Starting as a boutique stock broking company in 1992, Arihant Capital now provides investing and trading services to over 1.15 lac customers through its 680 investment centers spread over 110 cities in India. Its offerings span the entire gamut of capital markets, both for individual as well as institutional clients.

It has managed the capital markets down cycle of 2008-12 quite well and has shown impressive 15-yr EPS and BV CAGR growth of 22% and 17% respectively despite the turbulent 2008-12 years.

It has generated positive operating cash flows and negative financing cash flows for most of the past 10 years. In fact it has generated hefty 65 cr operating cash flows over the past 10 years despite operating in the cyclical capital markets industry. Being asset light, these operating cash flows are reflected in the zero debt status and cash balance of 60+ cr (excluding cash belonging to creditors).

It has also been a steady dividend payer and has maintained more or less stable dividend even during the turbulent 2008-12 period. It’s current RoE is 15%, but has touched 60% during the earlier capital market boom years, and has been on an upswing over the past few years after touching a low of 7% in 2012.

Despite of boasting a financial and operational track record comparable to some of the much bigger players in the industry, its valuations are far more attractive, presumably due to it’s low market cap (45 cr) and low liquidity. It’s available at a P/E of 4.2, P/B of 0.6, and D/Y of 3.3%. The market cap (45 cr) is less than the cash balance (60+ cr).

Thanks for initiating a thread on this company.Looks to be good on all visible parameters like ROA, PB and MCAP to Sales. Checked in Moneycontrol site and it has been paying dividend since last 10 years. But recently an independent director resigned. Hope some seniors would help to analyse more and throw some light on whether this can be a value pick or not.

@AlokBhola

Hi Alok, Can you clarify what is this inventory thing - about 13 cr worth of stocks company is carrying on the BS. Why is it not mentioned as Current investments.

Also company is carrying too much of cash on books deposited with the banks ( 60 Cr +) . Due to this the ROE will always be low. This is poor allocation of capital. I was not able to understand why a company in the business of stock broking and advising clients as to where to invest would invest its own money in low performing bank deposits . Why not invest in stocks ? or better pay as dividend and we would invest in Valuepickr portfolio

Though the company has managed the business well in the past years. As per one news article, 14 lac demat accounts were added every month last year ( i hope i remember the fig correctly). Need to see how many delivery centres / customers company has added this year.

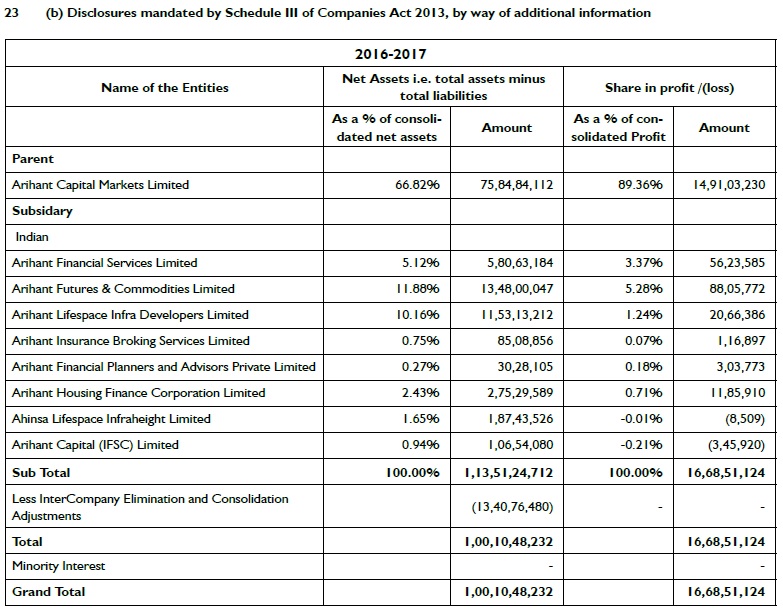

On checking past AR’s found the company has incorporated a subsidiary “Ahimsa Linespace Infraheights ltd”. The company is registered in Gwalior. For What ? Looks like the company intends to venture into real estate development. Maybe thats why its hoarding cash.

Company purchase freehold land of abt 5.4 cr in FY 12 and 5.6 cr in FY 14.

Can you clarify what is this inventory thing - about 13 cr worth of stocks company is carrying on the BS. Why is it not mentioned as Current investments.

It might have something to do with the nature of business. In any case what practical difference does that make. Both come under the head “Current Assets”.

Also company is carrying too much of cash on books deposited with the banks ( 60 Cr +). Due to this the ROE will always be low.

A business owner’s perspective is not limited to 1-2 year view but rather a 5-10 year view. Hence, they would preserve cash if they feel it might be useful in business a few years down the line. Cash is returned by only those companies that are in slow growth industries and are sure they would not need cash even a few years down the line. Capital Market is a sector where quite a few opportunities might arise in near future. Hence, cash preservation seems quite logical.

This is poor allocation of capital.

Can you suggest a better allocation with the same risk characteristics.

I was not able to understand why a company in the business of stock broking and advising clients as to where to invest would invest its own money in low performing bank deposits . Why not invest in stocks ?

The Company is in the business of capital market intermediation and similar activities, and is not an equity investment company.

We would invest in Valuepickr portfolio

The primary contributor of high returns of the valuepickr portfolio over the past few years is the P/E expansion. EPS growth has contributed to a relatively smaller share. The primary reason for P/E expansion is that valuepickr is followed by thousands of investors, quite a few of them blindly invest in the valuepickr portfolio. This piling up by thousands of valuepickr followers results in P/E reaching very high figures, that at least partly explains the high returns. However, investing in popular, overvalued stocks is never a good long-term wealth building strategy.

On checking past AR’s found the company has incorporated a subsidiary “Ahimsa Linespace Infraheights ltd”.

So long as this subsidiary is not significant, why bother.

Though the company has managed the business well in the past years. As per one news article, 14 lac demat accounts were added every month last year ( i hope i remember the fig correctly). Need to see how many delivery centres / customers company has added this year.

The right stress test period is 2008-12 when the capital markets were in bad shape and demat accounts were getting closed down. The company handled that period well.

Looks like the company intends to venture into real estate development.

Venturing into a new business is not necessarily a bad thing for any company so long as the company takes baby steps initially, does not risk a lot of existing capital, does not take debt etc.

Quarterly result is out and does not look good. May be rather than looking at quarterly results we have to look at annual results for these kind of businesses.

One needs to be patient with cyclical industries as first, it’s not feasible to catch the bottom of the cycle and second, the recovery is always weak during the initial stages. Basically, in the current market scenario, you broadly have the option of investing in either of the following two categories of companies:

Companies in cyclical industries that appear on the cusp of revival (such as capex, capital markets, etc) available at fairly moderate P/E. Such companies will gain both from P/E expansion as well as rapid EPS growth once the industrial revival takes hold.

Non-cyclical, growth companies expected to show consistent CAGR in the 15% - 25% range over the next several years, available at 40 - 80 P/E range. The problem I see here is that once the industrial growth cycle takes hold, funds will move from such companies to cyclical companies, resulting in P/E contraction. Hence, 3-yr investment returns will be zero from a Company that manages to grow it’s EPS at an impressive 26% CAGR over the next 3 years (hence doubling its EPS) but whose P/E halves from the current 80 (or 60) to 40 (or 20) over this period.

Having decided to go with option 1 and having selected a particular industry / sector for investment, the next logical step is the compare different Companies within that sector to find out which is the best option from the business quality and valuations perspective.

Let’s now compare Q1FY16 results of Arihant with Geojit BNP, a Company very similar business - both derive nearly 100% of their profits from Capital Market activities (India Infoline, Edelweiss, etc are not comparable as they derive only about 25% of their profits from capital market activities - rest comes primarily from their lending business):

Even Motilal Oswal has shown PBIT decline of 35% from its capital market activities. Hence, Arihant seems to have managed its profitability better than other, bigger companies available at much higher multiples.

Absolute delight to see the reply Alok. I am fortunate to be here and the learning is so steep. Thanks and would expect to see more such gems as clarifications coming.

Anyone tracking this micro-cap? Keen to hear your opinion on this stock now, as prices of many of the small/mid caps (Emkay, Motilal Oswal, Edelweiss, IIFL, Geojit etc.) which are either direct or proxy plays to the ongoing bull market have significantly increased over the past one month as well as one year. I believe that, this has happened for right reasons.

Arihant’s profit almost doubled over past year, but the stock price increased only 40% over that period. Current valuations of this stock look attractive to me with a P/E of 8.5, P/B of 1.29 and zero debt. It’s current market cap is just Rs. 123 crores. If I do a search on naukri.com, I can see 14 job postings by this company over the past 30 days.

Assuming that, we are just at the cusp of a long bull market, Arihant is a very curious case for me to look at. If everything goes alright, this cyclical stock may be benefited significantly from quick EPS growth as well as P/E expansion

Disclosure: I have already invested a small amount on this stock and exploring if I can invest more

LKP Securities Ltd, demerged from LKP Finance from December 2016, has been one of the oldest and reputed stock broking of the country since 1948 is today one of the largest multi dimensional financial services group and India’s first to be awarded the prestigious ISO9002 certified KPMG Quality Registrar, USA. Since 1948, LKP with its 3772+ outlets across India covering 200 cities in the country, including 25 regional offices at all the major cities, Continues to provide clients with a single source capable of meeting all their needs – be it Equities, Debt, Corporate Finance, Investment Banking, Merchant Banking, Wealth Management or Commodities.

LKP Securities Limited and its associates enjoy the following Registrations & Memberships :

Category I Merchant Bankers with SEBI, Membership of BSE & NSE (Capital & Debt Market), AMFI registered all India Mutual Fund Distributors, Member of Commodity Exchanges MCX, NCDX and DGCX (Dubai), Member of NSE for Interest Rate Futures, Member of MCX SX and NSE Currency.

The business verticals are as :

Equities :

Retail : LKP offers a wide spectrum of services that includes Equity Broking in Cash and Derivatives, Internet based trading, Demat services & Research services

Institutional : Clientele at the institutional desk include Mutual Funds, Financial Institutions, Foreign and Domestic Institutional investors, Insurance companies, Banks and Corporates. Some of our esteemed domestic clients include among others – UTI MF, Birla MF, LIC, HDFC MF, Pru ICICI MF, Reliance MF, Principal MF, Sundaram MF, Tata MF, Benchmark MF, ILFS, Canara Robecco MF, ABN Amro MF and FII clients include Morgan Stanley, JP Morgan, Matterhorn and Blackstone among others. Clients whom we have been serving for the past twenty-five years include UTI, LIC, IDBI, ICICI, Tata Group, Birla Group, and Dabur, Jain Irrigation, Emco, Godrej, JB Chemicals, Paper Products and UB Group of Companies among others.

Fixed Income Markets : LKP is recognized as major dealer of Fixed Income Securities, executing deals for Banks, Institutions, FIIs, MFs, Insurance companies, Primary Dealers, large Corporates, PSUs & PF Trusts.

Primary Market Division : LKP’s vibrant ‘Primary Market’ Division does syndication business in IPOs’, Company Fixed Deposits, Capital Gain Bonds (U/s 54EC), 8.00% Saving (Taxable) Bonds floated by RBI & various bonds floated by Central & State Governments.

Mutual Funds & Insurance Advisory : LKP Investment Advisory Services Offer tailor-made wealth management services to Retail, High Networth Individual and Corporate Clients.

Commodities : Alpha Commodities offers a complete bouquet of client- friendly services in the burgeoning Commodity Futures market.

Currency Derivatives : With the launch of currency derivatives, LKP offers its clients yet another segment for trading. Jointly regulated by SEBI and RBI provides traders with another lucrative trading avenue.

Valuations : A 70 year old closely held company with nationwide retail client base along with marquee institutional & corporate clientele is trading at a market cap of ~60 odd crore. Company reported total income for March Quarter of Rs 16.68 Cr and Net Profit of 3.32 Cr giving an EPS of 0.45 per share. Expected FY 18 EPS is Rs 1 per share. The stock is trading at just 8 times FY 18 , while the industry PE for brokerage companies is above 20 making it a good investment candidate for long term growth, as new generation has taken over the company with new team in place to drive its overall business to create shareholder value after demerging the company from LKP Finance Ltd.

Very true mambajamba. I had mentioned the naukri postings just as an indicator, as there was no easy way for me to verify the same. Vice versa also can be true. There may be a few people moving from Motilal, Geojit, Emkay etc. to Arihant also. I think, the best place to look further is linkedin. I see around 270 results in linkedin under “People” category for Arihant. When I get time, I could possibly go through each one of those (if linkedin allows me to view the information) and study the pattern. It might be time-consuming, but I feel it’s really worth doing it, considering the attractive valuations of the company.

BTW, the stock ran up 20% yesterday and hit upper circuit with a very large volume and a delivery percentage of 77.

The stock is definitely cheap by any parameter that one can check. Emkay has given a good run up recently after Porinju Anna entered the stock, i won’t be surprised if Arihant will also see similar re rating. The margins r superb and company is expanding its operations rapidly. Just waiting for the AR before taking the plunge. Ticks all the boxes as per me.

One of the Independent Directors Mr. Shailesh Kumath resigned recently and a new Independent Director Mr. Ashish Maheshwari joined.

Stock made a high of Rs. 102.80 last week (it was Rs.59 on 12-Jun-17, when I posted my first message above) and subsequently corrected to Rs. 86.70, which seems to be due to profit booking.

I continue to see many job advertisements by this company. It has updated its job openings page (http://www.arihantcapital.com/careers/job-openings) on the company website on 8-Jul and has included 6 new job profiles there for various locations. These are apart from the many naukri.com advertisements which I had been observing for the past couple of months. Overall at this point of time, I see job postings for 11 locations and for many of the positions, there are multiple vacancies across locations.

Company has come up with the Annual Report of FY 2017. Those who are interested, can go through it at http://arihantcapital.com/upload/financial_report/Annual%20Report%20copy.pdf. CEO’s views (page 3 in the pdf) and Management Discussion (page 35) paint a rosy future for the company and the sector in which it is in.

All its peers (Emkay, Geojit, Motilal Oswal, IIFL, Edelweiss etc.) have again come up with great profits from their capital market activities in Q1’18, as it was the case in Q4’17. I feel, Arihant’s valuations are still the cheapest among them.

Operating margin of 40 (as against Emkay’s 33) is probably the highest among all its respected peers in the industry. Its past performance throughout the history is also more consistent than most of its peers. Though a lot of P/E expansion happened over the past few weeks, this stock continues to enjoy one of the lowest P/E (16.59) in the industry (as against the P/E 40 of Emkay). Arihant has been constantly and proactively expanding in terms of their number of investment centres, based on the data available from their Annual Reports and Quarterly Results. Company has also been experimenting on low cost housing as well as housing financing in a conservative way, without straining its balance sheet in any way.

In the past few months, they also have come up with numerous job advertisements in naukri.com as well as at their company web-site. I feel, one reason for the increased Expenses during Q1 must be due to the above expansion related activities. As most of the job advertisements have vanished from naukri.com by now, I feel, they have filled up most of their open positions for the time being.

First of all, let me congratulate you for picking up one of the unnoticed gems in the industry. The company has been doing extremely well in its space of broking and asset management. However, it is commanding a valuation which is far lower than its larger peers. I have some key questions, however, regarding the sustainability of the growth going forward.

From what I understand from the annual report, the company is deriving more than 80 percent of its turnover from capital market activities. Am I correct in my assessment here. This also exposes it to cyclicality in this segment.

Along with the growth in turnover, the margins are also expanding. This looks like a very encouraging sign as it means that the incremental cost structure is getting into more lucrative revenue streams. As per their annual report, they are getting into distribution in a big way.

What are the growth areas that you see emerging in this particular story? Do you see growth from a particular asset class/ segment going forward or are there multiple levers to this story.

In your assessment how good is the risk management practices of the company. How do they compare to the best in the industry. As you know for firms engaged in capital market activities, risk management practices are paramount.

Overall, have taken a starter position in this counter as it looks like a promising growth story and currently I believe is the only reasonable growth story in the entire sector. Keenly tracking and adding positions here. FY18 profits should be around Rs.25-30 Crores (conservatively speaking) which essentially means that its is trading at about 10x. Even if the valuation doubles to 20x, we are looking at a clear 2x here.Would prefer to increase allocation between 135-140 though. However, I doubt whether the market will give me that opportunity.

Thanks for raising these queries. I will try to answer to the best of my knowledge. Please note that, I am a person of Computer Science background, who never learned finance/ commerce/ economics, hence you might find a few anomalies in my responses below. Please do not hesitate to point out any mistakes, so that I get a chance to improve further.

Sorry for the long reply, but I wanted to make my whole thought process very clear. In the below response, I am trying to address all your queries, but may not be strictly in the same order.

I agree with your opinion that, Arihant is an “unnoticed gem”. In fact, after doing my initial due diligence of this stock during May-17 (I just accidently stumbled upon it, as I was comparing the micro/ small caps on the NBFC sector on MarketsMojo), I got really dumbfounded looking at its quality versus undervaluation. My first impression indeed was that, finally I have found out a real “hidden gem” in its true sense!

However, I was still doubtful, why the stock price was not moving up, hence I had posted a message on this forum during June-17, as you would have already noticed. However, my above message failed to get the attention of most of the ValuePickr members then, as it was a microcap with market cap of just about 100 crores and never recommended by any analysts/ brokerage houses. I think, brokerage houses do not ever recommend the stocks of other brokerage houses .

Well, I should also thank ValuePickr and the boarder @AlokBhola, who really convinced me with his earlier messages on this forum that, this stock indeed is a cyclical one (my earlier imagination was that, only stocks like sugar were cyclical ) and as cycle turns positive and stay there for a prolonged duration, we should see a huge upside in these stocks. I looked at the chart of Emkay Global during May-17 and realized that, Alok’s reasoning was spot on! Thanks Alok.

Arihant’s FY17 net profit was 37% higher than Emkay’s, but its current Market cap is just 330 Crores, as against Emkay’s 757 Crores. Emkay had an early runup in its stock price as compared to Arihant, may be because it is listed on NSE and also got the attention of marquee investors like Dolly Khanna and Porinju.

However, till one month back, I was still doubtful if India had really entered a strong bull market. However, by now I have started believing that, we are already in a raging bull market. One reason for the above belief is that, my core portfolio (mostly micro, small and midcaps) which includes stocks like Arihant Capital, Shankara, Emkay, BEPL, Phillips Carbon, Himadri, Edelweiss, Manappuram, Capital First, DHFL and PNB Housing collectively increased by more than 40% in just the past 30 days, in spite of the ongoing North Korea tension and the earlier China tension.

Also, my belief about sustainability of this ongoing bull market is strengthening day by day. I will explain the reasons below.

Ever since I spotted Arihant and initially purchased it in May-17 for Rs. 57, I have been tracking it very closely. I kept on getting all the right “vibes” from this company time and again. I could sense that, it is a business house with the perfect balance of aggression and conservatism. If you browse through its history, it has never negatively surprised its investors, even during the toughest of market conditions, while most of its bigger peers ran into heavy losses. It has been a regular dividend payer. Its operating margins and ROCE had been consistently higher compared to all its notable peers.

Now, I don’t know if this would be against value investing principles, but my belief is that, as stock investors, we should leave certain stuff to perception and sixth sense also. I constantly tried to gather and verify a lot of details about this company using my tool and guru “google search”. I currently have the perception that, this company has the right ambitions, discipline, potential and the right governance to become a large cap like Edelweiss one day. I am again disclosing that, this is just my intuition for the time being. If I am not supposed to write this way on this forum, please caution me and I will delete this paragraph.

I formed the above intuition for various reasons – looking at the consistency in its cash flows, dividend payment, timely filing of disclosures, performance during toughest of the times, ability to protect and constantly improve its margins etc. Even seemingly cosmetic things like presentation and user-friendliness of its website and availability of useful information over there, how they keep the information at their website upto date speak a lot about their quality consciousness and customer-orientation. The quantity and clarity of information shared in their Annual Reports and Quarterly results (best-in-class for a microcap) talks a lot about their Corporate Governance.

During my study, I came upon a site (I do not recollect the website now) which compared all the major stock brokers in India on number of customer complaints and Arihant had the least number of customer complaints per customer and it was significantly ahead of others on that statistic too. I have been regularly monitoring the naukri.com site and their company website on the way they come up with job advertisements, and constantly filling up those positions in a disciplined way.

I have formed a belief that, they are a very tech-savvy company, which will help them in efficiently running all their business operations and also help their online trading business a lot.

A simple Google search will reveal the fact that, they are also making their Research activities stronger and stronger day by day. This will in turn help them to differentiate from their competitors.

If you carefully analyse the data provided at a brokerage-comparison web site (Stock Broker Comparisons in India 2020 | Brokerage, Video Reviews), Arihant had far more competent brokerage rates compared to almost all other full-service stock brokers and Arihant’s rates were even comparable to discount brokers like Zerodha. In spite of the above, Arihant has one of the highest operating margins in the industry.

Arihant had 690 investment centers (overall 1.30+ lacs of customers) as on Mar-17. The number of investment centers have increased steadily and stand at 750+ by Aug-17. During this period of time, they have also come up with numerous job advertisements. I think, their increased expenses during Q1 can be correlated to the above activities and we can expect even better Operating Margins in the coming quarters.

I feel that, as we traverse deeper and deeper into the bull market, their operating margins and ROCE will keep on improving. @AlokBhola has mentioned above that, its ROE even touched 60% during the earlier capital market boom years!

Let me try to explain, why I believe that, companies like Arihant or Emkay which derive their maximum income from stock broking activities are likely to grow at higher rates of profits over the next many quarters/ years, as compared to other companies in its sector (capital market/wealth management/ stock broking) or other _NBFC_s or Housing Finance Companies. Stock broking business by its nature is such that, as the volumes increase, the topline (sales revenue) increases, but the bottomline (profit) increases in a disproportionately higher way. As per my judgment, this is due to the reason that, the business (due to its very nature) is able to handle more volume with less increase in the resources (employees, computer software etc.) and thereby lesser increase in cost.

Hence, we have a non-linear relationship between volume and the cost. As we get into more and more deeper into this bull market, more and more money pour into equity market, hence volumes for Arihant will increase proportionately. However, its profits will increase in a disproportionate way, as explained above. Let me substantiate this hypothesis with one more fact. ROCE is the primary measure of how efficiently a company utilizes its all available capital to generate additional profits. Arihant`s ROCE as of Mar-17 was around 28, whereas it was just around 9 in 2004, when market condition was not favourable. I think, Arihant will keep on improving its ROCE significantly from now onwards due to the reasons explained above.

What is the reason for the current bull run on the stock market and how long is it to continue (5 reasons why you can’t keep the bulls tamed on D-Street for long - The Economic Times)? Well, this is what the big bull Rakesh Jhunjhunwala said during early May this year: “Tsunami of local money will come into the local market. Morgan Stanley is predicting that USD 425-825 billion in the next 10 years to flow into markets”.

Even a person like Saurabh Mukherjea of Ambit Capital, who more often comes up with doomsday predictions and negative views about the market seems to be very bullish on stock broking and asset management companies and that too for a period of even the next 10 years.

Here is a summary of what he says: “People have realized that they cannot really expect to save through real estate and gold and hence formal financial savings will rise rapidly over the next 10 years. There is good reason to believe that now we have fallen out of love with real estate, there is good reason to believe that the amount of retail savings that will come into the stock market will continue accelerating over the next five to ten years. We are not very far away from the point where SIPs alone could be a billion dollars a month of inflows into the market and even that I think is scraping the surface. We have enough wealth in our country, enough savings in our country to believe that the SIP number can go considerably north of a billion a month. On all of those fronts, there is plenty of upside in this theme. There are fine credible companies, clean honest companies on the savings theme whether it is insurers, asset managers or brokers, buy them, sit on them for a long time. This is a safe theme which will give you good returns.”

Thanks to demonetization and interest rates reduction, Indian households have started pouring money to stock market and the above amount is steadily increasing quarter by quarter, especially after demonetization. Let us examine the actual data on this:

SEBI website (http://www.sebi.gov.in/sebiweb/other/mutualfunds.jsp) provides domestic mutual fund investment information. As per the data provided, I calculated that, for Q4’17, the MFs have invested Rs. 11,465 crores on equities in Indian market. During Q1’18, their investment was Rs. 29,708 crores. And, during the first two months of Q2’18 itself, they have already invested Rs. 29,741 crores, which already exceeded the total investment done during the 3 months of Q1’18!

The above money is unlikely to stop any time soon, for the same reasons mentioned by Rakesh and Saurabh above and there is good probability that, the money invested increases every month.

Yes, you are correct. They currently derive more than 80% of their revenues from the capital market activities. However, for all the reasons I mentioned above, I believe that, current positive cycle for the capital markets sector is going to stay here for a very long period of time (many years), with minor dips and highs in between.

Also, company has been experimenting on Affordable Housing as well as Housing Financing for some time now, though I have not been tracking much on those activities of theirs. Though they are doing it in a small way without adding any strain to their balance sheet, I feel that, they might have gained sufficient expertise in the above two businesses by now. Following is what their recent Annual Report says about their diversification of business:

“We believe in diversification and have added multiple revenue streams over the years. Our Company launched an affordable housing project in last fiscal, which we discussed in our previous annual report. We are happy to inform you that the progress of Arihant Residency project located in Pithampur has been promising. During the year under review, development of Sector 1 has been successfully completed and sale of plots is well under progress. Few families have already moved to their houses in the township enjoying a quality life. The Company also formed a new subsidiary in the name of Arihant Capital (IFSC) Limited during the year for establishing a unit in GIFT SEZ to provide international financial services.”

Very true, this indeed is a very encouraging sign.

I believe that, their stock broking engine will fire on all cylinders in the coming few quarters and would provide them the sufficient cash flow to make them think about expanding their other businesses in a major way, including the affordable housing, housing finance and the Insurance broking.

There is a conducive market climate for all these businesses, hence we can confidently conclude that, they have picked up the right sectors/ businesses for diversification. Additionally, as we get more and more deeper into the bull market, all their capital market activities will generate increased cash flows.

In FY18, their focus would be on distribution and digitization. Let me quote from their recent Annual Report:

“The economic landscape in FY2018 is likely to be quite different from the one in previous years. The world of investing is changing. Technological changes are significantly impacting customer expectations, more and more investors are opting to invest in mutual funds {especially via the SIP mode} and the clients are looking for the best infrastructure at most competitive cost. The rapid speed of innovation, disruption in the financial technology space present challenges and opportunities and we are geared up for both.

We intend to capitalize on the growth of the retail brokerage industry, focus on attracting active traders, long term investors and franchises. The renewed interest in the equity markets will help us reach out to a wider population. We strive to enhance the client experience by providing wide range of investment products and services, enhanced trading tools and capabilities and unbiased objective advice customized to our customer’s needs."

From a broking house’s perspective, I think the key factors to consider would be the risk assessment of its customers and the legal relationships with them, protection of customer assets, financing of their Margin and the various other internal controls by the company. Company has also well documented many of the risk factors under the sub-heading “Risk factors relating to our business operations” on page 28 of the latest Annual Report.

However, from public media, I could not find much details regarding the specific risk mitigation measures taken up by the company. Here, my “intuition” has been that they understand these risks very well and as an ongoing process, will continue strengthening the mitigation measures, assisted by their software systems.

I am providing one example. Following is one thing that they claims at their website: “We have cutting-edge trading platforms and tools which include smart risk-management tools like conditional orders and alerts to help customer’s profits and limit losses”. I myself have not been a customer of Arihant, hence I cannot comment from a customers’ “feel” perspective here.

Hope, I have addressed all your queries in a reasonably good way. If you have any more specific questions, please do let me know and I will be more than happy to do a more thorough research on this company.

Hi Madhavikutti, good write up explaining in details the growth prospects of Arihant, can you let me know for knowledge purpose does ABCapital also into something similar to Arihant apart from their insurance, AUM etc.

This is being asked more to evaluate both the firms from valuation point of view and invest in one of them.

")