Whatever I could …hope I replied your queries …

1 Like

…“Microfinance Institutions Network—an association for the microfinance sector in India—has asked all the members to inform customers that collections will resume only after the lockdown ends and that they should keep the instalment money with them. As per Credit access grameen , the economic impact of the lockdown would not be too harsh as local consumption remained healthy for rural microfinance firms”…

2 Likes

@DEBASHISH

Now a days how much sentiment has changed for arman?

How much the topline and bottomline could be impacted due to COVID pendemic now and upcoming ?

Lockdown seems to be withdrawn in phased manner? No. of phases could be 3 or more and the timeline of each phase will depends on upcoming situation…

What makes investors to sell at such valuations?

Disc. Not invested

Now a days how much sentiment has changed for arman?

Reply -You mean sentiment of the market on Arman -That has completely changed in last 45 days which is why the sellers are more than buyers and hence prices are coming down everyday .

How much the topline and bottomline could be impacted due to COVID pendemic now and upcoming ?

Reply -Its difficult to predict as the scenarios will be very different basis no. of days of lockdown .The lesser the lockdown the better .Since I have been tracking this company for years ,in next couple of months ,they will focus on collection than on growth ,which is the right thing to do.

Lockdown seems to be withdrawn in phased manner? No. of phases could be 3 or more and the timeline of each phase will depends on upcoming situation…

Reply -This is the worry ,the more the lockdown ,more will be the impact on their business .

What makes investors to sell at such valuations?

Reply -Normally investors have a recency bias ,they are scared of the unknown and what matters to most is the impact on the portfolio .Its very common for a normal investor to feel scared and depressed to see portfolio going down everyday .On top of it in this kind of scenario, leveraged business like financials in short to mid term will be severely hit and hence no one wants to see losses in the portfolio increasing .

I dont see share prices like a paranoid .To me what matters is how the business will do in long run .I want a business where I can see “sustainable profitable growth” .All the 3 words is important for me in long run .I had seen this in Arman ,unfortunately like I said before in my earlier posts ,that Covid19 is a black swan event and hence derailed the story by atleast an year ,if not more .Having said that if I

fast forward 2 years ,will Arman’s business ,both in terms of topline and bottom line be better than FY 20 ,I think so and hence not only I am invested ,but I am also buying regularly but slowly .

Disc : Because of my large holding ,I may be biased and hence please do your due diligence before investing

8 Likes

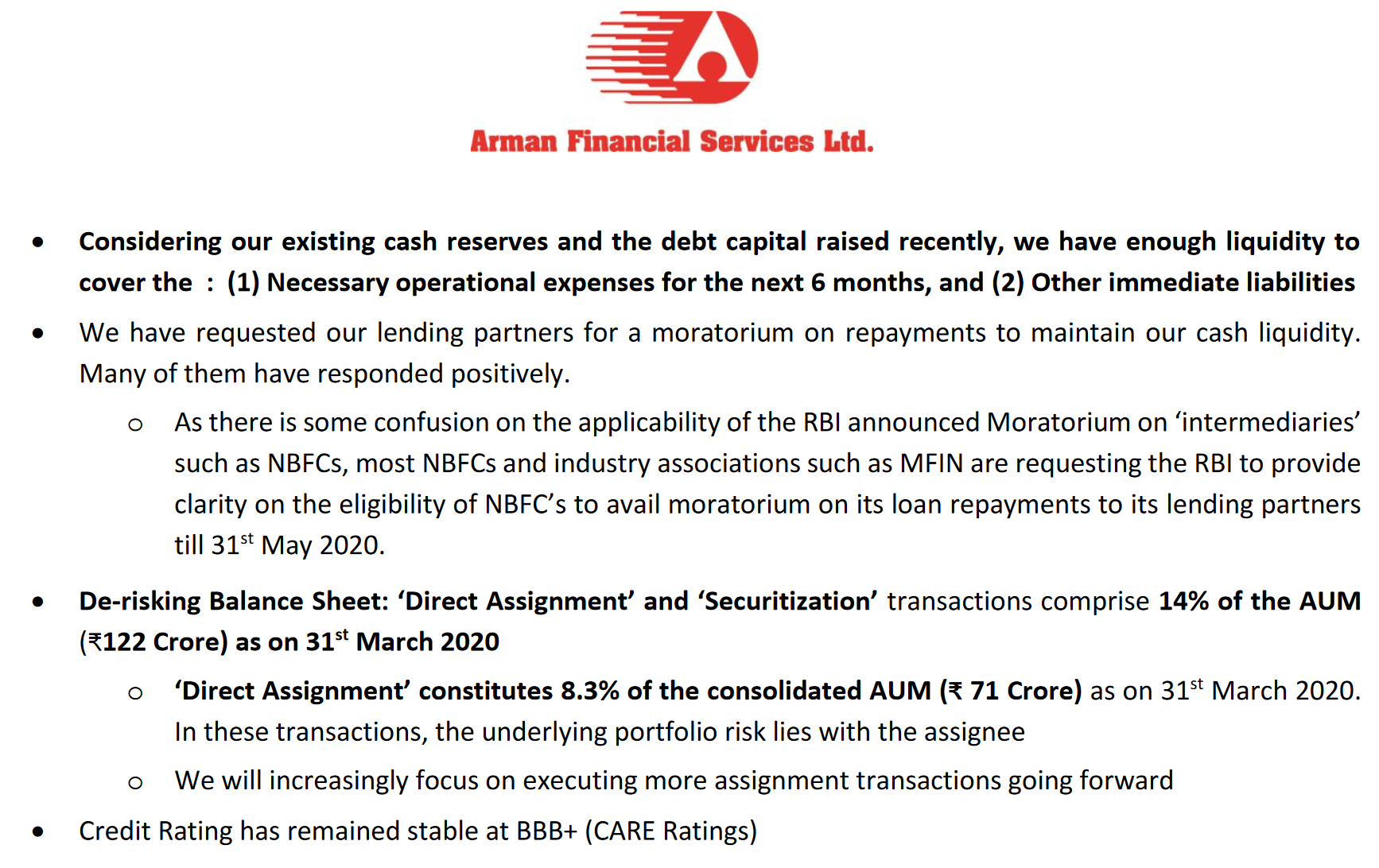

Arman Financial Services Limited: COVID-19 Business Update:

3 Likes

very detail and optimistic press release by Arman .

Some important points :

Resilient Customer Base in Microfinance & MSME

• Majority of our customer base in the ‘Microfinance’ and the ‘MSME’ division is based in rural areas

(comprising >80% of the AUM). Fortunately, the impact of COVID has been limited in Rural India so far

• Moreover, the recently announced food security and economic relief measures by the government will

hopefully aid in augmenting the repayment ability of borrowers in Rural India

• Customers engaged in essential activities (such as dairy activities, grocery retailing, etc.) form the bulk of our

portfolio, and for initial data available to us, they have not witnessed any major disruptions in their supply

chains yet.

Action Plan – Post the end of Lockdown

• Once the lockdown period is over, our field officers and branch managers will be determined to restoreoperational normalcy on the ground at the earliest possible with the highest focus on collections. As it seemstoday, the lockdown will be extended for many of the Districts/States that we operate.

• Collection Plan

o We would avoid providing a blanket moratorium and will start our collection process after the

lockdown ends as most of our customers have indicated their ability to repay

o If a customer requests for a moratorium, we will educate them about the additional interest burden,

and if they agree to pay additional interest, we will provide the moratorium along with the revised

repayment schedule with extended tenor.

• Disbursements

o Will resume disbursements in a particular geography, only once the repayment rate stabilizes in that

region.

o Many of our customers will also need incremental loans. We will support them without compromising

on our credit discipline (protecting the asset quality of our book has always been and will remain our

top priority)

• Preserving Resources & Liquidity is the Need of the Hour: We have implemented hiring freeze till conditionssettle and put all expansion plans on hold. Disbursement have also been put on hold until repayments are ontrack. Going forward, we will maintain a strict vigil on our ‘operating expenses’ and look to implement stepsto improve operational efficiency. Collections will remain our top priority for the next 2 quarters.

• Given the current dynamic environment, the company will closely track the on-ground developments andregulatory announcements, and pro-actively take appropriate stepsto protect its asset quality going forward.

There are no blue prints for dealing with such crisis but is something businesses have to face from time-to-time. However, this is not the first crisis that our industry has faced, and companies with strong and sustainable business models have not only been ableto survive but thrive in the aftermath of multiple such crises in the past.Arman is no stranger to crises, and we have successfully navigated our way through each one of them in our 28-yearhistory. During the demonetization period as well, our collection efficiency was much better compared to the rest ofthe industry and we were able to grow strongly and profitably once the situation normalized.

We firmly believe that we have the necessary resources (both personnel & financial) along with the managerialexperience to steer our company through these tough times and emerge stronger on the other side of this crisis.

4 Likes

Though they have requested moratorium from their lenders,it is indeed encouraging to see that they have enough reserves to cover 6 months of expenses and payments.

4 Likes

Key takeaways from our(Edelweiss ) conference call with microfinance institutions (MFIs)

Growth

Most MFI players feel that COVID-19 is more of an urban issue and that the rural economy is not really impacted. Most MFIs are rural based and expect growth to return gradually once the lockdown is lifted. Till March 20, MFIs saw strong growth in disbursements. Post that, disbursements have nearly stopped. Companies expect the rural economy to improve on the back of a normal monsoon and onset of the harvest season. They foresee a gradual pick up in disbursements, which should aid growth.

Asset quality

The current situation is health and medical related, and not a financial crisis. Hence, intention of most borrowers to pay remains intact. Collection efficiency for most MFIs remained high before March 20. Spandana Sphoorty Financial’s collection efficiency till March 23 was 98.6%. MFIs are currently not able to conduct group meetings and collections have come to a complete standstill. As per the RBI guidelines, MFIs have passed on the moratorium to borrowers. Hence, it is too early to comment on credit cost and GNPA outlook for these companies.

Liquidity

As microfinance is more of a cash business, companies normally maintain high cash levels. Also, MFIs like Spandana and CreditAccess Grameen were able to raise funds from banks and other sources in March, which is likely to help them meet their financial obligations. CreditAccess’ cash balance as on March 31 stood at INR 530 crore, which is sufficient for the next 4-5 months even after considering interest payments and OPEX (principal repayment moratorium). With liquidity worth INR 537 crore, Spandana has opted for complete moratorium from banks on its term loans. Also majority of MFI loans are compliant with priority sector lending (PSL) norms. Hence, companies can securitise, if required, providing them extra liquidity.

Other comments

MFIs are able to borrow funds from banks and hence liquidity should not be an issue. Currently, MFIs are interacting with their customers to keep themselves abreast of the situation and also to assess the borrowers’ mindset on repayment.

Our view

Overall growth is going to be impacted for the next couple of quarters. However, with harvest season beginning next month, few MFIs, with strong liquidity, are likely to disburse once the lockdown is lifted, resulting in some positive growth. MFIs, which are present in their respective districts for a long period, are expected to have better collection efficiencies as their understanding of the borrower profile is much better when compared to a new MFI player.

4 Likes

Good insightful report on MFI ,points discussed are :

- Sector’s resilience and ability to bounce back

- Need of the industry –

- Support from lenders for moratorium , additional liquidity for business and growth

- Focus on employee and customer engagement to hold the credit quality

-

Theme is positive and how do manage the current crisis well on assets and liabilities

- Learning from past and way forward to emerge stronger

2 Likes

In addition to the measures announced for NBFC’s by the RBI today,liquidity measures to the tune of Rs50,000 crore with half of this coming to the MFI sector.

Link to Governor’s statement:

https://rbidocs.rbi.org.in/rdocs/Content/PDFs/GOVERNORSTATEMENTF22E618703AE48A4B2F6EC4A8003F88D.PDF

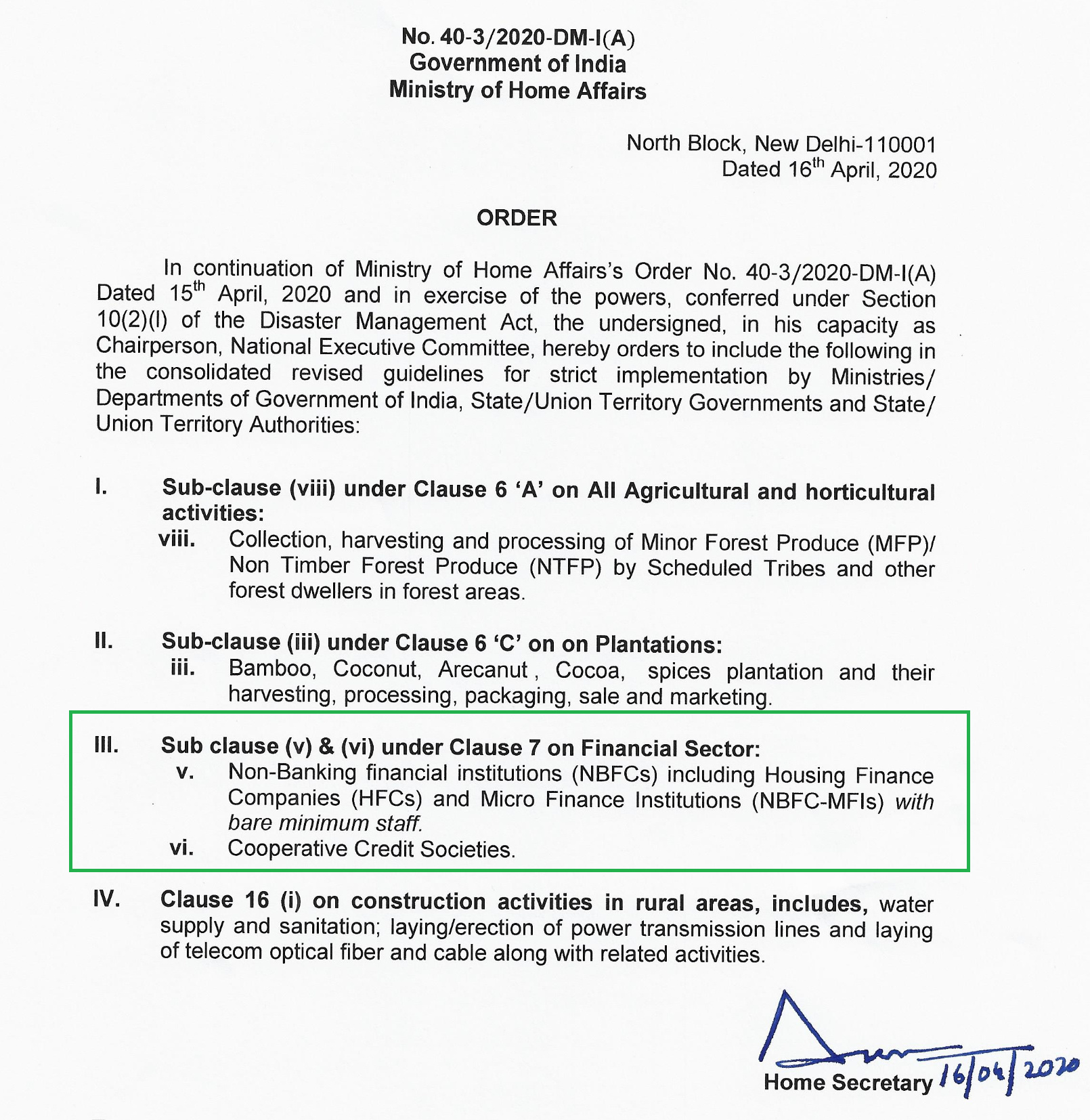

Yesterday the Ministry of Home affairs has allowed MFI’s and HFC’s to operate with minimal staff now like banks.

4 Likes

Have been regularly attending MFI webinars ,few insights in last few days which I could gather :

1)All MFI is facing collection issue because of lockdown ,including Arman

2)After 20th April ,depending on green zone(Arman has 76% in green zone as of now ) ,MFI will be able to collect but because of moratorium maximum of the buyers will not pay now

3)While MFI will be extending Moratorium they may not get the same from banks or NBFC (it will be at the discretion of banks /NBFC)

4)Hence liquidity will be am issue in short term for those who havent got the required liquidity (Arman has 6 months of operating expenses and few months of debt obligations )

5)While MFI faces huge difficulty now but they are amongst the few sectors which recovers fast (demon was a good example )

6)There will be credit loss in this crisis for all ,including Arman -this will get reflected may be after 6-9 months

7)RBI TLTRO scheme ensures it is passed by banks to MFI in investment grade .We need to see how fast this is passed effectively .Arman is amongst the few small sized NBFC’s who is in investment grade .Better and efficient way may be borrowing from NABARD /SIDBI

9 Likes

Today talked with one of the employe of arman finance he told the situation is unpredictable because we works with very lower income group and they suffer the most.

I also came to know that most of the labours whom they lends rs. 30000 loan are outsiders means either from orrisa,MP, UP or rajsthan.

And they will not suppose to come back soon.

They have huge exposure near ahemedabad and baroda region which falls in RED zone.

Disc. Tracking position

2 Likes

Hi, the intent is not to counter but just to give a perspective.

Its an unpredictable situation for sure. While the rural linked companies, mfi SROs like MFIN and Sa-Dhan and many market observers are of the opinion that rural hasnt been as much impacted as urban, and that rural will recover faster (will not go into the reasons for the same), however clearly the stock market believes otherwise looking at where mfi stocks are. Today, in the absence of hard data on collection rates or the impact of the lockdown on livelihood etc., these are views and opinions, and not analysis (not to say they are not important).

However specifically in Arman, it is a fact that they do not lend to migrant labourers or “outsiders”. Infact, one of the basic go-no-go criteria they have is that the borrower or spouse (whom they take as co applicant / guarantor) must own the house in which they are living in the location where they are availing the loan. Imagine, their borrowers are not even tenants, forget migrant labour. Another fact is that, if at all someone is migrating, it would be the husband (co applicant/guarantor) who would be going to other places to work for livelihood.

Ahmedabad and Baroda and many other large cities in various states are indeed in red zone. I am not aware of their % portfolio district wise, but one can guess that it wouldnt be non-material. (Now here is an opinion, because we havent yet seen action on this), however state govt. and district/municipality level officials are mapping hotspots in all the red/amber/green zones. So its likely that there could be some economic related activity even in red zone, but this remains to be seen.

Thank you.

Discl - long time and long term investor in Arman and have vested interests and would have the attendant biases, howmuchever I would like to deny that.

13 Likes

If one reads the ET news below and the interview of Padmaja Reddy ( Spandana ) one gets a feeling that MFI will recover fast -only time will tell when they recover and how much will be the damage …

Notes on microfinance sector ! interview of padmaja reddy ( spandana )

- where ever company’s staff has reached, 80% of borrowers are paying installments (not able to meet borrowers is a problem)

Operational problems as of today :

- loan officers are not able to meet clients

- challenges from police , vehicles of staff being seized, landlord and neighbours complaining to police

- it takes 1 mins to collect money from borrower , now taking 15 mins

- surprise to see 80% people paying back ( npas shouldn’t be issue )

Also if they don’t pay now , they get delay in their cycle loan - i.e. they do not get next loan and moratorium interest money can be actually used for next loan interest payments

6)lots of district have zero cases or very low covid cases (20% branches in red zone)

-

Good point is some 50-60% borrowers are in essential services , i.e agriculture and dairy and allied activities. These activities were intact.

-

*due to migrants coming back and Increased demand ,

Daily agricultural labourer wages Increased by 60%

Like person otherwise getting 300 rs got 500 rs in last month

Add to it harvest season of crops like cotton chilly and paddy -

due to low ticket size installment size is less

-

presence in Tamil Nadu bihar west bengal and Assam needs to be monitored as they are very over leveraged

-

moratorium applications are from urban area (30% around )

Liabilities side

11) No problem in raising funds for companies rate good A and above

12) state bank of india nabard and other agencies are lending and even in lockdown company able to raise 800 cr

( Banks need PSL certificates )

Discl: I am heavily invested and hence opinion may be biased ,hence please do your own due diligence

5 Likes

Sir

I want to understand from you what makes Arman financial a better bet then Manappuram

Actually I am planning to buy some nbfc shares and read your Research report on Arman and that helps me lot.

That report has changed my perception about nbfcs.

I am interested in Manappuram because of 70% of their loan book are against gold and it gives complete safety.

Disc. Not invested but keenly watching both the companies will add on dips.

Hi ,No equity investment by definition is completely safe . If you are looking at "relatively safe " bet compared to Arman ,Manappuram may be better as a large part of its underlying business is backed by collateral like gold ,which is on upward trend .Since you are looking at relatively safe portfolio and looking at gold loan NBFC ,my suggestion is that you can look at Muthhot finance, as thats the best play being a market leader in that space ,with lesser exposure to MFI, unlike Manappuram who have higher exposures in MFI

1 Like

Very nice "insights " on MFI industry when it went thru crisis and how it recovered .On similar lines that its the first sector to get impacted and the first to recover -over few quarters things become normal .The hypothesis is backed by huge sets of data and analysis .Microfinance recovery analysis post shocks.pdf (281.5 KB)

2 Likes

Good detail report explaining the problems the MFI companies and its client are facing now …

Impact of Unfolding COVID 19 on MFIs and Clients.pdf (672.7 KB)

“The repayment behavior through periods of shocks may provide a fresh perspective to policy makers, lenders and rating agencies on the risk attached to borrowers at the bottom of the pyramid” -lets hope so as this industry serves the most important bottom of pyramid customers

1 Like