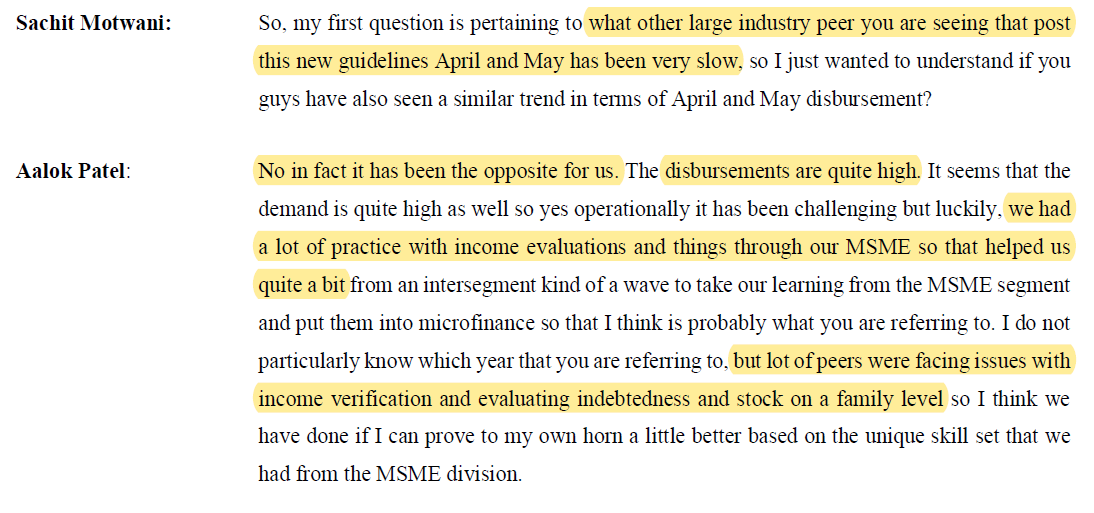

“Micro loan delivery slowed in April-May as lenders took time to adjust to new guidelines”

On the other hand Arman Financial’s comments in Q4FY22:

“Micro loan delivery slowed in April-May as lenders took time to adjust to new guidelines”

On the other hand Arman Financial’s comments in Q4FY22:

438d9eaf-077c-4b88-8cb5-49246a8e14c7.pdf (327.8 KB)

Q1FY23 results are out. Key highlights -

INR 15.7 crores of profit (sustained on QoQ basis despite rising credit costs. Should be passed on completely by next quarter)

AUM approaching INR 1400 crores (Mgmt guided 35-40% growth over FY22 AUM. It seems it will cross that easily)

MFI Collection efficiency back to a solid 99%.

Another solid performance!

Disc. Invested.

The Qtr 1 result is very good ….

1)clear uptrend in Collection efficiency

2) good improvement in asset quality matrix (NPA around 0.3% is excellent ,possibly the best in listed MFI space )

3)annuliased ROE coming back to pre covid normals….

4)AUM close to 1388cr ,going by current rate of disbursement AUM by Mar end should be around 1800cr looks like (without any macro risk ),lets see….

Discl : Arman is my largest holding in PF with significant allocation hence I am completely biased ,request everyone to do your own due diligence

Last Quarter had securitization income of 5.8 crores. Excluding that Pat has grown QoQ from 10.2 crores to 15.7 crores QoQ.

Disclaimer:- Invested and one of the top 3 positions in PF. Do your own research.

Solid set of numbers from Arman Financial

Rev 93cr vs 51cr

PBT 26.7cr vs 7.3cr,q1 at 20cr

PAT 20cr vs 5cr

H1 EPS 42rs vs 10rs

GNPA 4.89%,NNPA 0.56%

Very good set of number by Arman

Arman Qtr 2 141122.pdf (412.7 KB)

Discl :Views may be biased as I am one of the largest individual shareholder ,please do your due diligence

detail presentation gets even better

Arman Qtr 2 161122 inv ppt.pdf (2.9 MB)

Just some qualitative observations from the Q2 FY '23 Earnings Conference Call. Management appears to be cautious and mature. Some of the answers they gave speak highly of their leadership skills :

When asked if as a result of new software “operating leverage in terms of opex coming down as a percentage of assets or income whichever way you look at”.

“I mean, no. Sir, that is always a hope. And as Jayendrabhai would put it that cost-cutting and finding efficiency is always a constant endeavor. However, you will find us to be quite lean overall, how much extra lean that we can become, I think the idea is to always find a balance. If your goal is to become the leanest and the most cost-efficient company in the industry, you might get some good short-term results but that means is you are not investing enough. Your people might get frustrated. Your retention might suffer and a lot of other things might happen."

On being asked if the new software will result in the loan officer being able to handle a higher volume of clients, customers?

“It could, but I’m not exactly sure whether that should be the goal because higher per person capacity also comes with its own set of risks when something goes wrong. So when the delinquency and stuff rise, one person is not able to manage such a large case load. And the group sizes also have been overall in the industry going slightly lower as years go by. But what will help us in the future is moving more towards the cashless repayment. And in that case, yes, an FO will be able to handle more customers, but that will be a whole new model. Under the current model, I don’t think that is our overall goal is to increase the case load for FO, although that might be an ancillary benefit down the road.”

In summary, they are not in the league of making grandiose claims. They also show respect to people. A different league from, say Axis bank with its alleged toxic culture…that’s another story.

-Disclaimer: Invested

Realisation dawning on Sponsors and Promotors that MFI is a touch and tough business!!

@Worldlywiseinvestors How do we gauge whether we are in a lower end or higher end of the MFI cycle? Are there any metrics that you track to check if we’ve crossed the peak of the cycle & to time the exit points?

Disc : Invested

Check the NPA % as a trend whether coming down every quarter for buying the cycle and when NPA % trend starts increasing for few quarters to sell the cycle

+Tracking technicals of the entire sector can help along with business momentum. At the moment cycle has just turned and even the most conservative lender i.e. Kotak Mahindra Bank is growing the Mfin book at a fast pace.

Disc: invested.

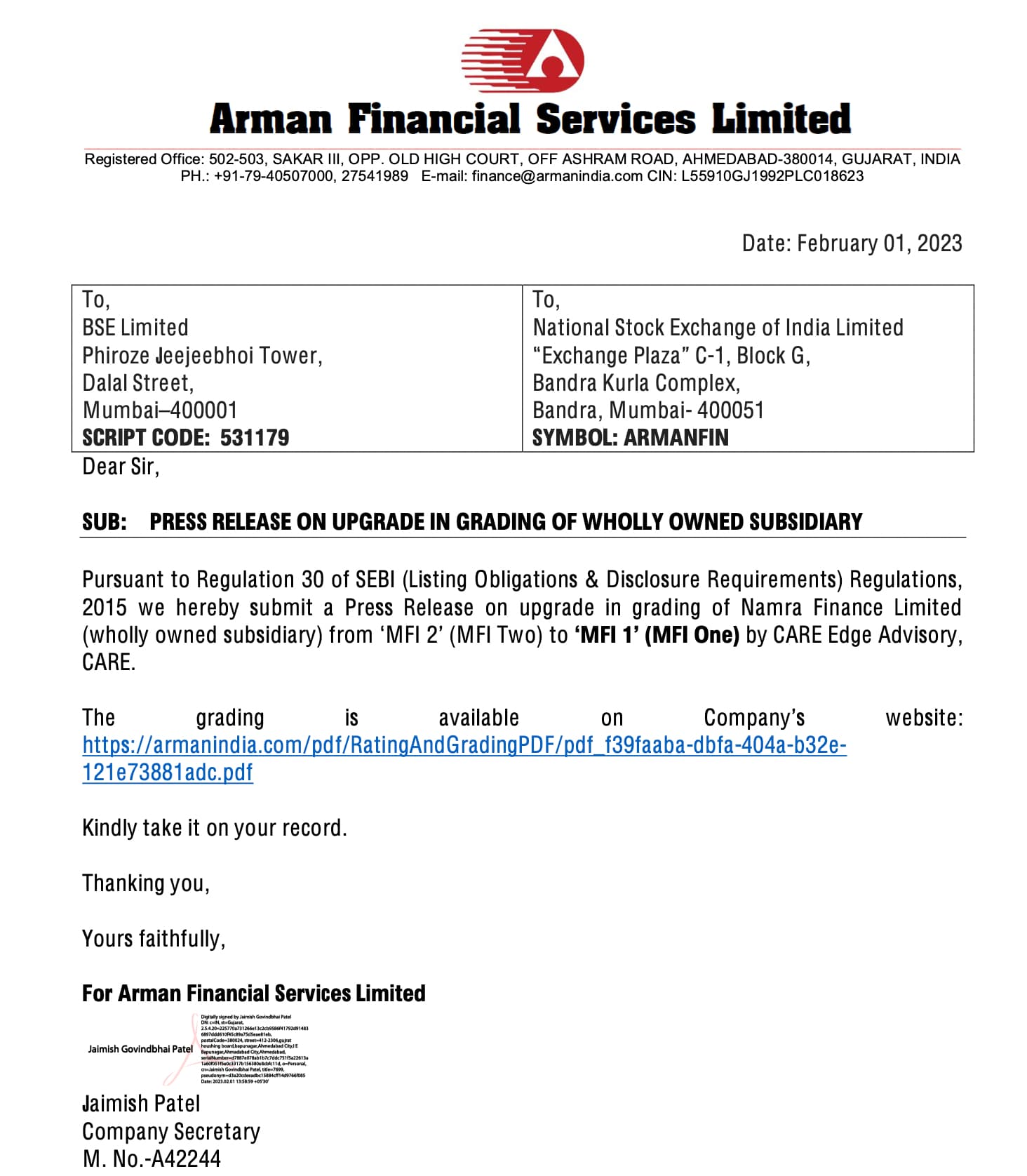

Credit Rating Update for Arman

Disclaimer: Invested and remains one of the top 3 allocations in the PF.

7cb444dc-efe1-4b98-bd3a-7c9e4269b512.pdf (2.8 MB)

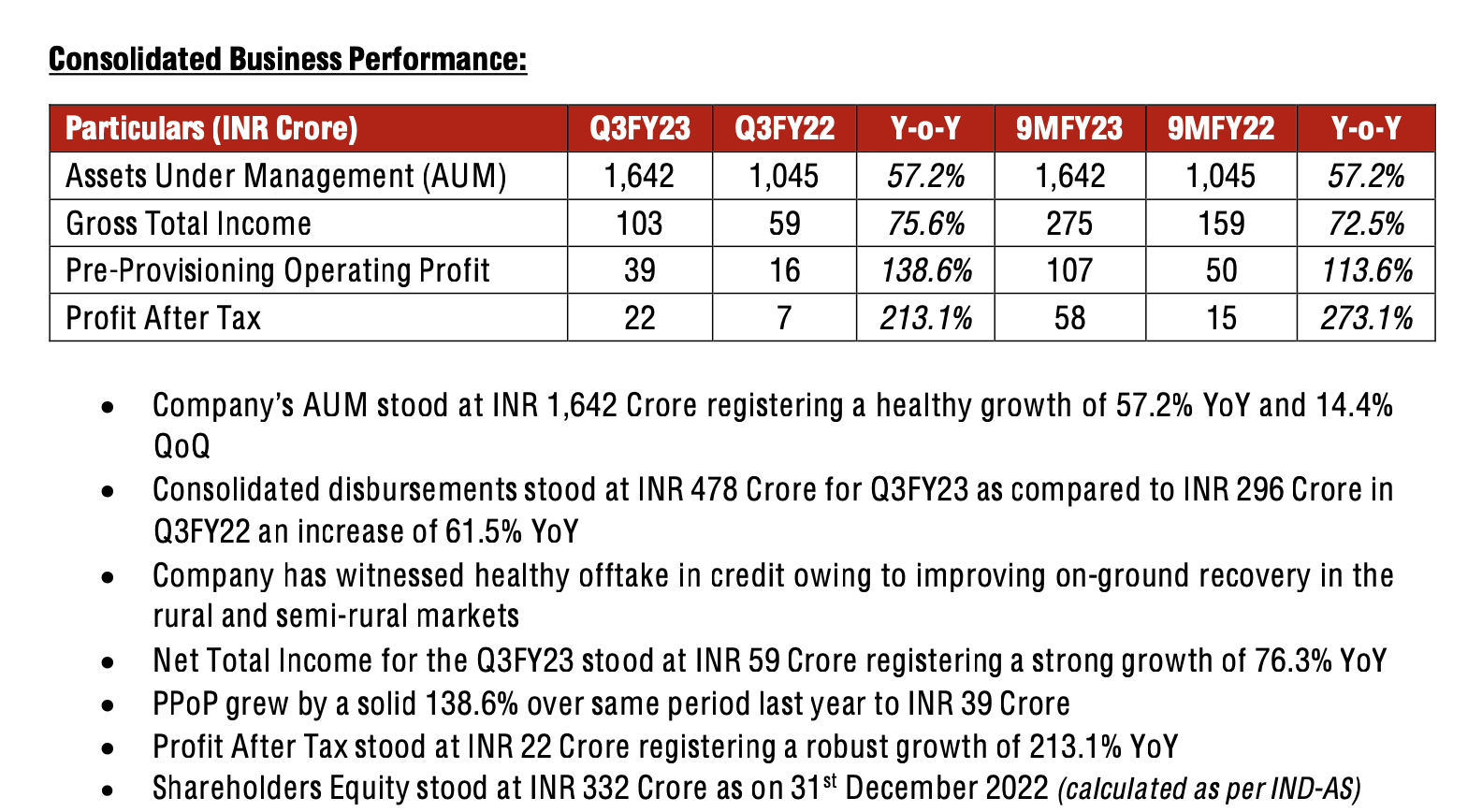

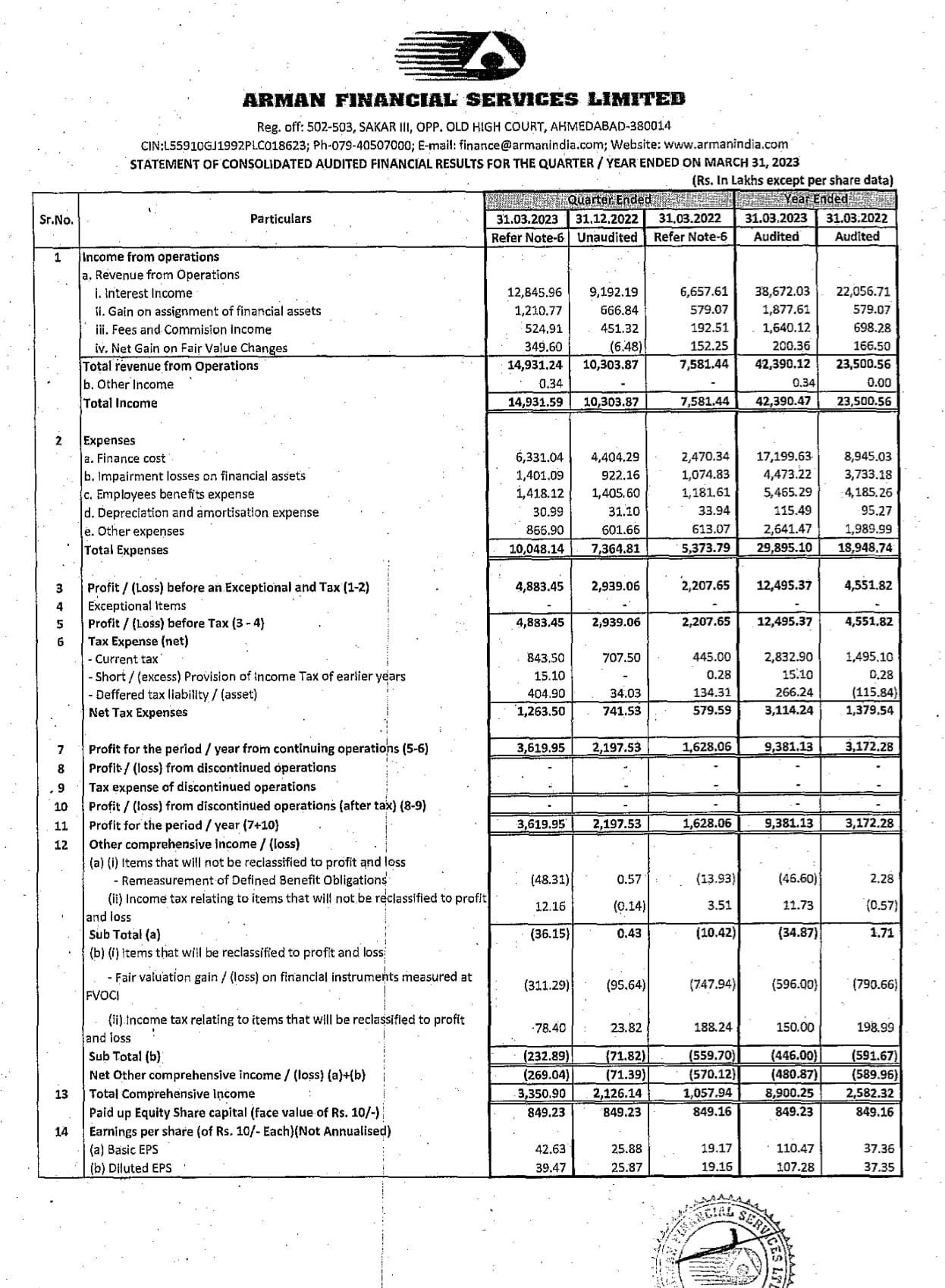

Q3FY23 Results.

Profits have further increased QoQ and YoY, albeit higher than normal increase in expenses.

After todays fall the TTM PE stands at 17

Disclosure : Biased. Holding

Continuing with the trend of QoQ growth for last several Quarters. Reported 200%+ PAT growth and 10%+ QoQ growth.

What was interesting to notice in this quarter is:- They have also started doing Individual Business Loans

Disclaimer:- No reco to buy or sell. Invested since 800s & no transactions in last 30 days. Please understand this is a cyclical business. Why you bought will also give you the reasons of selling.

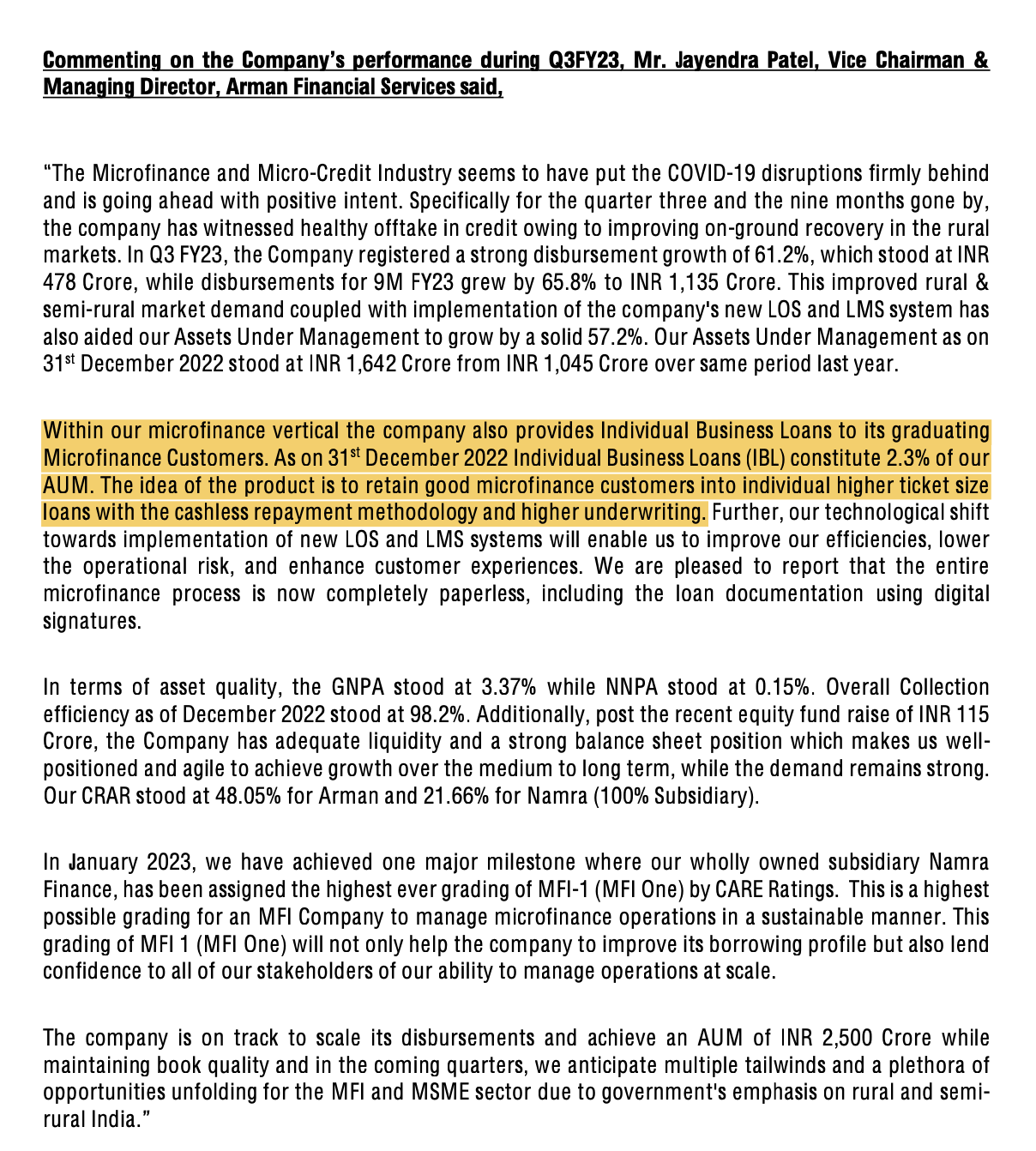

Arman Financial Services Ltd Concall Q3-FY23:

Credit demand is unaffected and rebounded even after the rate hikes by RBI; strong disbursement growth in Q3; improvement in rural and semi rural demand.

Started offering individual business loan; as on Dec 22 it contributes 2.3% of AUM; idea is to retain the MFI customer

Achieved milestone in Jan where company has received highest ever credit rating in MFI segment; it will improve the cost of borrowing for the company

Entire MFI process is now completely paperless; Arman is first company to do so in MFI segment

AUM growth of 14.4% QoQ; disbursement increased 72% QoQ basis; growth supported by high demand in MFI segment; registered growth of 11% in GTI due to improvement in yields; recorded highest ever quarterly profit

Have presence in 8 states with 321 branches; company forayed into Bihar & Haryana

Company believe that worst is behind us and they will see robust growth in next couple of quarters

Finance cost increased in current qtr due to CCD and OCRPS; also the interest rates has been increased as RBI raises repo rate. Approx 5cr is due to OCRPS; in Q4 also there will be slightly higher finance cost

Direct assignment transaction is of Rs. 100cr in Q3; the gain increase is due to lower retention ratio; and weighted ratio of tenure also impacts the assignment income

Increase in NPA of MFI is due to West Maharashtra; it is a small blip; but it is under control on an overall basis. Also increased due to RBI new guidelines, due to its new guidelines the increase is of 20bps.

Our target is to grow 35-40% in AUM over a long period of time. Will continue the same or near that in next year as well.

Avg cost of borrowing is around 12%; might expect increase of 20-25 bps due to repo rate increase by RBI and also after improvement in credit rating company may continue in the range of 12% as well but it is hard to tell currently

Approx 5cr increase in finance cost is due to qtrly impact of 3cr of CCD & 2cr due to OCRPS; this 5cr qtrly impact will continue till the redemption/conversion period i.e, till Mar 24

Our target is to achieve 2500cr AUM in next few qtrs and expecting 14 to 15% NIM going forward;

I really like how they’re finally pivoting into individual business loans in full swing.

Although its just the existing MFI customers upgrading into IBL, In my opinion this is a seed for what will become a muti-line NBFC tree for Arman

Disc. Invested. No recommendation to buy or sell.

https://www.equitybulls.com/category.php?id=328358

In the backdrop of the prevailing regulatory regime and RBI’s concerns towards deposit taking activity by NBFCs, the Board of Directors in its meeting held on Feb 23, 2023 considered the issue of the Company voluntarily surrendering its deposit taking license and convert its status to ‘NBFC-Non Deposit’ taking (NBFC-ND).

.

Taking a holistic view, the Board concluded that holding the deposit taking license is neither a business necessity nor serving the Company’s best interests. Therefore, the Board has decided to voluntarily surrender the Company’s deposit taking license and convert its status to NBFC-ND.

very good detail report on MFI companies with projections

Microfinance – Upcycle set to get stronger 270223.pdf (704.9 KB)