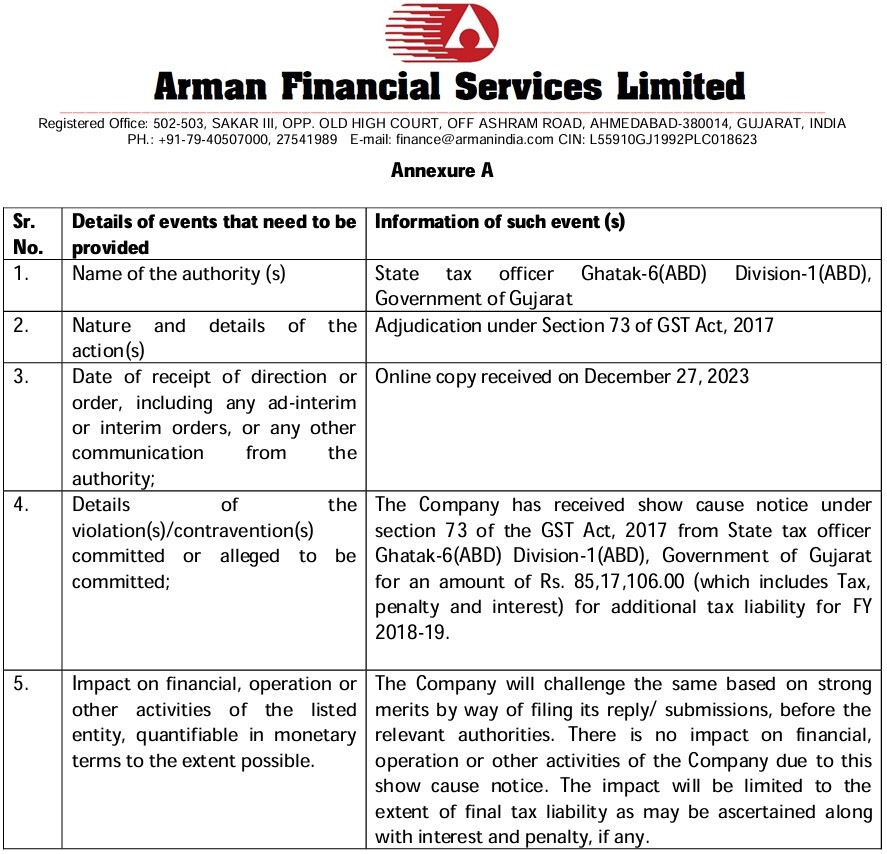

Thanks for sharing. The GST demand of 85 lacs is peanuts compared to this company’s market cap. I don’t think it will impact anything.

1 Like

I believe it has more to do with equity dilution due to their capital raising and ESOPs. If you carefully see even the retail holding is reducing and most banks and nbfcs go through this phase of equity dilution because of raising capital. I believe a 20%+ promotor holding is actually still healthy.

4 Likes

I did not see this disclosure on BSE website

STALLION ASSET PRIVATE LTD

Bought 58,406 shares @ Rs.2,529.99

Seller- ELEVATION CAPITAL

It seems Elevation (promoter group) took a partial exit from open market

The net worth now stands at 733 crores post dilution

2 Likes

Elevation capital has large shareholding in Arman , but not a part of promoter group as per my understanding. They are a fund house with investment in listed and unlisted companies.

1 Like

Stance: Invested

The QiP should have tremendous growth potential for the company. Very few NBFCs are showing such numbers in Indian market.

Book value of 470 Cr. Post QiP, this book value should be 700 Cr (470+230). That means, company is trading at around 3.5 Price to book, post QiP.

With a RoA of 7.6% and RoE of 35%, company is fully utilizing the capital adequacy norms. Further 40-50% growth seems to be too good. However, am not sure how long they can sustain this level of growth in microfinance industry. Any views from others on this?

12 Likes

How will market react to rise in NNPA is the question. To some extent they had signalled rise of expenses

1 Like

Every site is showing a different Price to Book value…However based on my calculation based on latest ppt, it’s coming out to be 3.3.

Book value per share ~= 770 cr/ 104 lakh ~= 735

Price to Book value = 2436/735 = 3.3

Can someone please confirm or correct me if I am wrong. Thanks

3 Likes

Yes. Too less for a financial company generating ROE>35% pre QIP.

2 Likes

Market has reacted quite negatively… just because of the uptick in npa numbers? I think management had already hinted about it in last concall. Other parameters that got impacted were due to RBI guidelines, which I think shall normalise.

4 Likes

From next quarter disbursement numbers should pick up, regarding rise in npa nos these should normalise going forward , as mgt has delivered and over longterm, above very few companies generate 35% roe, and above all 5000 cr aum in next 3years should double the profit

6 Likes

Arman qtr 3 inv ppt detail 060224.pdf (1.9 MB)

Just heard the conferance call .

- Arman have started micro LAP loans -this is very good

And this is rural with ticket size of 3-10lacs

And this is rural with ticket size of 3-10lacs - Difficult to get a Nbfc growing for decade at 40% with roe of 30%,ROA of 7% ….And now whatever little getting into a bit of secured loan ,a product for long term ……

- And don’t need any equity to double from here on till AUM of 5000cr

Discl: Views may be biased bcos of my holding

20 Likes