If anyone can quantify the impact of covid-19 in terms of percentage, I mean if you can elaborate how much percentage of topline will be heated and similar in bottom line.

No one is is knowing how going forward the covid-19 will take shape… Or how brutal it could be

Can anyone tell when arman will be removed from asm list

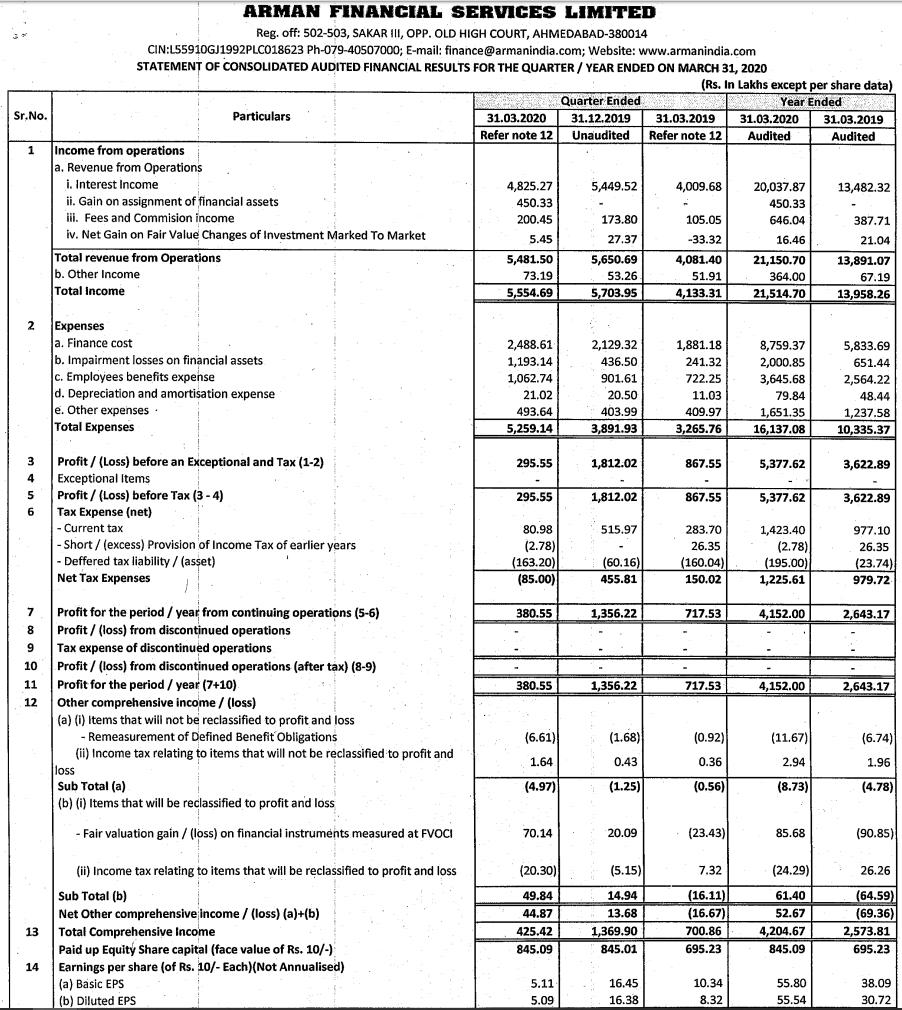

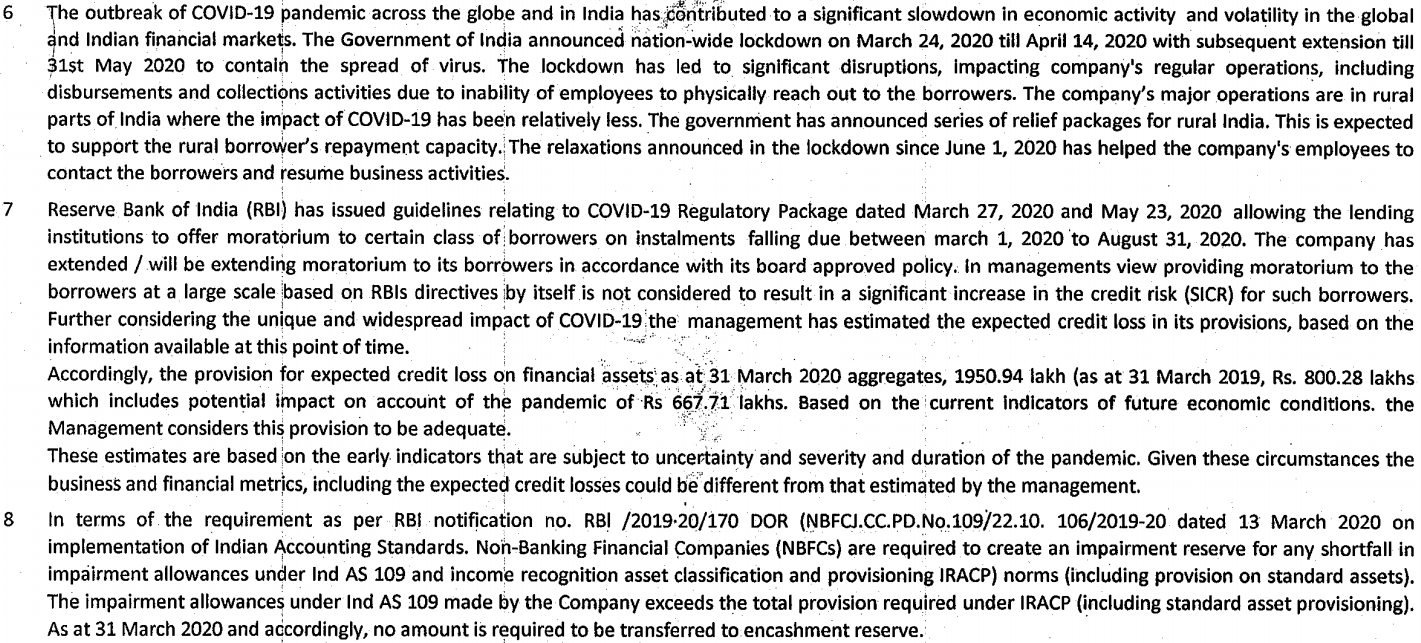

Q4 FY20 results:

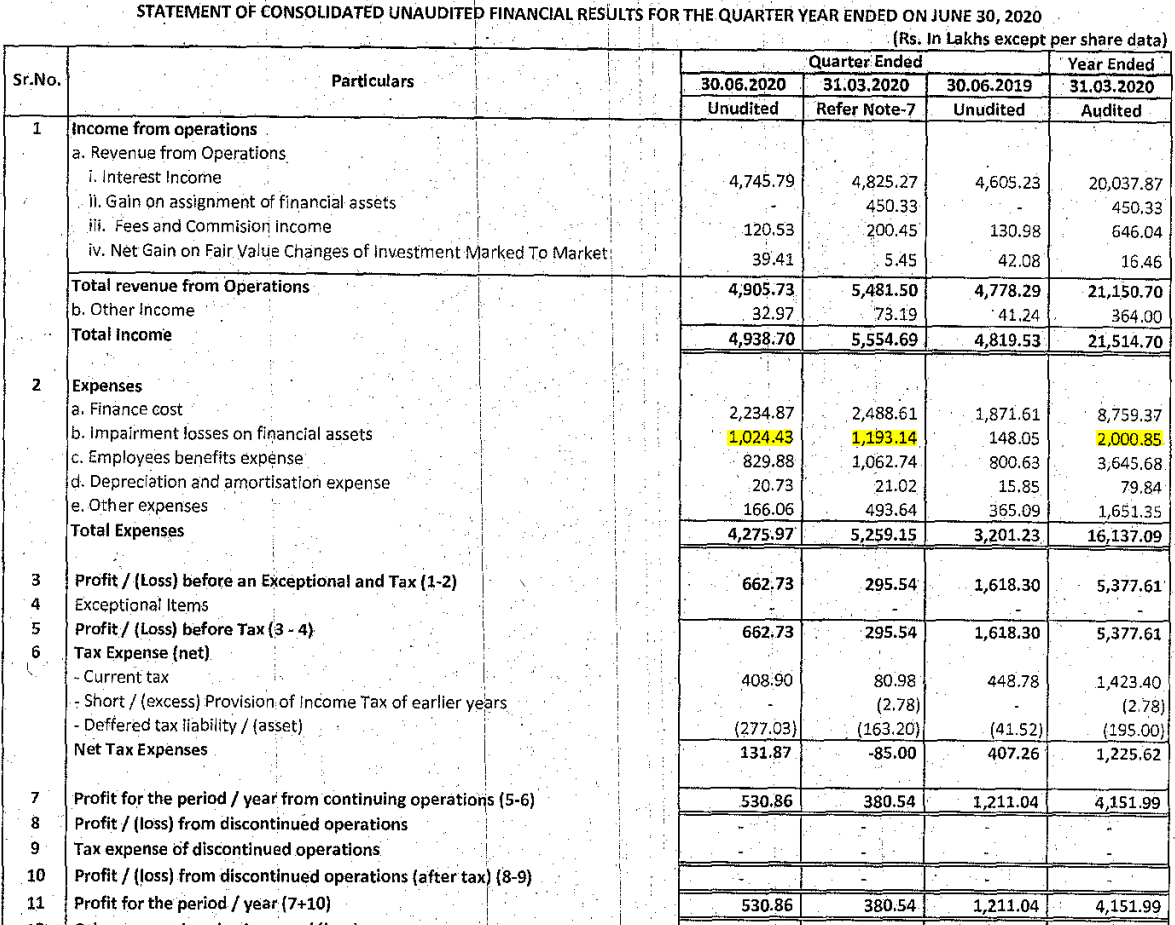

Impairment taken extra as 8 Cr compared to previous quarter.

Interest income is 7 Cr lesser.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/31043f73-6d86-4aa1-a290-f6f16a7814aa.pdf

Important notes:

Mgmt commentary is optimistic, saying rural impact is less and greater impact was due to non-visitation by recovery agents.

4 Likes

What is the meaning of impairment of 8cr ?

Disc. Tracking

The number might have some slight mis-calculation, but the overall idea is explained in the points noted, #7 and 8. Basically it is nothing but provisioning for expected NPA. So, setting aside part of income (in advance) to pay for (roughly estimated) bad loans. Some part is required by RBI rules.

Better explained in this press release perhaps: (under ‘Provisions’)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d9a379d3-5c1e-4f42-880b-fe00f1cae026.pdf

3 Likes

1 Like

The call went fine. Few points to highlight:

- Disbursement has been stopped since March, focusing on collections. Restarting of disbursement unlikely till collection efficiency reaches 90-95%. Have cash of about 120-125 cr.

- 48 cr loan repayment in Jul, 42 cr in Aug and 135 cr in Sep.

- Almost finalised equity raising when the lockdown happened; couldn’t close the deal. Open to equity issuance to get some more comfort. However, valuations not favourable.

- Someone suggested cashless collection but Arman has high touch with customer base. Don’t want to lose that. So, still exploring UPI / QR systems or hybrid for cashless collection.

- Most collections in a month happen between dates 1 and 12. 85% monthly collection; MFIs bi-weekly, 2W direct debited in the first week of the month.

5 Likes

few updates on Arman-

Arman Financial Q4FY20 Concall Update – Nirmal Bang Securities

(CMP: Rs. 463; M.Cap: Rs. 391 Cr)

Play on faster revival in rural India; Healthy collections for June is encouraging

Outlook: Positive

Operational Updates

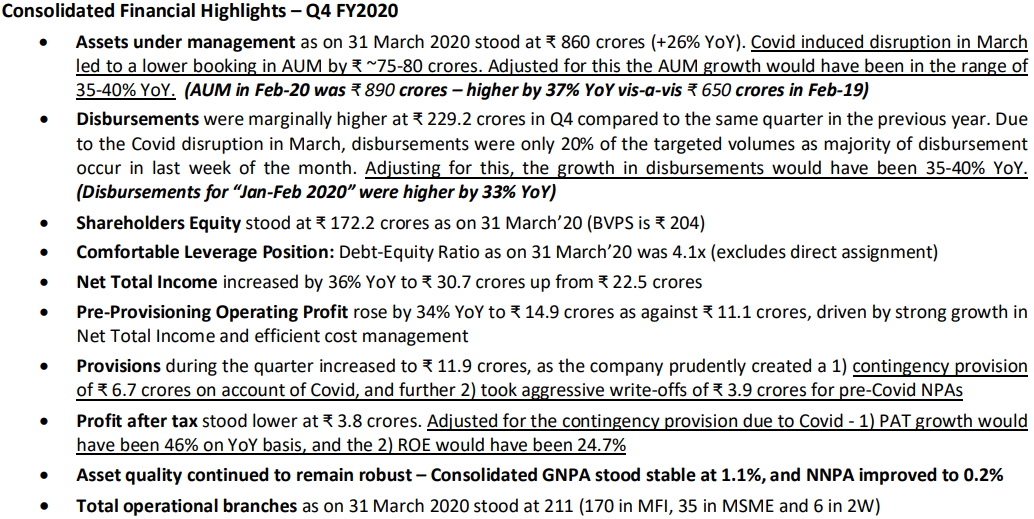

• Total AUM increased to Rs. 860 Cr (+26% YoY). Adjusted for the lower new loan booking of Rs. 75-80 Cr due to Covid, the FY20 AUM would have otherwise grown by 37% YoY.

• Segmental AUM Mix: MFI has remained stable at 71%; MSME has increased from 10% last year to 17% and 2W has declined from 20% to 11%.

• Segmental AUM – MFI Rs. 622 Cr (+29% YoY); MSME Rs. 143 Cr (+44% YoY); 2W Rs. 95 Cr (-7% YoY).

• Within 2 W, Rural AUM was at Rs. 11 Cr and grew by 68% on a low base.

• Total Disbursements grew 4% YoY to Rs. 229 Cr. Co has not yet started disbursing loans neither offered any top-up loans post lockdown. Co will start disbursing from 15 July onwards with tighter underwriting standards. Disbursement levels will not reach pre-covid levels until Sep 2020 atleast.

• PPOP increased 34% YoY.

• Co provided for Covid provisions of Rs. 6.7 Cr in addition to normal provisions of Rs. 5.3 Cr

• PAT came at Rs. 3.8 Cr vs Rs. 7.2 Cr YoY.

• Adjusted for the contingent provision created for Covid, PAT would have stood at Rs. 10.5 Cr (+46% YoY) in Q4 FY20.

• Co has 211 branches; 170 for MFI; 35 for MSME & balance for 2W. Co added 43 new branches during FY20; 32 for MFI & 11 for MSME.

• Arman obtained moratorium from banks for 72% of the amount due for the months of April & May. Arman has comfortable liquidity now and has not applied for any moratorium from banks for June. Co also raised Rs. 75 Cr post lockdown to strengthen its liquidity which includes from NABARD & SIDBI at sub 7% rates. Co is sitting on Rs. 120 Cr of cash.

• The govt support for rural population is a positive for the co & MFI industry.

Asset Quality & Collections

• GNPA was at 1.1% vs 1.0% YoY. (MFI 0.9%, MSME 0.3%, 2W 1.4%). NNPA was at 0.2%.

• Total moratorium for April was at 45% and for May at 50%.

• The company resumed collections from 1st June onwards. A majority of the MFI & MSME customers have repaid their dues for the month of June despite the RBI extending the moratorium till August. Repayments rates for June dues closed at 59% for the MFI segment, 85% for the MSME segment and 95% for 2W segment. Thus collections on total AUM stood at 66% for the month of June and is beyond the expectations of the management which was expecting collections of only around 40%. Repayment rates in July should be much higher.

• State wise, Gujarat outperformed for Arman with collections at 74%, MP was 60%, Rajasthan was 56%, UP was 55%, Maharashtra was lower at 42%.

• MSME is mostly being done in Gujarat and hence it has higher collections.

• The 2W bounce rates in April & May were 45-50% compared to the normalized level of 15-20%.

• For MFI - 85% of customers are on a monthly collection cycle and 15% are on biweekly cycle.

• As currently disbursements are not happening, even sales team is doing work of collection.

Co achieved an ROE of 28.1% in FY20 (vs 29.8% YoY) despite providing for Covid provisions in Q4. Stock is trading at FY20 P/B of 2.3x & P/E of 9.4x

3 Likes

Interview of the Promoter /ED -Aalok in CNBC -

PART 1

PART 2

Arman on cnbc…72% collection in July.

4 Likes

Out of bunch of NBFC’s how Mr. Alok Patel director of micro cap company like Arman finance get selected for the debate.

Why this company wants to be in news?

Disc.Invested from 320 levels.

2 Likes

Q1 FY21 results:

PBT:

125% up QoQ

60% drop YoY

10 Cr further provision created, adds to 10 Cr created in previous quarter and 10 Cr carry from before that.

Another quarter and the story should stabilize, maybe good growth by end of the year. This would have been the worst quarter operationally.

Gains are mainly through control on expenses.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/014936bc-1412-47d5-bf9a-9364326dc4a7.pdf

4 Likes

Indeed very commendable performance by the team

2 Likes

@DEBASHISH

Waiting for ur comments on latest results . And current situation of overall MFI industry.

My apology for replying late as I dont go thru valuepickr on a daily basis (though regular with time lag

1 First of all I will point out my "thesis of investment " in Equity market .I normally like financials and investment in brands (given my experience in this field over years .

2 I normally like to invest in a category where the category is growing and then find out a strong or a niche player in that category .

3 I define strong by market share and niche by having "competitive advantage /differentiation /uniqueness "

4)In India MFI as a category has been growing and will grow more than 20% pa+ CAGR for next 10 years + given the under penetration of the banks in this space .Given that PSU banks is loosing market share the same will continue for many years .I like Arman because of their prudent lending practice .They are conservative and since lending is a leveraged business it helps .They are one of the company who stopped disbursement the next day of demonetization (9th Nov 16) which attractive me to invest in Arman then .

5)Coming to results I am happy not only on the results but the way they are building provision buffers. 6)I expect in next 6-7 quarters the real NPA will hit the MFI and banking sector -it can be anything between 5-10% of current AUM (its anybodies guess and hence I can be wrong ).

7)I expect Arman to be on the lower side when it comes to NPA in the MFI sector -they have already build close to 4% of AUM as provision and may gradually do so over few quarters .I like this aspect of being conservative and prudent

8)Their collection efficiency and bounce rate of MSME and 2 wheeler is one of the best in the industry (its better than Bajaj finance also - in no way i am saying that as a business they are better than Bajaj finance -BTW i am invested in Bajaj Finance also ) but MFI collections at 80% is little below the best of MFI’s around average of 85% .Just a caution Spandana’s collection efficiency at 92% is not being believed by the market and hence they are being punished by market ,hence I have ignored them in the average .

9) Arman have adequate fund as of now -though they dont need fund but they may be preparing to raise equity for future at right price and I " personally believe "SAIF partners would also be investing when the promoters dilute as they are now on the board and involved like a long term partner (I may be wrong on my view )

Discl -I am completely biased because of sizable holding in Arman ,hence request you and everyone to please do your own due diligence .

7 Likes

Crisis research on collection efficiency across sectors -Arman is better in all !

Crisil collection efficiency ytd aug20.pdf (261.7 KB)

3 Likes

Sorry but I am missing something…

Where does armaan financials name mentioned in the report, not in charts also!!!

1 Like

Check Armans last quarterly presentation on collection efficiency and compare with crisil report(average of the industry ) -you will see that they are significantly better on all parameters

3 Likes

@DEBASHISH

Sir

Please throw some lights on financial results…

Impairment losses widen to 1863lacs during the period when bajaj finance and other NBGCs performed well is it warning ??

Disc . Top holding

The impairment loss on financial asset is actually doing impairment testing on provisions and booking it ,looks like this is done all across business verticals ,this would be done by auditors with input from management is my understanding (actual loss may be less or more ) .Since we dont have the investor PPT yet ,we have to see what they mention in that and in investor concal, we need to ask whether in next quarters also they have to do this “huge provision” or not ?

Discl: my largest holding also

2 Likes