Here management has mentioned that sale of APL tubes shares have been done but when we see in AR-2015-16 as on 31 March 2016 the shares were there in the balance sheet under NON current investment i dont know how to read or interpret management comment on sale of APL tubes share. Missing figure would be in crores …

Please put some thoughts.

Anybody have update about the merger???

Company will move from GSM3 to GSM2 from Monday, 9th October. This would mean trading would happen on all days but it will continue to remain in T2T segment and buyers would need to deposit 100% additional margin. Hopefully next review in Jan 2018 it will move out of GSM.

Has come out of GSM. Enjoy the upmove now

NCLT approves merger of Apollo Pipes Ltd with Amulya Leasing & Finance Ltd

name of the Company is change from ‘Amulya Leasing And Finance Limited’ to ‘Apollo Pipes Limited’ as approved by Registrar of Companies, NCT of Delhi & Haryana vide its certificate dated 20.12.2017.

First post. Sorry if any guideline is violated.

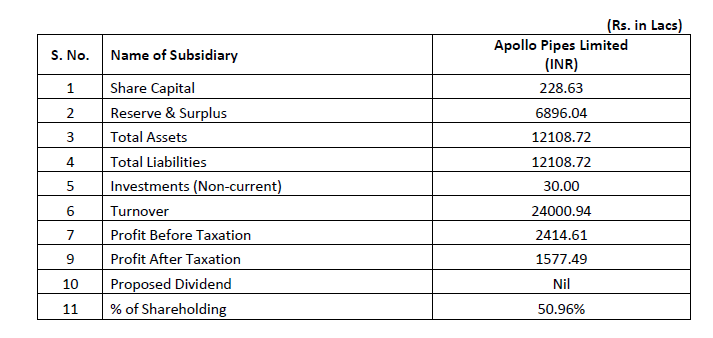

Amulya holds 50.96% in Apollo Pipes. As per latest annual report, turnover is 200 Cr and net profit is 15.77 Cr. At a 20% profit growth and forward PE of 30, Apollo Pipes valuation will be 570 Cr. Amulya with its only business of holding Apollo Pipes should be valued around 290 Cr. With current mcap of 276 Cr, upside is 5%. Too much hype without the comfort on valuation! [Uploading…]

Disc: not holding.

PS: not able to upload annexure 1 to director’s report from annual report 2016-2017

2 Likes

Today param capital and vallabh bhansali bought the shares of the company.

28th Dec : Bulk/Block: Amulya Leasing - buy - Vertex Suppliers (60k shrs @Rs553) & Vallabh/Suraj Bhansali (188k shrs @Rs554), Param Inv (400k shrs @Rs555), Ajay Relan (50k shrs @Rs555), Rohit Dhoot (100k shrs @Rs554) & Fidelity Inv Fund (500k shrs @Rs560); sell - Sameer Gupta (1.8m shrs @Rs557).

Hi Yogesh,

I have read a lot on Amulya Leasing and the big guys getting into it. Can you please share your email Id or contact coordinates so we can discuss. It seems like a huge play…

Regards,

Nitin

Shareholding of promoters seems to have increased…

Anyone here tracking this company? Seems a lot of interest in this recently by big players…

@zygo23554, @Yogesh_s ---- do you still track this , would love to hear your thoughts on this…

1 Like

I largely agree with assessment by @coolgaurav141.

Here is the Annex 1 to director’s report in AR 2017 of Amulya Leasing

Source: http://www.bseindia.com/bseplus/AnnualReport/531761/5317610317.pdf

Company is earning a margin of 7% on sales which is in line with Astral. ROE is 23% which is good. Astral and Supreme are selling at 4-5 times sales. If Apollo Pipes were to sell at 3 times sales, it will be valued at 750 Cr. Amulya Leasing owns 51% so its share will be 375 Cr. This is again an optimistic valuation. Astral and Supreme are much larger companies with proven track record. Amulya cannot be valued like an Astral or Supreme (both of which appear to be overvalued to me). On a more reasonable 2 times sales, Apollo Pipes can be valued at 500 Cr and Amulya’s share will be worth 51% of that or 255 Cr. So we are looking at a valuation range of 255 Cr to 375 Cr. Its current market cap is 333 Cr.

What investors are paying for is future growth and ability of management to scale this business. Astral and Supreme are overvalued because investors believe in the growth potential of the industry. With this, you are able to get a small company with 333 Cr market cap which is planning to take sales 4x in 5 years. Management could have done this even without merger but as with APL Apollo, management want to adopt best practices and target market cap. So overall story looks good to me and going by valuation APL Apollo, I think this will do well too.

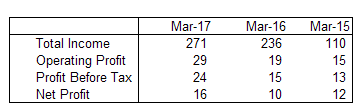

Management has already proven their ability to scale this business. Sales, operating profit and PBT have already doubled in last 2 years.

Source: Capitaline

8 Likes

Hello Everyone,

I am looking at this company after the interests shown by the institutional investors. I have some very basic queries regarding the merger and name change. My apologies if I they are already mentioned earlier in the thread.

-

Post the merger, will there be only one company i.e. Apollo Pipes? Or there will be a separate holding company?

-

After the stake sale by the promoters, what is their current holding in the company?

Thanks very much in advance

-

After merger total shares would be 1.1 crore and promoters hold good 79 lack shares so one can calculate how much holding he would be left with after recent deals.

-

So if we go by merger plan than the Market cap of the company is more than 750 crore from todays price.

Please correct me if i am wrong.

promoters sold 17.6 L shares recently to big investors, roughly they must be having 49 percent of shares

I am answering some of the queries asked on this company.

- Apollo tubes is in to PVC, uPVC and CPVC pipes and currently has 53000Mt capacity. The company sold close to 28500MT in FY17

- the capacity s likely to increase to more than 80000Mt over next one year and given the focus on affordable housing and irrigation, we can expect 20-25% volume growth for this company over the next 3 years.

- Key Competitors include Astral Poly, Finolex and Supreme. All these companies expect double digit growth in volumes for the next 2-3 years.

- Current share capital is 4.99cr and post merger it will increase to 11.5cr. So on expanded equity, market cap is close to Rs800cr.

- During FY17, the company reported Rs268cr sales and Rs17cr PAT. By FY20, I expect Sales of close to Rs580cr and PAT of Rs50cr (assuming 30% revenue growth)

- peers in this segment like Astral, Supreme and Finolex are trading close to 30-40x or ward PE. (Astral is 65x trailing PE). Even if you assume 25x FY20 PE for this company, target market cap comes to Rs1250cr which is still 55% higher than current diluted mkt cap.

- Given the 10 yr growth profile of APL apollo (promoter grp company), i believe mgmt is very sanguine and savvy when it comes to growth.

- Promoters are likely to issue themselves preferential warrants in future with the money they raised through share sale last week.

key things o watchout

- Volume growth in new and existing markets and using the existing distribution network of APL apollo to grow in new geographies for pipes.

- Volatility in raw materials

- Competition

Please note that the above analysis is based on the feedback received from an existing investor who was part of the bulk deal that happened in the last week of December

6 Likes

Apollo Pipes is under top 5 Pipe Brands in India Source (https://www.mostinside.com/best-brands-cpvc-pipes/)

Apollo Pipes

Apollo CPVC Pipes in India

Apollo Pipes Limited started producing a wide range of U-PVC high end pipes in the year 2000 and has its technologically advanced plants set up in Uttar Pradesh. Along with its vast expansion in production and distribution networks, the company has become a renowned name in India due to its core objective of offering committed quality products and services to its customers.

The CPVC pipes and fittings are the latest addition in the company’s Indian portfolio and are produced keeping in mind the quality required in residential and commercial projects. Highly suitable for distribution of potable water, these pipes fro, Apollo are said to have a life of over 50 years after installation.

As they have manufetiring plant in UP so they will have better access to northan India market and I feel with affordable housing push by govt and housing for all target by 2022, should get benifit for apollo, as UP might be needing more homes, as UP alone has 16% of India’s total population and I feel Apollo is better placed to supply to UP & other northan parts of India than Astral and ashirvaad…

Also APL Apollo managemen also has proven track record, so I feel this is nice bet to have and when you see marqee investors like vallabh bhansali has invested @ around 577 price (bought promoter’s stake) that also give good confidence… I missed Astral in its growing years, maybe this can at least somewhat repeat Astral story, as I feel India Still need lots of piping both for new houses being built and also repalcement of old GI pipe in old houses…Looking for 3 plus years of investment horizon on this…let see how stiry get unfold from here…

7 Likes

yesterday again 17L shares of promoters bought buy reputed investors including 2.75L by kotak mahindra mutual fund , is this slowly moving towards MOAT position ?

I am already sold on the potential of plastic piping segment in India. One cannot find too many industry segments where 10%+ volume growth at above average (20%+) ROCE is doable over the next 8-10 years. Every single pipe maker out there is expanding, one would expect Apollo Pipes to do the same too. This will be a growing market where there is enough for everyone to grow without having to resort to pricing gimmicks

At a cursory glance none of the numbers here look out of the normal range - One would expect a player of the scale of Apollo Pipes to show a realization in the range of 85000 - 95000 per MT. At a sales of 268 Cr, they have 100 distributors while Finolex has sales of approx 2200 Cr on a distributor base of approx 800. As someone who’s participated in the APL Apollo story I already have a good amount of comfort with the promoter group.

On the face of it this story should do well from here, one needs to do a thorough check on what price one is willing to pay for the current scale of the business. I most likely won’t look at this immediately since I am already in with a substantial position in Finolex Industries - reasons I’ve articulated in that thread. I will be tracking this one though

4 Likes

I agree that Pipe industry is there to grow in double digit for a decade or so, as lots of houses will build in next decade also lots of replacement demand will come for GI pipe… I feel many players can grow together in such a large country and I find this is a good opportunity to get a pipe company in less than 1000 cr MCAP…