I had attended the concall of APL. Some of the points I noted during the concall:

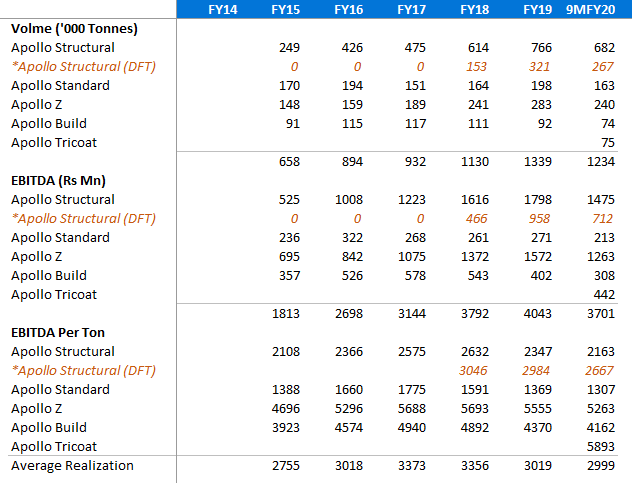

• Consolidated volume of 4.80 lakh during the quarter. Excluding Tricoat, growth is 38%. Restocking at dealer level and overall improvement in markets. On path of 20% volume growth during the year.

• EBITDA/tonne stood at 3,440. Planning to increase market premium and better product mix. Should report further volume growth.

• EBITDA in Q3 came at 165 crore.

• PAT performance is also better that we have moved to 25% tax level.

• On balance sheet front, reduced total debt by 100 crore during the quarter. On consolidated basis, D:E improved to 0.6 times as compared to 0.9 times.

• Improving market sentiment and increasing liquidity helped the company.

• Cash flow to improve driven by pick up in utilization. Company is also actively targeting 80 – 85% capacity utilization. Targeting steady improvement in product mix. Focusing on larger diameter hollow segment. Sector still has large demand on these segment. Company appointed PK Singh as an executive director.

• During the quarter, promoter completed 75 crore infusion in the com

• Demand environment seen healthy volume growth – Geography and industry wise? Sales volume break up 65% sold in building category and 35% is from infrastructure and industrial applications. Last 3 months, we have seen demand from housing, commercial and infrastructure. Focused on value added products which has grown higher. Taken market share away from other smaller players. Aspect of government growth which added to our quarter’s sales? Very limited sales from government. All trade channel sales.

• Distributors added? 800 distributors added. Do add new customers and consolidated them. Added 20 – 30 distributors in past 4 – 5 months.

• Ex tricoat – EBITDA/tonne is 3150. Tricoat – 6100 per tonne on consolidated basis.

• Did 48,000 MT in the quarter in Tricoat – total capacity is 250,000 MT.

• Did commercial paper issuance – what was yield to maturity? Issued at 6.60% per annum at mature at March end.

• EBITDA per tonne ex Tricoat is 3150 per tonne. How much of that has come from steel price increase? Steel prices as on 1 October compared to December 31 – no changes in prices. No inventory gain or loss for the quarter.

• Other expenses increased quite a bit, what is the issue? Passing on benefits through distribution rebates? Other expenses increased due to change in trade policy. We have changed to FOR basis, last quarter impact is there. Some branding increase is there. Compare with yoy – last year it was 1 crore, this quarter is 17 crore, last quarter it was 10 crore. Freight policy change – Now selling at gross level plus freight charges.

• Impact of rain disruption and lockdown on sales? Volume sales ramp up started from November onwards. Going forward we may have better volume growth in Q4 compared to Q3. Endeavor is to achieve better.

• Inventory valuation at quarter? Quarter ended December it was 1.5 lakh tonne. Stock got valued at base prices.

• Current prices are higher compared to December 31 rates.

• Product mix – GP, GI and Apollo Tricoat? October was like Q2. Only had 2 months in the quarter where demand had increased. 1.5 months since scenario has improved.

• Reduction in interest cost during the second half of the year. Not seeing that in Q3? What kind of debt levels are we seeing at March end. Debt levels – they have come off. What we look at March, 2020. Debt/EBITDA and interest coverage main ratios definitely improving. Both the ratios would improve further in March, 2020.

• There has been shifting of plant from Gazhiabad – consolidated basis have 10 plants running compared to 11 plants.

• Demand trend for Apollo Tricoat? Started in March, 2019. Working on seven portfolio. Being produced for the first time in India. Ramp up of these products is better than we thought. Chaukat, plank etc – 4 products have ramped up quite well. Channel partners and market have liked the product. Already running at 70 – 80% capacity utilization. Should launch 3 products. Next 2 year, take utilization levels upto 80 - 90% capacity utilization. Potential for the business? Dealer and customer feedback? One product Chaukhat producing 4000 MT per month. Replacement for wooden chaukat. Better price and termite free. In a small 2 BHK flat, there are atleast 7 – 8 doors, it can be a huge market. Only selling in North India currently, would expand further. Signature – designer pipes used in furniture currently.

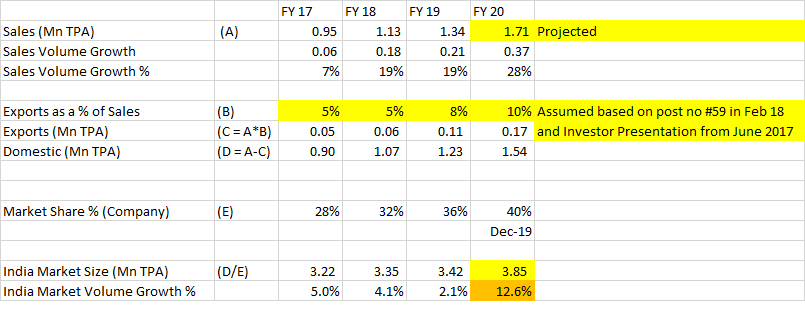

• 40% market share of APL, what is that? Market is structural steel market. India is 4 million tonne, we are doing 1.6 – 1.7 million tonne, so 40% market share. Run rate for growth for the company? Double digit volume growth and superior EBITDA/tonne is possible.

• Higher share of larger dia pipe contributed for growth. Yoy growth. Dia pipe is above 300 mm. It contributed 7 – 8% of our sales compared to 3 – 4% overall for the industry. Need to grow market – have to make architecuture, builders aware about it. EBITDA/tonne higher for it. EBITDA spreads are 2 times higher than what we get for blended basis.

• You have significant capacity yet to be utilized – capex going forward? Capex spend at 20 – 25% of EBITDA. Did 4.8 lakh tonne. Annualized run rate is 18 – 19 lakh tonne. Still 15 – 20% away from optimal utilization. If there is actual pull from the market, we can go ahead with capex.

• Capex front – not much capex. Debt levels will come down? FY20 – how it is panning out, despite capex and acquisition, we have been able to reduce debt. In simple words, capex intensity is low, debt levels should come down. Volume growth of double digit volume growth and superior EBITDA growth for FY21.

• Capex – Guided for 200 crore this year. What stage will we look at further expansion? Capex front – spent 80% of the total outlay, Q4 will be minimal. Capex guidance for FY21 and FY22? Still 12 – 15 months away from optimal capacity utilization. If there is pull in the market, we may have to think of capex. We have land parcel in Raipur which we have already bought. Capex for machines. Some capex for higher diameter tubes.

• January volumes? Tapered down from November, December levels? January ground level demand is still robut. It should continue for next 2 quarters.

• Advertisement and brand spending? Stick to 40 – 50 crore annual expenses in FY20. Getting good response to it. Spend similar amount or lower amount next year.

• Higher margin in Tricoat despite similar realization? Realization are higher in Tricoat leading to higher EBITDA. Apollo Zee and other products sold in entire India while in Tricoat primarily sold in North market.

• Decline in Apollo Standard volume? Share in product mix has declined during the quarter.

• Last year – scrap volume not shared? Not part of manufactured volume. That comes in other operating income. Its around 5% of manufactured volume.

• Current cash and bank balance? We have given debt figures in the presentation. Debt repayment is to the tune of 100 crore. Cash balance is high as of now? Cash is fully invested in working capital and capex. Not much difference between gross and net debt.

• Q4 paying 25% of PBT.

• DFT side – how are seeing panning out of DFT – where do we see it in next few years? Ramped up quite well, sharpness in edges. Customization possible. Started to charge premium for it. Will attract more premium going forward

• Next year guidance is superior EBITDA growth.

• Inventory loss or gain there is none? HRC prices, average price had been significantly lower during the quarter? Have we built higher inventory during the quarter? No inventory gain or loss in the quarter. Saw decline in 1500 per tonne in inventory while November and December were increase of 500 and 1000 per tonne.

• Price increase in January – passed onto consumer may be with time lag.

• Last year we had acquired couple of assets, like to like volume growth – 32% during Q3.

• Rise in steel prices, scrap prices remain low? Scrap prices move only in accordance with secondary steel prices. Recently, secondary steel prices have also moved up – scrap prices have moved up. Scrap prices change every day. It’s a very wide range of variance. Unorganized players loosing market share? Across the industry, working in our industry for sure.

• Brand costs would not be higher than this year next year. Know which category have performed well for us and want to focus on that.

• UP – saw great visibility for about company. Great visibility across roads and interior? It’s a nationwide campaign. We have done it everywhere. In certain areas, we have done more as per our strategy.

• Average inventory levels at distributor level? Normally, our dealers stock 15 – 20 days of its monthly sales. Any prices movement, they have just 5 – 7 days of inventory. If it reduced below that, it would cause problem to him. In price increase, they would be short of working capital. If price stabilizes, they would have to still keep atleast 15 days of inventory.

• Improvement in working capital, what is the reason for that? Collection has improved over the past one year. Channel financing is playing a role in that. Plus we are the largest player in the industry with 40% market share. Have been able to command better payment terms with our dealers. Better inventory and collection days led to improvement in working capital.

• Government receivables? Better payment terms? Don’t have any exposure directly to government agencies. Its normally in line with our receivable days with government contractors.

• Any plans to increase B2C share? Offering are increasing to more building product category? Don’t want to do it directly. But talking to distributors where they can start APL Apollo experience centers. First go through distributors.

• Globally, lot of steel players get into forward integration into steel pipe manufacturing? See similar trend in India? Globally, also pipe players are pure play steel tube players and not steel players. For a steel producer, who are doing 15,000 EBITDA/tonne kind of trend, they would like to be into higher value add products. Tata Steel, JSW and Bhushan are already there in steel tube. Haven’t heard of any other large player in the market. In fact, competition might help in expanding market. Structural steel is 4% of the overall steel market while globally its 10% so huge room for us.

• Improvement in EBITDA/tonne, what is contribution from DFT, logistic cost benefits etc – how much impact? Value added products have contributed to growth have higher margins.

• DFT plant at North and South. Logistic saving coming from Shankara? Neglegible. Doing 10,000 MT per month from Shankara – total capacity 200,000 MTPA.

• Large diameter is fastest growing segment in structural tubing industry. Globally it is 25 – 30% of structural tubing industry while it is at 5 % or even less than 5%. Growth opportunity there.

• Other expenses – what could be quarter run rate – 150 crore quarter run rate? Its linked to volumes. You will see that EBITDA growth is superior than volume growth.

• Royalty with Tricoat as same distributor is selling Tricoat product? What sort of Royalty payment we see there? Tricoat is APL Apollo’s baby. We are not talking about any such arrangement with Tricaot. Tricoat has 50 – 60% same distributors as APL Apollo. Majority of volume will be from APL’s distribution.

• Merger of Apollo Tricoat with APL Apollo for creating vale for APL’s minority investors? APL holds 51% stake in that. For future merger, cant comment now.

• Can we go above 100% capacity utilization? I think depending of size, SKUs, we can maximum operate at 90 – 95%. If we make just one product we can target 100% utilization but not with the wide product range we are making.

• CFO during 9M and H1 – 9M its 265 crore and H1 was 305 crore? It was on account of line by line merger of Tricoat. Any addition is negative for consolidated company. Slight decline in creditor days led to decline in CFO.

• Normal working capital is 30 days for the company.

• No comments on the merger of APL and Tricoat.