in my understanding tricoat is almost manufactured based on pre bookings with advance payments,so possibility of such kind is remote in near future, in my view till 2025 at least until the expiry of non sharing of this technology to other players

6 Likes

It is noteworthy that only sharp falls in steel prices lead to inventory losses for APL Apollo and Tricoat. Slow and gradual fall in steel prices are unlikely to impact their profits

5 Likes

Distributor meet notes on both Apl Tricoat and Apl Apollo:

- Have seen the company grown exponentially in the last 2 decades. They used to have a shop near to our place in Chawri Bazaar by the name of Bihar steel tubes.

2)Company has created 3 levels amongst the distributors depending upon the sales. We are a part of the fist hierarchy (top level something couldn’t understand the name). We regularly receive products from the company for sampling.

-

Post the lockdown period, in June. APL Apollo was the first steel tubes company off the blocks in terms of re-starting the production and supply. Others took time and some companies went bankrupt in the industry. One major change that happened was the receivable days. Now, we pay on the same day we have received the goods. This was painful initially, however, we have tightened our credit from the retailers (receive payment on the same day or with a lag of 1 or 2 days). I personally wanted to confirm this point, and he indicated that the entire industry has moved to cash and carry.

-

Coming to Tricoat, Chaukhat costs Rs2 per kg more than the normal pipes that we receive. (He indicated the per tonne price of other Apl products was at Rs56 per kg, chaukhat costs Rs2 kg more). Planks are priced Rs5-6 more per Kg.

-

Seeing good demand for Chaukhat within Delhi. Other main competitor is Tata in this category. However, preference is given to Apl Chaukat, delivery time is much lower. Tata you have to order 20-30 days in advance as the company isn’t willing/aggressive to keep inventory. You have to be aggressive in steel tubes/pipes business. Seeing good demand for Chaukhat from Affordable housing projects and major demand in Delhi is from South Delhi and Mundka region.

-

Chaukhat’s major markets are Uttaranchal and Uttar Pradesh. Major sales are coming from these 2 regions. Chaukhat is the most selling product when compared to Plank and Chequered Sheet. Chequered sheet was launched 6monthss ago, haven’t seen a good pick-up in this product.

-

Company will be launching In-line Galvanization pipes sometime, these will be very highly-priced from what we have heard. They are also launching colored pipes, work for which has already started at their Raipur facility.

My inference and thoughts: Largest market for Tricoat products are from Uttaranchal and Uttar Pradesh. The company is slowly launching in other areas of India. Seems quite interesting, if the products gain further acceptance in other parts of India. The market potential could be huge.

Disclosure: Tracking position and I am not a SEBI Registered advisor/analyst. This is not a recommendation. The distributor has 3 warehouses within Delhi, I will be visiting one soon. One more thing that the distributor pointed to was that Tricoat can potentially grow to 1Lakh tonnes per month.

43 Likes

Hi, which of the two companies is launching in line galvanization and coloured pipes?

The parent company- Apl Apollo will launch the colored tubes and Tricoat will launch the ILG ones

5 Likes

thank you so much for your amazing scuttlebutt ![]()

Found an amazing video explaining evolution of APL apollo:

It’s a bit cringe but definitely amazing explanation for the company evolution. It is from the company’s official YT channel so the company definitely is vouching for the info.

PS:

- it is in hindi, if anyone would like english notes, please reach out to me. I’ll only add notes if there is enough demand because it would be quite a laborious process.

- The orator is a famous YT personality with 12M subscribers. Dr. Vivek Bindra: Motivational Speaker - YouTube

On a related note, listening to Machine Gun kelly “Rap Devil” play in the background as the speaker is introducing Sanjay Gupta in the APL Apollo Steel for Green event is one of the raddest thing I have seen in the investment world. ![]() : Exact timestamp where this happens is here.

: Exact timestamp where this happens is here.

9 Likes

Tata is not present yet in special tubes segments like ILG, Chaukhat, Planks etc. Surya Tubes has presence in Chaukhat segment. Rest of the products are almost exclusive to Tricoat.

Tata Steel competes with parent APL Apollo segments and it is correct that they lack aggressiveness of Apollo. Also would like to add that Tata Steel’s lead time for supply of tubes is much larger says 30-45 days and due to excessive demand their stockyards are dry.

4 Likes

- All time high sales volume of 72000 MT in Q3FY21. QoQ growth of 20% in sales volumes.

- This represents a capacity utilisation of 83%.

- Large increase in Apollo signature volumes.

- Chaukhat at 87% capacity utilisation.

- ILG production has not started yet and that capacity is being utilised in fungible way for other production.

Disc: invested, full portfolio here

9 Likes

There is lot of talk about chaukhat, but if you see latest exchange release, major part of volume is coming from apollo signature and apollo elegant. Asked few delhi friends, not many hv seen the products.

So biggest question is from where the demand is coming for elegant and signature pipes? Retail or some steel furniture companies buying directly or builders ?

Products available in only 4-5 states , so very difficult to dig deeper in this.

Anyone can share more info, will be very helpful.

2 Likes

Same question was being raised in their Ratings upgrade report from ICRA!

The rating, however, is constrained by the limited track record of the ATTL’s operations with facilities commissioned during the last fiscal. Notwithstanding the favourable initial response, the acceptability of triple coated tubes and related products in the targeted markets is yet to be established.

2 Likes

Great numbers from tricoat:

- Core business ROCE of 60% (on full capacity utilization). Working capital at 0 days.

- Total capital employed = Gross block = Rs 9820/ton

- EBITDA for Q3 at 57cr, 100% YoY increase. 54% increase QoQ.

- Net profit at 38 cr. 100% YoY growth and 58% QoQ growth.

- Operating cash flow was Rs 110 cr in 9MFY21 (99% of EBITDA)

- Revenue of 500cr, growth of 51% QoQ.

- EBITDA/ton at Rs 7872 vs 6137/ton in Q2. (This level of EBITDA might not be sustainable. No word from management in this regard yet. Will watch concalls for more updates regarding this).

- Target to achieve full capacity utilization in next 2 years.

Disc: Invested, full pf here.

9 Likes

Q3FY21 Notes

Few metapointds:

- In the metanotes I have also included whether the commentary applies to entire consolidated company or only tricoat.

- Most of the questions were in Hindi so i could not transcribe my learnings from a reading of the transcript. Will wait for audio to become available.

Notes:

- (Reasons for market share gain, consolidated): there is a natural pull in the industry for stronger brands like APL Apollo; competitors are suffering from supply chain constraints & raw material shortage; #3 is the continuous efforts to expand our rural distribution network & improve the serviceability for the rural clients. Added 15 new distributors in Q3 in the Tier 2/3 towns. Opened 2 warehouses in the Delhi NCR and Raipur for the rural market; #4 is the continuous commoditization of our sales volume, our product portfolio.

- (Reasons for higher margins, consolidated): Steel prices have gone up by 20-30% in the last few months. It is because there is raw material shortage, steel shortage in the country because in all the end user industries (construction, tube producers, consumer durables, automobile) the demand for steel is going up. So when there is a shortage of steel, our realization goes up because we are able to service our distributors. So the regular sales discounting that goes away in such a phenomenon when we’ve been the dominant player, we are able to service our clients.

- (sustainable EBITDA, consolidated): We are at 75% utilization level, the value addition portfolio is going up for us. We believe that we should be able to generate INR 4,000 to INR 4,500 per tonne kind of numbers, EBITDA numbers over the next few quarters, which were in the range of INR 3,000 to INR 3,500 for the last 2, 3 years.

- (On complete solutions, Tricoat): And in the TriCoat business, we are totally focusing on how do we go into the total solutions like Doorframe Solutions, Electrical Solutions and the Rooftop Solutions. We are working in the – now started working on the small way. I think in the coming years, we are totally converted into the solution provider in this company.

- (On Electrical conduits Market): ILG pipes line started working 3 days ago. I think this electrical solution market is very big in India. We are working to develop this market. Getting BIS certification for our product.

- (Price Comparison with other building materials, consolidated): Pratik, if you look at if you compare steel with stainless steel, it is almost 2, 3x cheaper. If you compare steel with aluminium, again, it is 2, 3x cheaper. So wood also today is 20%, 30% cheaper steel compared to wood. So I think all these product categories, what we are targeting to replace, there is still a lot of margin, even if our color coated tube will be expensive than a normal black tube or galvanized tube.

- (brand pull, consolidated): Did this survey with our fabricators who are using our products with around 30,000-40,000 fabricators. those fabricators are saying that 30% of their end consumer is coming and asking for Apollo Tubes, whether it is from residential side or from engineering construction side or from a large contractor or from a real estate developer side.

- (Guidance on Growth, Tricoat): So Q3, of course, we hit 80% utilization. Our target is that we are able to demonstrate 350,000 tonnes on an annualized basis in year FY '23 with EBITDA spread off much higher like what we have achieved in the 9 months so far

- (Complete solution provider, Tricoat): So within Chaukhat, we are going for Ready Chaukhat Solution and Ready Steel Door solution. And with Designer Pipes, we are going into roofing solution in the coastal markets and East market of India.

10; (ILG technology, Tricoat): we have in line galvanizing technology, which came with the company when we acquired it. But of course, because of the technical lack of technical assistance owing to – because the U.S. technicians couldn’t travel last year. But now through video conferencing, we are – our team in Bangalore has been successfully able to kick start the production. And now after a few weeks of tiding troubles, we should be able to streamline that manufacturing also - (EBITDA, Tricoat): Want to take Tricoat EBITDA to 10,000/ton in steady state by forward integrating (complete solution providing) and launching new high margin products like ILG pipes.

My take: the 20% growth in volumes over next 2 years is definitely a dampener for the valuations and makes the investor question why the management is looking to grow slower than even the base business which itself would grow at 20% PA over next 2 years.

Disc: Invested (for now).

11 Likes

I have been following APL for years. Management has a history of under promising and over delivering

Invested

7 Likes

Absolutely, I remember their capacity went from 2.5 L Tons to 3.5 L Tons in no time without making formal capex announcements.

2 Likes

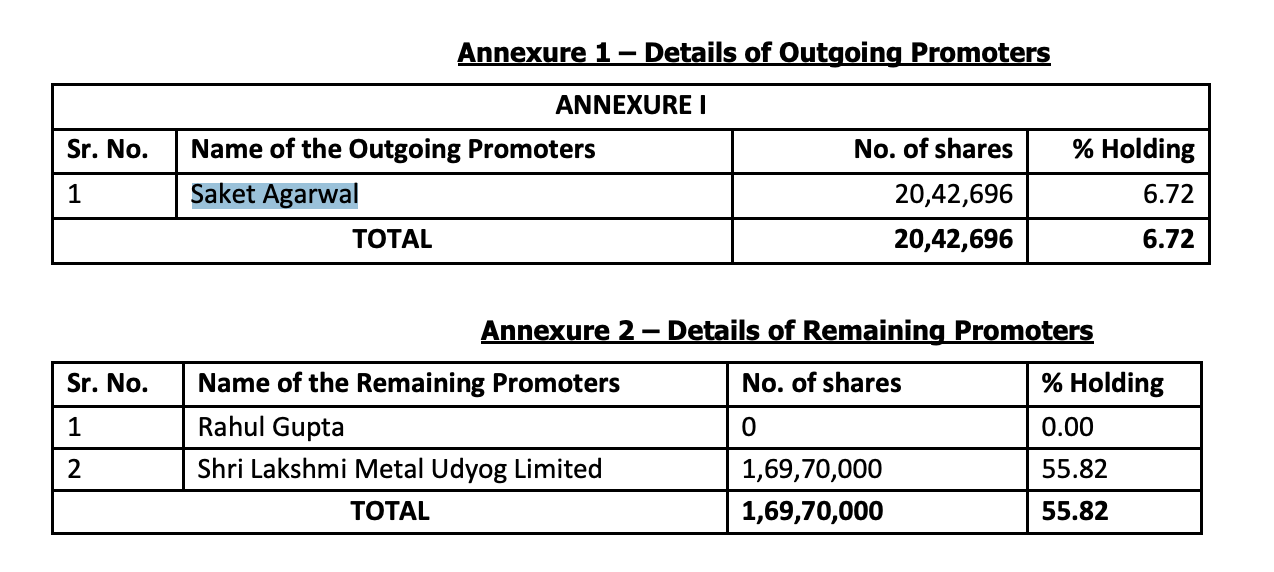

Reclassification of shareholders

Promoters holding went down from 62.56% to 55.82% mainly because of reclassification of Saket Agarwal’s 6.72% shares as public shareholding.

5 Likes

in last three days Saket Agarwal has sold more than 6L share out of the total 20L shares. till this selling doenst stop shares will not find a floor.

2 Likes

Tricoat to be merged with APL Apollo, proposed merger ratio of 1:1

3 Likes

Great news. All the questions related to brand use, royalty etc. are put to rest with this merger.

Disc: Invested in both the companies

For apl Apollo shareholders, yes.

Not sure how it’s good for tricoat shareholders. They get an average business that they didn’t want. My first reaction is that the differentiated product for which I had become tricoat shareholder is going away. Apl Apollo growth imo is too slow, better opportunities exist. I’ll probably sell out asap.

Disc: invested, as of right now looking to sell out asap…

3 Likes

If they hadn’t merged, Tricoat could have followed the same path as Astral Poly with product differentiation, brand and niche. Growing at existing rates, Tricoat was also a undervalued business (even with recent run up in price) as it was available for about 2 times sales.

A good differentiated business is getting merged with a much larger slow growth business. Not a good merger and may lead to erosion of shareholder value with time.

3 Likes