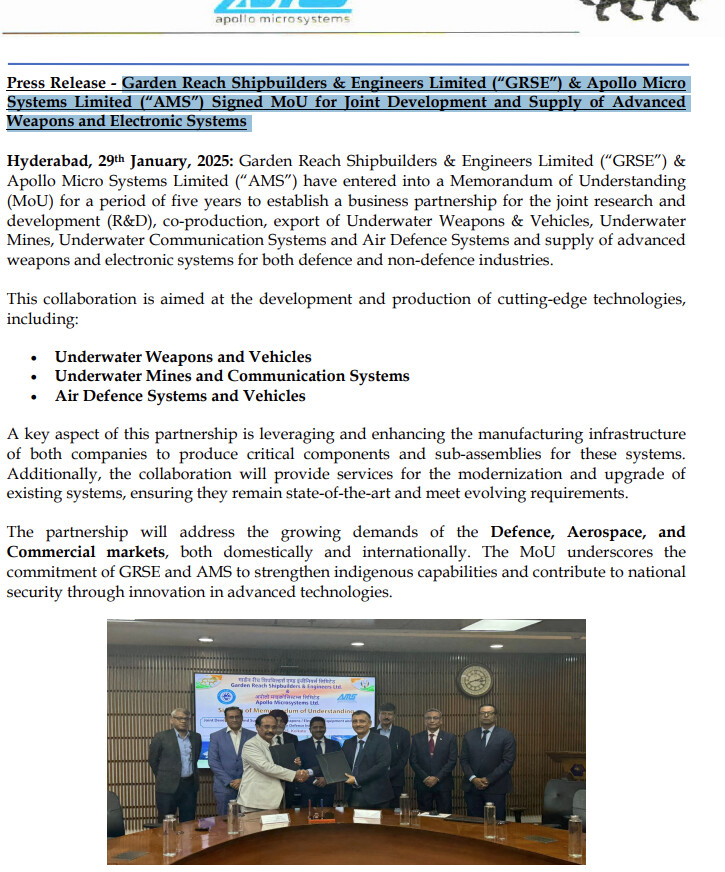

Overview

Apollo Micro Systems Limited (AMS), based in Hyderabad, India, is a pioneering design and development organization specializing in high-performance electronic systems and solutions for defense, aerospace, and other industrial sectors. Established in 1997, AMS has grown into a significant player in designing and manufacturing cutting-edge technologies tailored for critical applications in extreme environments.

Core Expertise

AMS focuses on end-to-end solutions, including design, development, assembly, and testing. Their core strengths lie in:

- Build-to-Specifications (BTS): Developing custom designs based on client specifications, involving hardware and software development, prototyping, and qualification testing to meet targeted environmental and functional requirements.

- Build-to-Print (BTP): Manufacturing and assembling systems using customer-provided designs, ensuring adherence to stringent standards and quality expectations.

- R&D Capabilities: Certified by CEMILAC for developing airworthiness systems, AMS’s in-house R&D team works across multiple verticals, including aerospace, avionics, space, naval, and automotive sectors.

- Collaborative Partnerships: Recognized as a collaborative R&D partner by Bharat Electronics Limited (BEL), AMS also provides lifecycle support for its solutions.

Solutions and Services

AMS operates in diverse domains, offering innovative solutions and services:

- Defense: Development of rugged electronics meeting military standards for ground, air, and naval applications, including embedded hardware and software for extreme conditions.

- Aerospace and Avionics: Advanced on-board systems and ground support equipment designed for aerospace missions.

- Transportation and Homeland Security: Embedded solutions for security, monitoring, and operational efficiency.

- Electronic Manufacturing Services (EMS): Comprehensive services for hardware design, CAD, and IT/software integration, catering to various industries.

Infrastructure

AMS boasts state-of-the-art facilities and advanced infrastructure to support its extensive R&D and production activities. This includes a robust supply chain management system, ensuring seamless procurement and manufacturing processes.

Achievements and Certifications

AMS’s certifications and consistent quality benchmarks highlight its commitment to excellence. It operates under stringent quality assurance processes, ensuring compliance with both customer requirements and global standards.

Global Reach and Vision

Apollo Micro Systems aims to position itself as a global leader in its domain by continuously innovating and maintaining its focus on customer satisfaction and mission-critical solutions.

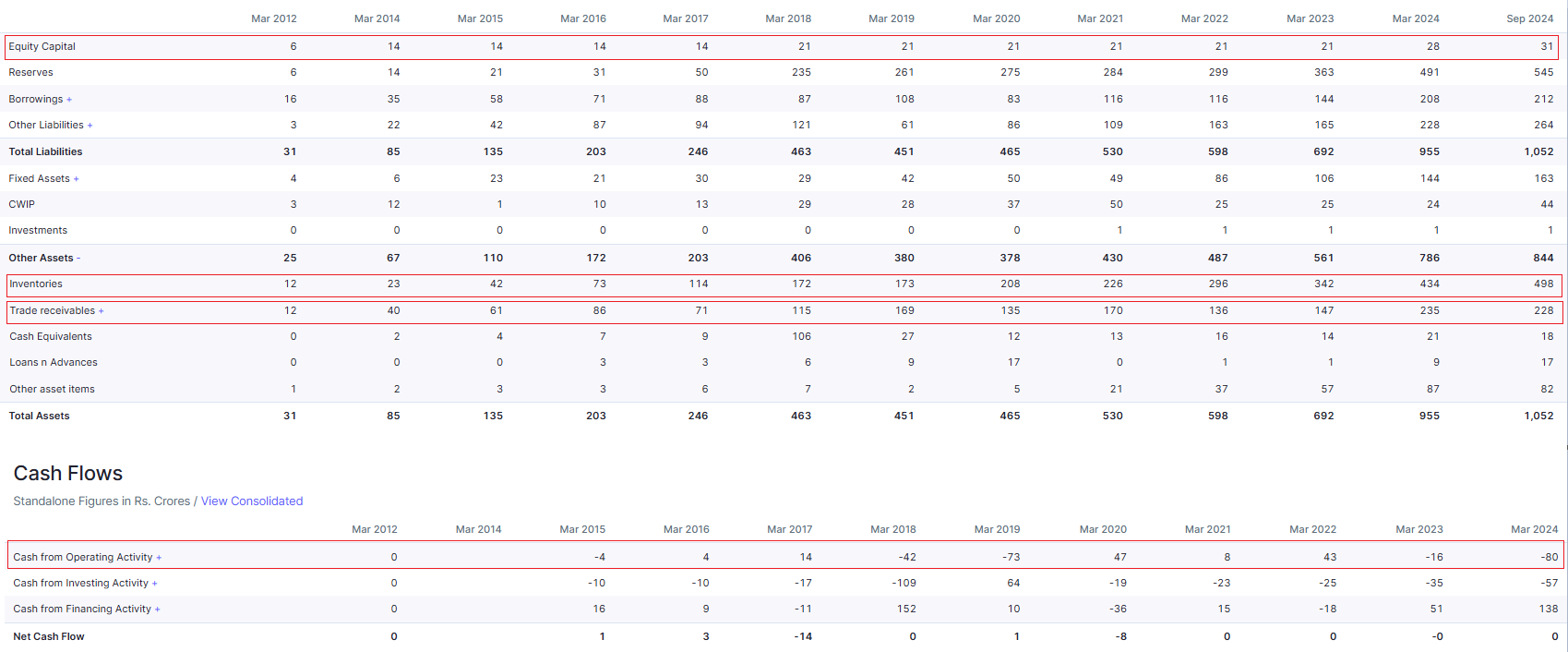

Financial Performance Table (FY21-FY24)

Profit and Loss

Summary

Apollo Micro Systems has shown a steady focus on expanding its operations, particularly in defense and aerospace sectors. In FY24, the company reported an 8.52% Profit After Tax (PAT) margin and a 23.27% EBITDA margin, highlighting its operational efficiency and profitability. The company’s ongoing investment in research, development, and manufacturing capabilities continues to strengthen its position in the market

Key Observations:

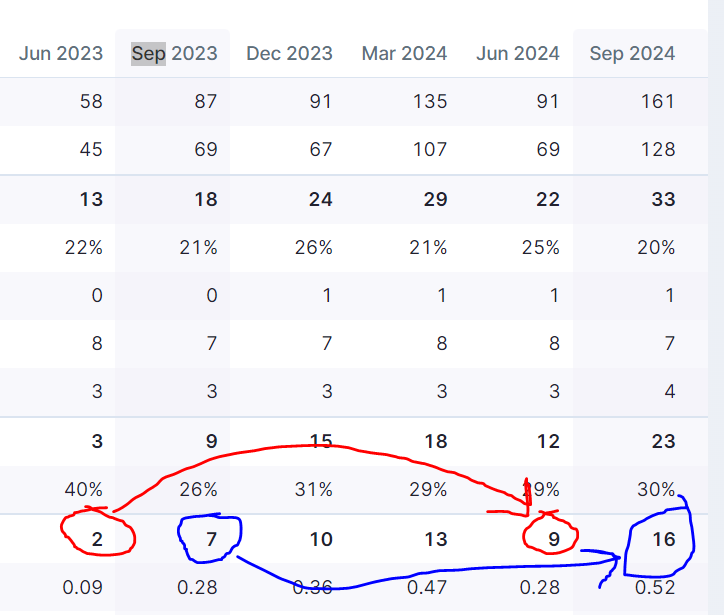

- Revenue saw a steady year-on-year growth from ₹203.00 crores in FY21 to ₹373.00 crores in FY24.

- Net profit improved proportionately, highlighting operational efficiencies, despite slight sequential reduction from Q4 FY24 due to project cycle

Apollo Micro Systems reported an operating revenue of ₹478.69 crore on a trailing 12-month basis, showcasing an impressive annual revenue growth of 25%. The company’s pre-tax margin stands at a robust 12%, reflecting healthy profitability, while its return on equity (ROE) is 6%, indicating moderate efficiency with room for improvement. With a low debt-to-equity ratio of 2%, the company maintains a strong and stable balance sheet. On the technical front, the stock is currently trading below its key moving averages, and a sustained breakout above these levels is essential for any significant upward momentum.

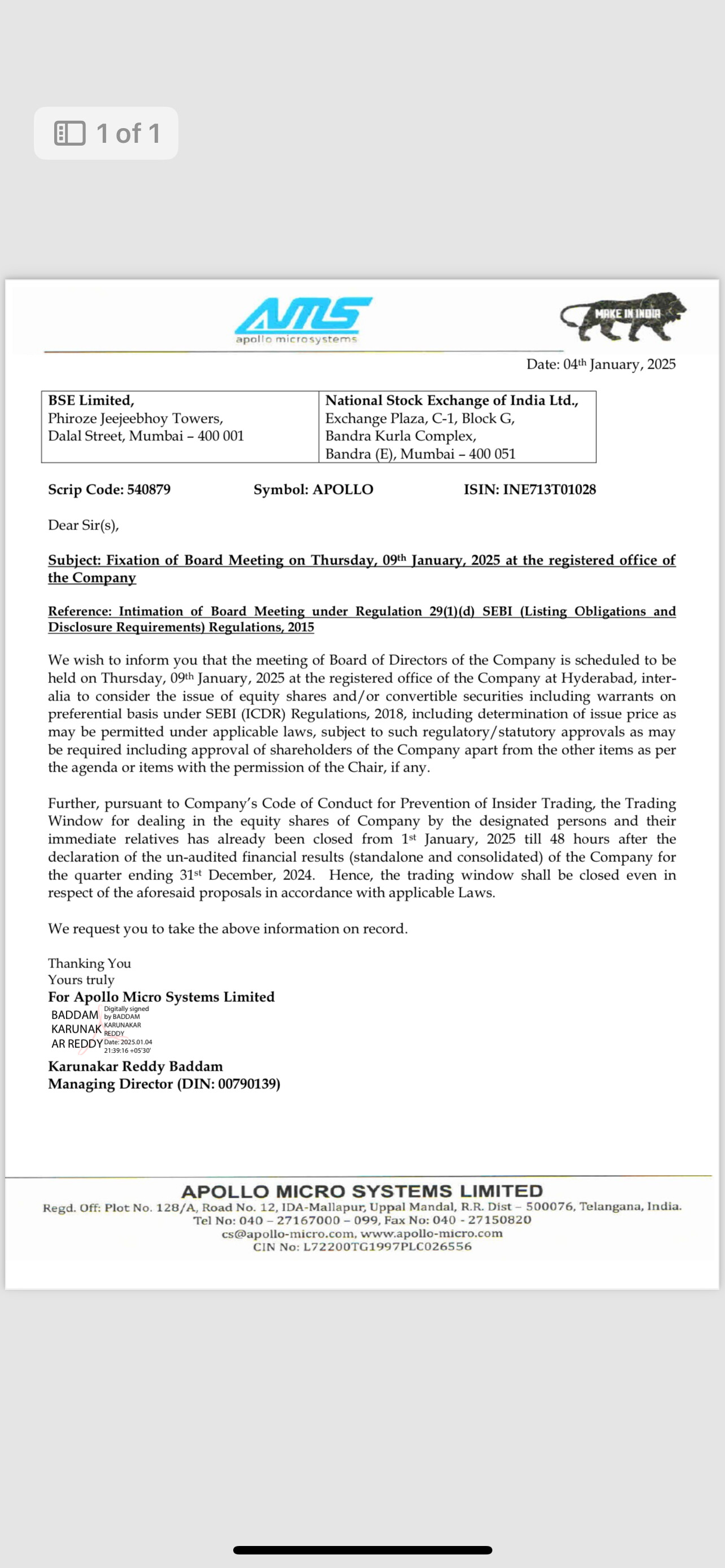

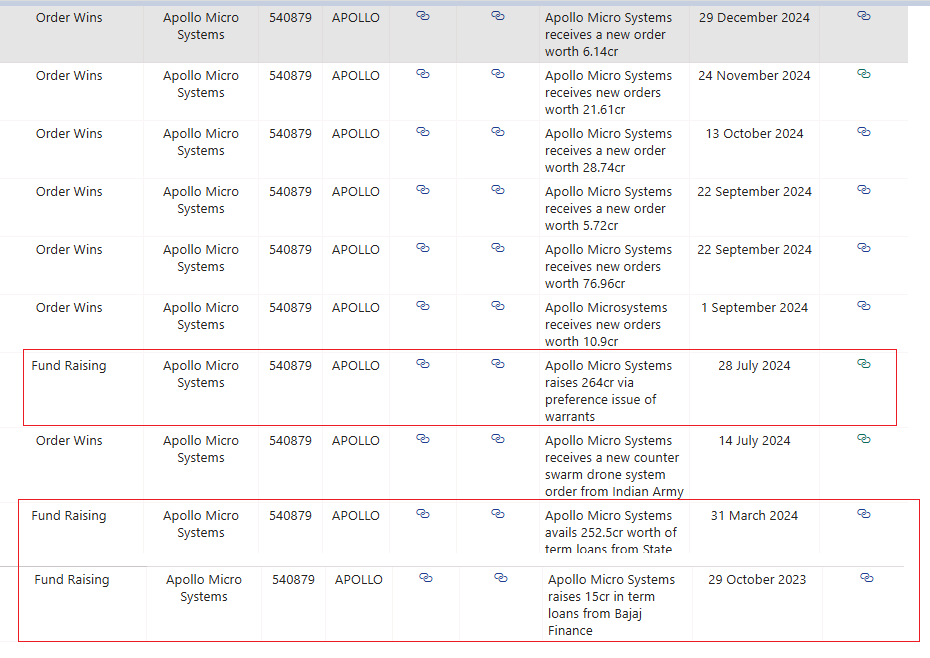

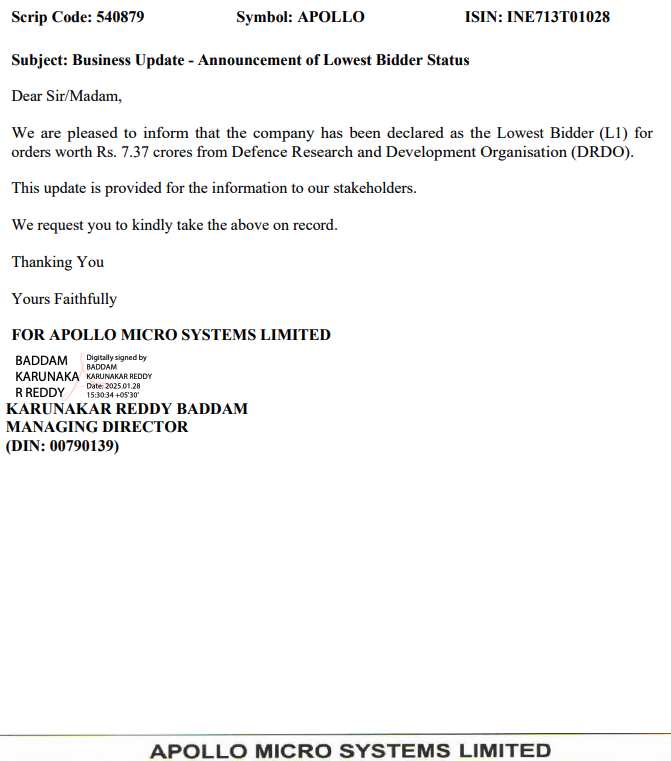

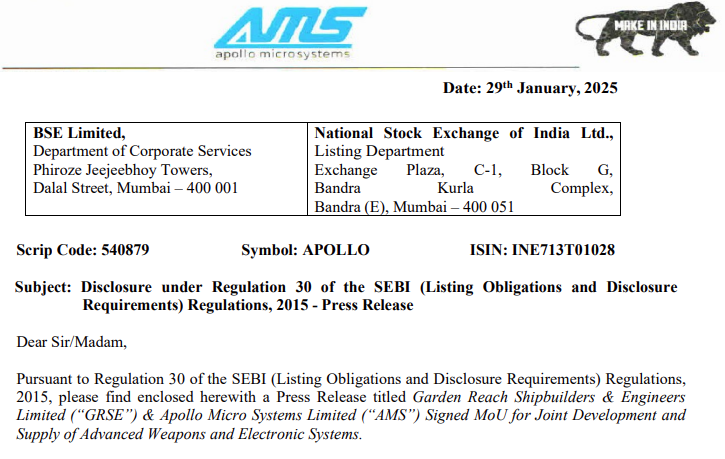

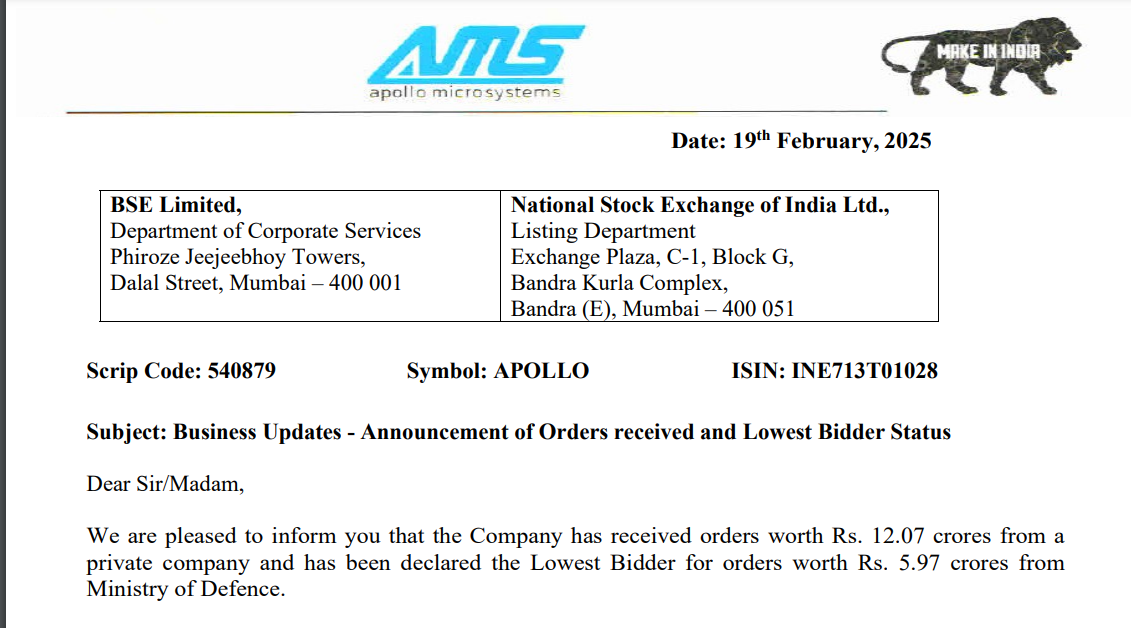

Recent Significant Order Wins

On 12 July 2024, Apollo Micro Systems announced it was shortlisted for a Make II project by the Indian Army.

This project involves the procurement of a vehicle mounted counter swarm drone system (VMCSDS) (Version I) under the Make II category of DAP-2020. It is the company’s first Make II project and is considered very prestigious.

The systems developed for this project are state-of-the-art and highly futuristic. There is no cost obligation involved for the company in this project.

The Directorate General of AAD, IHQ of MOD (Army), awarded the contract. The nature of the contract is categorized under Make II of DAP-2020, and the order is to be executed within 85 weeks for single-stage composite trials and staff evaluation.

This order boosts the company’s share price by increasing investor confidence. It highlights the company’s capability and potential for future growth in defense technology.

Apart from the big order, the company was also under focused as it announced that it has converted some share warrants into shares.

What Next?

Apollo Micro Systems is set for continued growth following its strong performance in FY24. The company’s revenue and profit have seen significant increases, driven by robust order execution and increased operational scale. This positive momentum is expected to carry forward into FY25.

Its order book is strong, with many contracts moving from development to production. This shift provides greater visibility for future revenue growth.

The company continues to focus on developing innovative defense solutions with significant export potential. Participation in Make-II defense projects and potential collaborations for larger platforms will further support this growth.

The company is expanding its manufacturing capabilities with the development of new facilities, including the Integrated Plant for Ingenious Defense Systems (IPiDS) in Hyderabad. This plant will enhance its capabilities in missile and unmanned systems development. The additional facilities under development will significantly boost production capacity to meet growing demand.

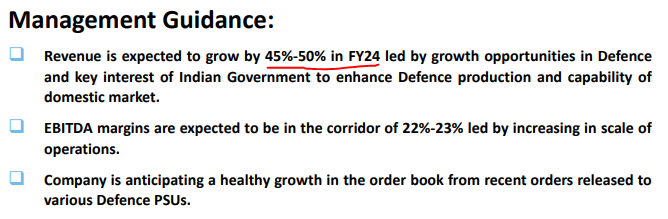

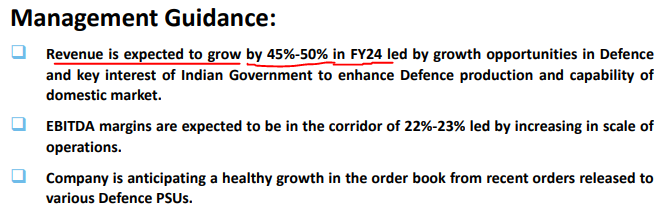

Looking ahead, the company expects revenue to grow by 25% in FY25, driven by new defense contracts and increased production capacity. In FY25 EBITDA margins are anticipated to be between 22% and 24%.

From 2023-24 AR

The order book is expected to grow with recent defense orders, ensuring a steady stream of future revenue. Additionally, its subsidiary, Apollo Defence Industries, is exploring potential acquisitions to further strengthen its market position.

Risks

The financial risk profile

of the company has remained healthy with healthy capital structure, low gearing, and moderate debt protection metrics. The net worth of the company stood at Rs.383.70 Cr. and Rs.319.14 Cr. as on March 31, 2023 and respectively. The net worth is improved due to addition of money received against share warrants of Rs.45.96 Cr. and accretion of profits to the reserves. The company follows a conservative financial policy reflected in its peak gearing of 0.38 times as of March 31, 2021. The gearing of the company stood at 0.37 times as on March 31, 2023 against 0.36 times as on March 31, 2022 and 0.38 times as on March 31, 2021. Tol/ TNW stood at 0.80 times as on March 31, 2023 as compared to 0.87 times as on March 31, 2022. The debt protection metrics were comfortable with the interest coverage ratio and debt service coverage ratio stood at 2.76 times and 1.36 times as on March 31, 2023 respectively as compared to 2.70 times and 1.25 times as on March 31, 2022 respectively. The debt to EBITDA of the company stood at 2.29 times as on March 31, 2023 as against 2.49 times as on March 31, 2022. It is expected the financial risk profile to remain healthy over the medium term on account of the company’s healthy capital structure and stable operations.

High Entry barriers and moderate order book position

AMSL operates in a niche segment of a high entry barrier Defence and Aerospace industry. The company is ‘Centre for Military Airworthiness and Certification (CEMIAC)’ certified, whereby it is an approved design house for design and development of software and equipment for military aircraft application. This certification is based on technical experience and past record of such authorized design houses. AMSL deals with reputed clientele like Bharat Dynamics Limited, Bharat Electronics Limited, Defence Research and Development Organisation (DRDO) among others. As of Feb 24, AMSL has an unexecuted order book position of Rs. 344.88 Cr. With high entry barrier coupled with long term nature of contracts of the order book provides revenue visibility over the medium term. Further, AMSLs growth prospects remain healthy, supported by the Indian Government’s focus towards indigenization in the defence sector amid the Make in India thrust

Working capital intensive nature of operations marked by high GCA Days

AMSL’s working capital operations are intensive marked by its high Gross Current Asset (GCA) days of 657 days as on March 31, 2023 and 701days as of March 31, 2022 on account of stretched receivables and sizeable inventory. AMSL primarily caters to domestic defence establishments that usually have long production cycles due to scrutiny and inspection involved in every stage of production, starting from raw material procurement to delivery of the systems. And also it manufactures various kinds of customized products which leads to a long turnaround time that varies across the segments, and furthermore the R&D cycle of defence products and solutions is long, which could stretch over several years. The inventory days stood at 535 days as on March 31, 2023 and 547 days as on March 31, 2022. The higher inventory levels as on March 31, 2023 are attributable to additional stocking of critical raw materials. Moreover, the systems need to be tested by its customers after delivery, after which the payments are released. This results in high debtor days at 180 days as on March 31, 2023 as compared to 205 days as on March 31, 2022. The company meets a part of its working-capital requirements by stretching payments to creditors; however, the same are backed by LCs

Liquidity Position: Adequate AMSL’s liquidity is adequate with adequate NCAs to its repayment obligations. ASPL generated cash accruals of Rs.29.43 Cr. during FY2023, while its maturing debt obligations Rs.0.54 Cr. during the same period

Disclosure: Invested