I think people are still not getting the game that’s being played here. I hardly see any post looking at the nitty-gritties and nuances of the financial engineering involved.

Let’s start from the beginning - or at least from 2016.

Potential Investment and Finance in 2016 had 1,85,00,000 total shares outstanding and was a penny share of an empty business. The name of the business though might suggest of what was to come - a “potential investment”.

Here are some brief notes on what has happened to Potential Investment when it became “Best Steel Logistics”

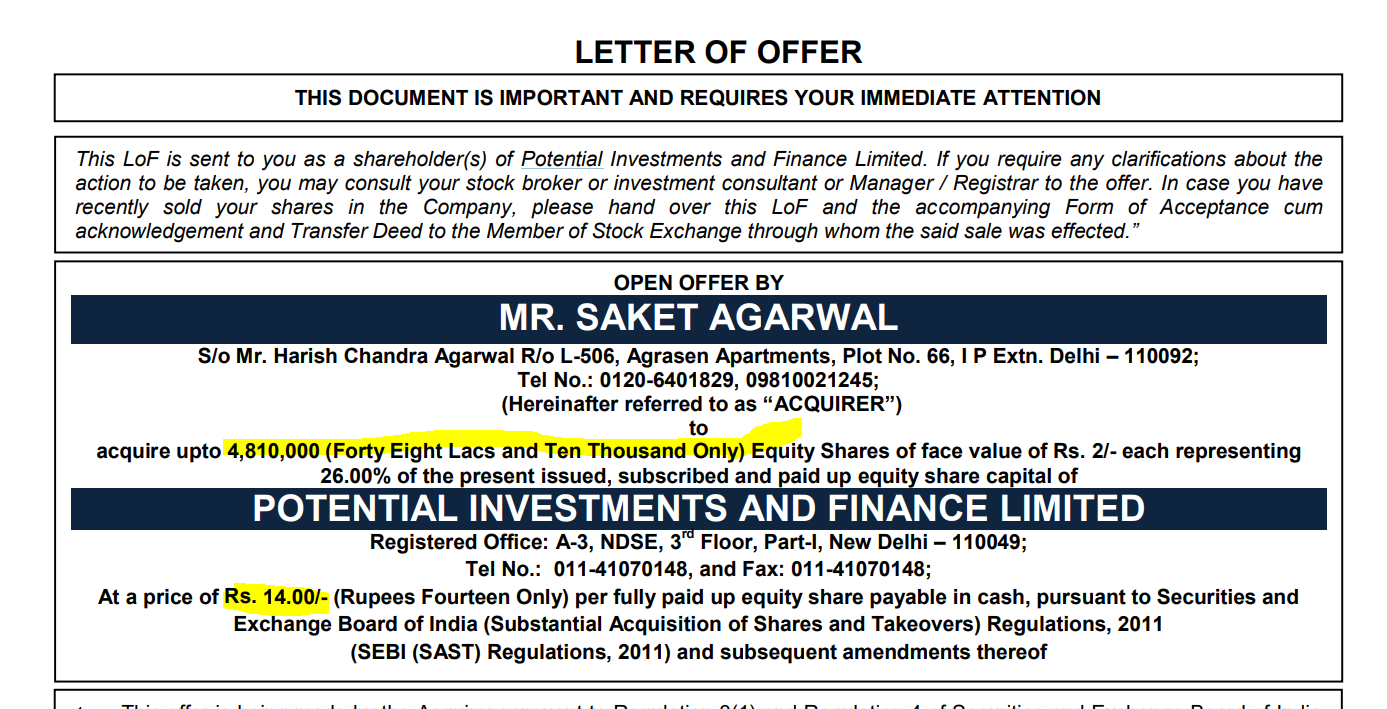

- Saket Agarwal open offer for 48,10,000 shares at a price of Rs.14 (21st Jan to 28 March 2016)

- Saket Agarwal held 3800000 before May 2016 - Presumably shares purchased in the open offer at Rs.14

- 4125010 as of May 2016 (Bought 3,25,010 shares off market) - At Rs.14/share

- 5665010 as of June 2016 (Bought 15,40,000 shares from Kanav Gupta and Manoj Gupta at Rs.12/share) - 30.62% of the company

- 7222910 as of Dec 2016 (Bought 15,57,900 between Sept and Dec off-market at Rs.12/share) - 39.04% of the company

Dec-16 to Jun-17 - Saket Agarwal sat tight. Occasionally selling a bit

Meanwhile Jan-16 to Jun-16 - RG acquired 28,00,000 shares from open market as Public at same Rs.14/share. This needed no disclosure but you can verify this from shareholding pattern from 2016.

June-Dec '16 - RG sat tight

As of Dec’16 - Saket Agarwal and RG held 1,00,22,910 shares together - at an average purchase price of under Rs.14.

Total Investment so far - Rs.14 Cr

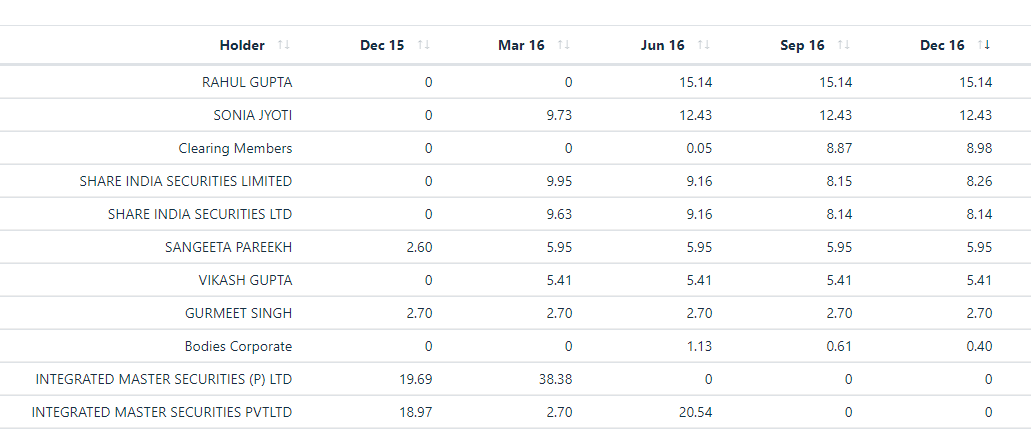

Now the story isn’t over there since there are several holders like ‘Share India securities ltd’ and ‘Integrated Master Securities’ and ‘Sonia Jyoti’ and ‘Vikash Gupta’, ’ Sangeeta Parekh’ who have all bought large holdings totaling of about 80,00,000 shares - around avg. price of Rs.20.

So now overall control via promoter + large public amounts to over 1.5 Cr shares acquired at an average price of Rs.20 or so. Overall spend so far? Around 30 Cr for about 90% of the company. Not bad.

Overall disclosed promoter holding though as of Dec 16 was only 39%. The rest would be transferred in the course of time because market likes increasing promoter holding over time right?

Dec’16 to Dec '18 - Price appreciates from 60 to 120. Those 1.5 Cr shares are now worth 180 Cr - notionally anyway. Its cornered and closely held so what’s its worth is notional.

Then along came Lakshmi Metal Udyoj a fully owned subsidiary of APL Apollo and bought 55% 16970000 shares at around Rs.135 - About 230 Cr? Considering initial cost of just about Rs.30 Cr put in, this is 7x return for the 90% cornered shares which benefited. On top of it whatever else was left is also being offloaded slowly at much higher prices by Saket Agrawal. I can’t even fathom the returns this man has made in 5 years time. He still continues to sell to this day and no has been reclassified from Promoter category to Public once his holding dropped under 10%. Oh there’s also some warrants which were subscribed and later sold.

Clearly someone benefitted quite well from this saga without even looking at underlying business. Now let’s look at the underlying business then.

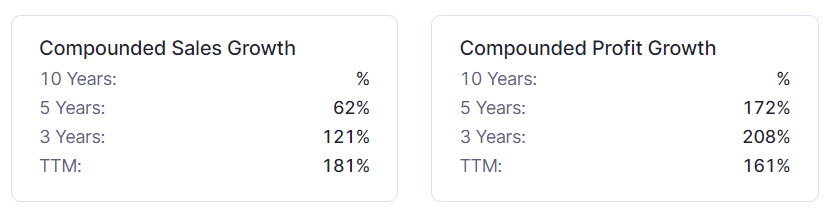

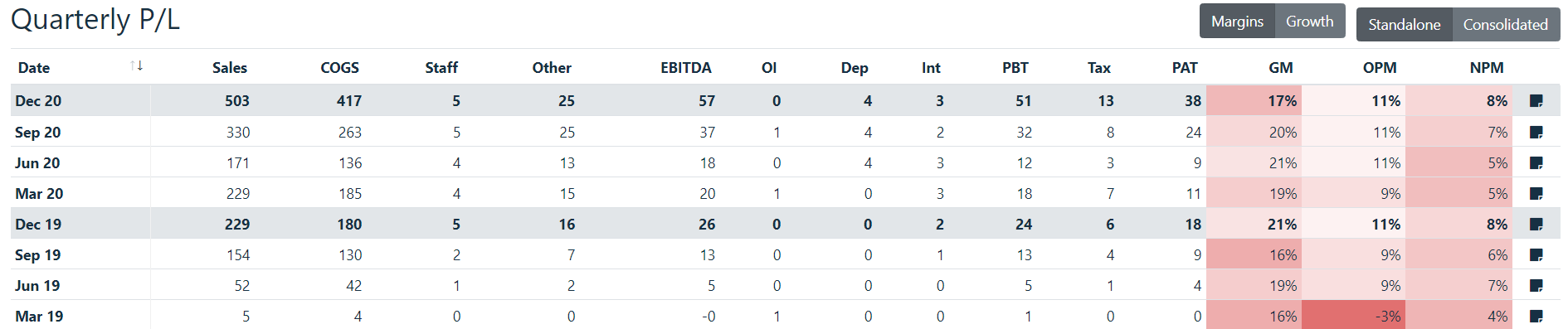

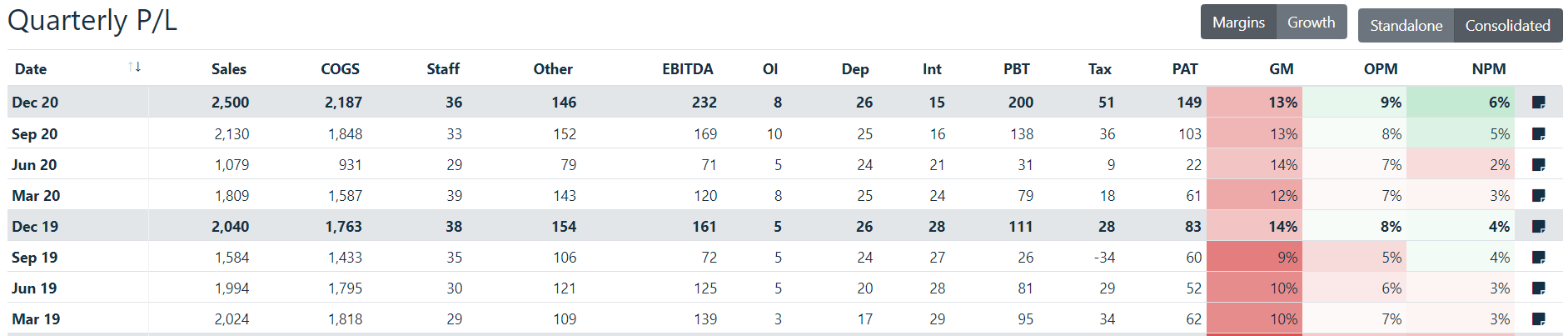

Here’s the Quarterly PNL trend of Tricoat

and APL Apollo Tubes

There’s about 5% difference in GM which only translates to 2% difference in OPM. This tells me that whatever value-add is being done, costs the business maybe through higher labour or power costs. There really isn’t anything significantly awesome about this business looking at the gross margins in isolation.

But why do the return ratios look better than APL Apollo Tubes?

- The company is probably leveraging APL Apollo Tubes ad spends (Looks at Chaukat ads featuring Amitabh Bachchan being featured in APL Apollo’s youtube channel for eg.)

- It is leveraging APL Apollo Tubes R&D spends

- It is definitely leveraging APL Apollo’s brand equity

- It is leveraging the distribution channels of APL Apollo

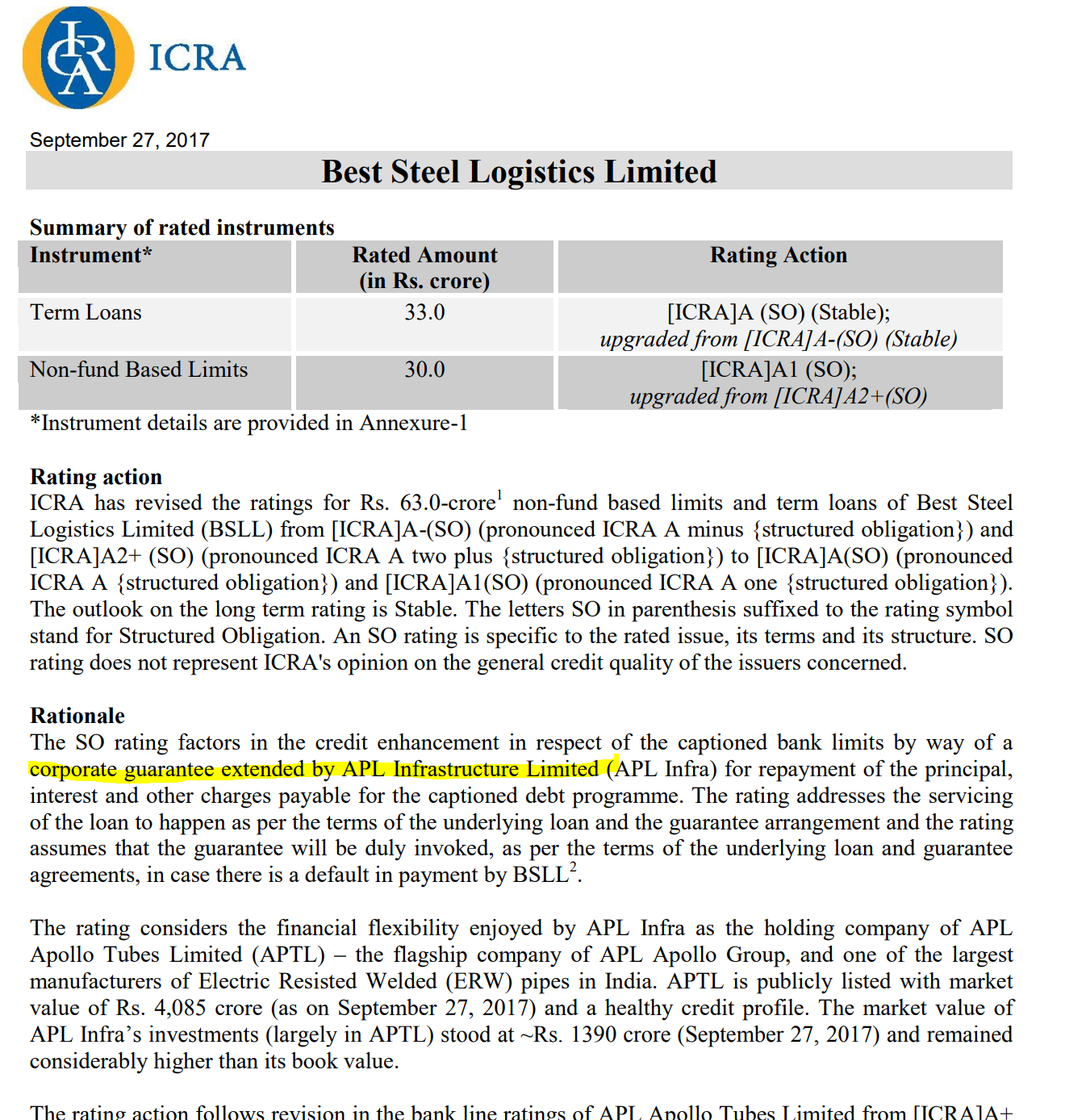

- Its debt is secured by APL Apollo Tubes (Check ICRA’s rating or FY20 AR). In fact even Best Steel Logistics had its debt guaranteed by the promoter of APL Apollo.

So if this business is looking better than it should, understand the nuances that are making it so, especially when buying something like this at 12 times book. Now coming to the amalgamation - this ideally should have always been part of APL Apollo Tubes - But it would never have got the market fancy and some people wouldn’t have made a few hundred crores in the process with a miniscule investment. If you want to know what it would have looked like had this not been a separate entity, simply add the numbers of tricoat to apl apollo and look at the sales/pat growth and think of what you may have paid. It is now being merged because the game is effectively over and all the benefits that had to accrue, have already accrued, although in its wake it has left a huge corporate governance question mark.

Disc: Traded in Apollo Tricoat short term in 2019. No holdings since.