It has completely different problems, PE guys who owns > 51℅ wants to sell it to axis banks at certain price, MD wants at higher price.

What CRISIL had to do with it?

There can be exception to ICRA but CRISIL I can find any.

It has completely different problems, PE guys who owns > 51℅ wants to sell it to axis banks at certain price, MD wants at higher price.

What CRISIL had to do with it?

There can be exception to ICRA but CRISIL I can find any.

Why Arman gets such huge valuations PE of 90, ??

Second debt market and equity market difference ?

These are the completely fair questions any outsider can ask.

But who knows company very closely knows what’s the point behind such valuations.

My company also do cattle financing , in case of Arman that’s the unique segment that other micro financial find difficult.

Because of its large customer pool they manage to grow at such a scale, but now the time was difficult. Now even HDFC started cattle financing. There are many small players enter in this segment.

So according to me golden days are over, now they have to struggle from both side. As u have seen they are making impairment losses since laste 6 qtrs.

Similar story continues I guess…

And because majority shares are in strong hands .so they are waiting weakers to come  .

.

Disc. Sold my position.

Well done @Worldlywiseinvestors ![]()

As always @Worldlywiseinvestors has successfully done his part in enlightening about the segment in MFI.

Disc:- Invested from 875 levels.

Pe question, might need to normalize the Pat no to check the Pe

In case of financial companies, it is almost impossible to say anything with certainty (about the quality of assets, recovery processes, whether the numbers are being fudged etc.) unless one is an insider and really in the know of things. See the recent case of IndusInd Bank. Investing is a matter of faith in the management more than anything else. Bad asset quality is apparent and can be seen by everybody, but good quality cannot be guaranteed even if nothing adverse is visible. Absence of evidence is not evidence of absence. After I realized this, I stopped investing in financial companies totally. Just not my cup of tea.

(Disc: No view on Arman. Not invested, not interested.)

Arman conference call link

TRANSCRIPT OF THE INVESTOR CALL HELD ON NOVEMBER 17, 2021

Blow out earnings!

Cycle is turning.

Disclosure:- invested and transactions in last 30 days. Not sebi registered.

Arman.pdf (320.9 KB)

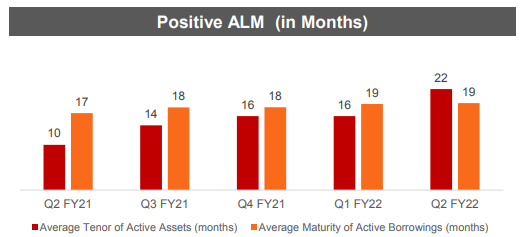

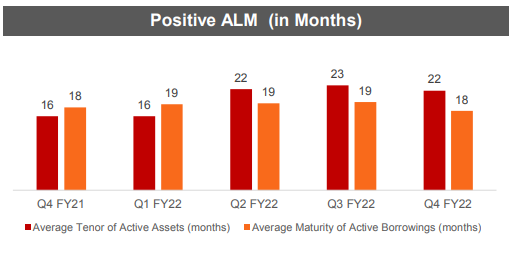

Any view on their long term alm mismatch? this is from Q2

Another nice interaction post Q3FY22 results.

Strucutral change I’ve been waiting for is finally here. Removal of interest rate capping

RBI puts an end to pricing caps for microfinance lenders and standardises the definition of microloans. RBI Removes Pricing Caps For Microfinance Lenders

Roe and roas will bump up post these changes.

Disc:- invested. Part of top 5 holdings.

Good business update

Also Good collection efficiency and on increasing trend for last few months !

Arman business update 130422.pdf (183.0 KB)

Just points to bottoming of the cycle and the eventual recovery. Those who bought the pain will truly reap the rewards if we have a +ve cycle for atleast 1 year.

Disc:- invested.

Good article on MFI

Discl : Biased bcos of my holdings

Arman qtr 4 result 300522.pdf (4.3 MB)

Since Q2FY22 they are having negative ALM . I don’t understand how this is going to work out in future? are they going to raise fresh debt to have +ve ALM? Did this happen in past? Why the average tenor of active assets increased after Q1FY22? Was it due to restructuring?

I am surprised in Two - wheeler finance and Cattle finance they are running into ALM issues, means they are borrowing very short term loans.

Can you please share how you know it’s cattle finance and 2w finance where these alm problems are