Apm industries is in synthetic blended yarn sector located in Bhiwandi industrial area with a spindle capacity nearly of 60000 It has more than 5% div yield. P/E is less than 7 and P/BV 0.6 Cash flow yield is about 30%. EPS and sales growth are consistent. Net profit margin is growing and consistent. Promoter holding is 61% and increased holding Dividend is growing too. ROE is at an adequate position and consistent around 12-13%. Debt to equity is almost 0.

Having said that, why is such a value opportunity not utilized yet in this Bull Run or is this value trap? Am I missing something?

The financial numbers speak that APM Industries Limited is a descent business, which has been growing at a moderate pace of 8-10% per year while maintaining 10-12% operating margins. Net profit margins have also improved over last 4-5 years to 6-8%.

APM Industries is paying its due tax as the rate of tax paid is about 33-35%, which is a good sign.

Profits are being collected in cash and the operating efficiency levels are improving year on year whether we measure it by asset turnover, inventory turnover or receivables days. APM Industries has been generating good cash from operations and has used repay debt now it is debt free cash flow for the last three yrs at 37 cr 22 cr and 32 cr

APM Industries has been sharing its earnings with shareholders as it has started paying dividend since FY2011, the year since its profitability has shown improvements. Dividends have increased over the years with growth of the company.

Its market capitalization is INR 112 P/E ratio is currently 6 and Evebita of 4 now Welspun syntex is quoting at At 12 PE 8 Evebita and 3 times book value with a debt of 180 cr

Now seniors please throw some light on valuations and promoter history and corporate governance

Discl. I have invested a tracking qty

Indirachitra your earlier thread of associated alcholol has hit new high of 160 now iam studying this with curiosity have seen a news some where will copy paste it once I get it anyhow associated was realy good any further info

Though I agree that APM has consistent numbers and good profitability, the concern i see is that there is hardly any growth. If someone stops growing then he will automatically have cash flows. If you read the last few annual reports there is zero expansion in capacity.

Thank u ayush yes I did notice there was no capacity addition that why I did not categorise it under untested hidden gem I was comparing the huge valuvation anomaly between WELSPUN syntex and Apm based on the present numbers only. With tail winds towards textile sector I thought this should get some sort rerating and basically I considerd it because it is only textile stock I can see without debt .

For capacity addition and growth iam considering Sutlej textiles since iam studying the annual report of 2015 which I received only yesterday I did not mention that.

As regards associated alcholols Mr Prakash please go the thread I have given my views thanks

Ayush do you please mind to have a look at Cosmo films earlier I was not considering it because of the debt level with opm on increase can it become a cyclical uptrend stock I do like Mr Jaipuria a highly educated and decent man and one more I noticed is Anil Kumar Goel is holding a substantial portion

the company hasnt put capex or shown significant volume growth in past 5 years.

the OPM of the company keep fluctuating, since there is not much pricing power enjoyed by the company. Main RM - Polyester fibre , whose prices keep fluctuating

the cash flows earned by the company in past 2 years have been used for investing in non current investments like mutual funds,bonds, equity instruments etc. This shows that there is not much demand for the company’s product and no scope to expand.

however the company is trading at price of 140 cr vs a share holder value of 190 cr.( reserves+ equity capital). but this difference is too less for there to be an increase in market value, and such value normally does not get unlocked in my opinion.

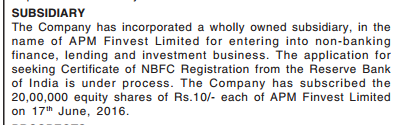

the company has obtained a NBFC license from the RBI for its subsidiary APM Finvest Limited.

i believe since the company is not able to expand it is using its cashflows to invest in securities, and entering a new line of business. this is a huge negative for me , as most of the textile players are putting up capacities to cater to increasing demand . Plus with no experience in financial services , it is difficult to predict how things will turn out for the company.

NOC/Observation letter received from BSE/SEBI for demerger of NBFC (APM FInvest). http://apmindustries.co.in/wp-content/uploads/2018/06/BSE-observation-letter.pdf

Next is approval from NCLT. Subsequently NBFC will be listed. Investors will get free shares of NBFC in ratio of 1:1.

Textile division is also doing well. huge land bank of 30 Acres or so. Company did revaluation of land in 2009 and stated it as 73 Cr in Balance sheet and hence RoNW reduces a bit as most company value land at cost price in their BS. Current market price should be around 110Cr.

Current Investments/Cash/Cash eq of 77 cr in books (~36 Rs/Share). MCAP just 101 Cr .

NBFC expected to head start with Book value of Rs 40 or so and will offer price of Rs 80 at PBV of 2. Textile division (APM ind) will also have a value of Rs 60. So the sum of parts (SOTP) valuation expected at 140 Rs.

(Disclosure: Invested & hence interested party)