Aptech

Market cap – 2087 cr

P/E- 31

ROE- 29% , ROCE- 34%

Aptech is in the space of non formal education and training. They operate in majorly two segments – retail segment and the institutional segment.

Retail segment

In the retail segment Aptech has its centres where they conduct training and courses for students. Last year they had 1,19,000(FY23) students enrolled vs 86,000(FY22) a year before. Aptech operates in two main areas-

Media and entertainment

Beauty and wellness

These 2 segments contribute 90 % of the revenues from retail segment

In the media and entertainment space Aptech is a market leader has a share of 75-80%. Their brands are Arena Animation and MAC are market leaders in this space.

In beauty and wellness they have a tie up with Lakme in the form of Lakme Academy. They are the market leaders in this segment as well. This is a fast growing segment.

Their retail revenues were 285 cr in FY 23 vs 129 cr in FY22. However they are not comparable on a like to like basis. This is due to the the change in their revenue recognition model. The company operates through franchises in retail segment. In the earlier model only the royalty fees was recorded as revenues. In this model the student fees paid is recorded as revenues. IN FY23 , 58% of the companies revenues were recorded from the student delivery model and 42% from the royalty model.

On a royalty basis a like to like comparison would be 121 cr for FY 22 vs 174 cr for FY23, indicating a growth of 43% inline with the student growth rate of 38%.

The fees charged to students varies depending on the segment, duration. For the beauty and wellness segment the courses are typically short in duration, ranging from 10,000- 60,000. In the media segment we have courses of higher duration, hence higher costs – around 1,00,000.

Placements for students

Company claims to have an excellent track record for placements. Some of the employers for the company are

1- Red Chillies, Amazon, Byjus, MPC- in media and entertainment space.

2- Loreal, Nykaa, Lakeme, Urban Clap in beauty and wellness space.

3- Tata Elxsi- in IT learning space

The company claims to have 2.5x the number of jobs for students enrolled in long courses ( these are the students who actually come for placements). This seems to be a high value add for students. The typical packages fall in the range of 25,000 to 30,000 .Company claims that the ROI of franchise owners falls in the range of 30%.

Hence this business model seems like a win win for all the stakeholders involved. Also given the huge gap between graduates passing out each year and the employable individuals non formal training institutes like Aptech seem the need of the hour.

Cost structure

Interesting thing to understand is the scope of operating leverage. The retail division had a PBT of 68 cr in FY23. In FY 22 the PBT of retail division was 41 cr. We can see a 65% jump in PBT with a revenue growth of 43 % on a like to like basis.

This division seems to have a fixed cost of 25-30 cr. The variable cost seems to be roughly 40-45% of sales(if sales are counted on a royalty basis).

Fixed cost might grow at best the inflation. Hence we can see the scope of operating leverage present

In this division the company has 85-90% of revenues from domestic side and 10-15% of revenues from the international side as of now.

The scope to grow in both places is huge. Company expects a growth of 25-40% in this segment over the next 5 years. This number seems reasonable based on the jobs being created in the media and entertainment space as well as the beauty and wellness space.

Also company seems to be entering into new segments of Aviation and preschool which might start contributing meaningfully.

Right now Aptech is present more in class 1 and class 2 cities. It is yet to penetrate into class 3 and class 4 cities – this might be the next place for growth in the retail business.

Institutional Business

In the institutional/ enterprise business Aptech carries out entrance exams for universities/ PSUs, companies. It can run end to end process or partial process- it involves registering students, hiring space and machinery, setting question bank, providing invigilators, conducting test, providing software,etc.

Aptech clocked revenues of 172 cr from this segment last year in FY 23. They are expected to clock revenues of 250 to 270 cr from this segment in FY24. This was the management’s commentary in the latest concall based on order in hand. Management is very bullish and expect to clock a revenue of 350-400 cr in this segment over the next 3 years.

The market size in this segment is around 1500 cr. Out of this 1000 cr is catered by TCS- which is the big player in this industry. Managements expects market size to grow to 3500-4000 cr over the next 3 years. Even if Aptech maintains its current market share it can clock 350-400 cr over the next 3 years. This obviously depends on the contracts Aptech can win and retain.

Cost structure

The institutional business also seems to enjoy great amount of operating leverage with scale.

In FY 23 we did a sale of 172 cr vs a sale of 97 cr in FY22. The growth rate was around 75% . While the PBT from institutional business was 38 cr in FY23 vs 16.5 cr in FY22 , implying a growth of 230%. This business seems to have a fixed cost of 20-25 cr. The variable cost seems to be 65-70% of sales. A stable PBT margin of 25-30% with scale seems possible. As per the management anything over the breakeven translates into 30-35% of sales to the bottomline.

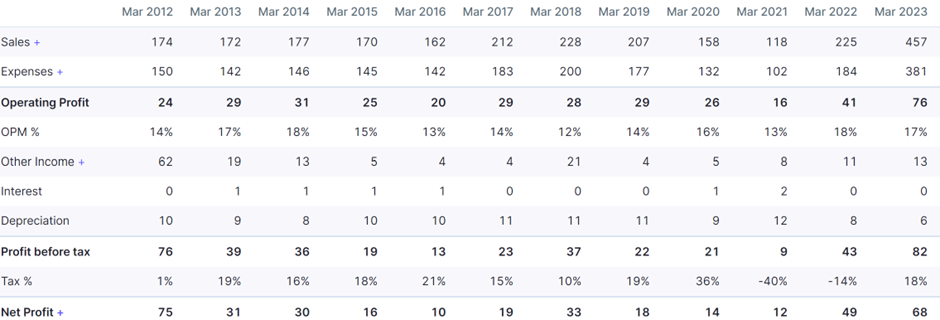

Attached above is snapshot of last 10 years P & L of the company

Attached above is snapshot of last 10 years balance sheet of the company.

Overall Aptech looks well poised for growth for the next few years. Being an asset light business one can expect it to generate significant amount of cash. Will be interesting to see how the company uses the cash being generated.

Risks

• Not able to retain existing contracts or win new contracts in the enterprise business.

• Growth being saturated in the retail segment

• Company not utilising the cash properly and does a bad acquisition.

• New players entering in the enterprise business- it is not clear what exactly is the moat of the company in the enterprise business

Disc- Invested