20% growth in volumes in Q2 (11% on like for like basis) - link

Recently APL Apollo bought a distress plant from a subsidiary of Shankara Buildcon for some 70 Cr.

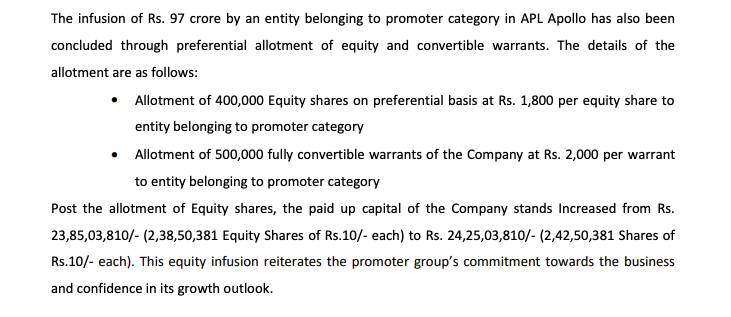

At the end of the above note this information regarding capital infusion was given.

This shows the confidence of the promoter with his business. That is indeed very good. If one tries and asses closely this infusion was done for the plant acquisition of shankara buildcon.

In the same press release it was mentioned that shankara was operating the plant at 40% and APL under its umbrella can operate the same at much better levels. Another important point is shankara has done a contract with APL that it will buy 2.5 lac ton material in Fy2020 which APL says will assist their volumes and the said contract is an exclusive one.

How it benefits APL (these are my assumptions and i could be wrong also here)

- Say APL has overpaid for the plant by X amount. The traditional method for accounting this is in cash flow from investing activities.

- Now APL (the money it has overpaid has to get back the same) over bills its inventory and sells the same to shankara (exclusive contract 2.5 lac ton which will assist volumes). The money received goes in cash flow from operations hence also affecting free cash flows from next period.

- Company key highlights is focus on cash flows.

https://www.aplapollo.com/wp-content/uploads/2019/05/APL-Apollo-Q4-FY19-Earnings-Presentation.pdf

Page No 7 & 8 in this presentation.

This show the strength of the business with increasing and improving Cash Flows.

How it benefits Shankara

- Shankara is in stress. They get to release their working capital tied up in their business by this stake sale.

- They get to pay down their debt with the same to some extent.

Shankara is the second largest player in southern region (again as per the press release) which was not able to efficiently use the plant (40% utilization levels) / Suddenly that same acquired plant has ramped up to efficient usage in just 1-2 quaters going forward.

The max growth in volumes and realizations the company is getting in GP (Galvanized segment) the in efficient plant acquired from shankara.

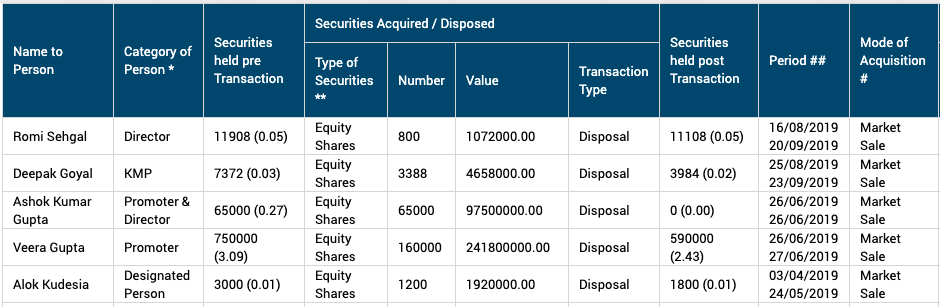

All looks like too good to be true. And when promoter shows confidence in business by infusion capital via pref allotment and warrants during the same time promoter is also selling their stock in open market sale (as per bse disclosures)

The confidence fading away in a time of few quarters.

2 Likes

Few points on steel pipe industry from CRISIL; though the report is few months old but I found it to be very interesting

• Demand for steel pipes likely to grow 7-8% in next five years compared to 4.5% in last five years. Growth would be higher for ERW at 8-10% as against 5-6% for S&S (Submerged Arc Welded and Seamless)

• Water supply, sanitation, irrigation and increased usage of structural pipes in infra to drive demand for ERW pipes

• For S&S, the main growth drivers is oil & gas

• CGD orders will require at least 10,000-15,000 KM per annum of pipes through fiscal 2029, entailing an opportunity of over Rs 5000 crore per annum over 10 years

• Generally, steel pipe makers work on conversion margin, which insulates them from price risk to a great extent

• Most of the pipe maker have completed capital expenditure programme in FY19 and have enough headroom for capacity utilization

• ERW pipe capacity utilization for FY18 was 59% and in FY19 was around 63%; next round of capex will start only when the existing capacity utilization will reach 80-90%

• S&S capacity utilization in FY19 was 46% and likely to increased to 50% in FY20

• For ERW pipe maker, sharp movement in hot rolled (HR) coil prices is key factor to monitor

• Steel pipe contributes around 8% of India’s steel consumption

• Steel pipe industry size Rs 50,000 crore, split equally between ERW and S&S (in value terms). In volume terms market split is 70:30 (ERW:S&S)

• Operating performance of S&S players was impacted in FY16-17 due intense competition of Chinese players; but performance improved in recent times due to implementation of anti-dumping duty

• Square ERW pipes (door and window frame) pipes, which are widely used for construction, are expected to be the fastest growing segment in steel pipe

• In ERW pipe segment share of unorganized player is expected to reduce to 40-45% by FY22 from 50-55% currently

• Ductile iron pipes is a major substitute for SAW pipes

• Margin for ERW players got impacted by around 150 bps due to inventory loss

• Govt. in December 2016 has extended the provisional anti dumping duty on seamless pipes (355 mm and lower diameter) from China by five years

4 Likes

In the last 10 years APL Apollo has outperformed its closest peers significantly. Revenue for APL Apollo grew at a CAGR of 29.8% (through organic and inorganic route) while Surya Roshni posted a revenue CAGR of 13.7%. EBIT margin is also superior to its competitors; 90 bps higher in FY19, which is significant in such a low margin business. Hopefully it will improve further with their recently launched valued added product (DFT and Tricoat).

I have outlined the above in the following graph

2 Likes

along with DFT and tricoat, I believe acquisition of shankara would also add to margins.They were APL’s biggest competitor in south. This will give pricing power. Additionally they have got 2,50,000 tonnes of committed volumes from shankara.

1 Like

Change in shareholding structure of Apollo Tricoat: I have observed one very interesting point that “INTEGRATED MASTER SECURITIES (P) LTD.” which acted as “Buying Broker” for “SHRI LAKSHMI METAL UDYOG LIMITED” (100% subsidiary of APL Apollo Tube) to acquire Apollo Tricoat during open offer in 2019 also acted as “Buying Broker” for Saket Agarwal (promoter group with 12.69% stake) to acquire the company in 2016. Saket Agarwal’s stake in the company has been reduced to 12.69% as of 30-September-2019 from 39.04% in June 2017. I have just one query regarding the acquisition of Apollo Tricoat; why APL Apollo Tubes acquired Apollo Tricoat via Rahul Gupta (son of Mr. Sanjay Gupta, Chairman of APL Apollo Tubes) instead of acquiring directly.

I have attached the shareholding pattern of Apollo Tricoat.

Apollo TriCoat shareholding.xlsx (12.3 KB)

3 Likes

Q2 results (Link)

Decent results. Industry leading volume growth (expanded market share) but EBITDA declined because of overall demand slowdown and low steel prices. EPS doubled because of deferred tax.

Company is guiding for better capacity utilization and better profits from Q3.

@zygo23554 any comments would be helpful.

Thanks

Disclosure: Invested

1 Like

The results are bad compared to last year. PBT has declined from 41 cr to 26 cr. That’s a huge drop. This is largely due to increase in other expenses from 79 cr to 106cr. These are consolidated numbers. Standalone results have loss before tax.

Disc. Invested tracking qty.

4% increase in market share is a huge positive in my view.

1 Like

For apl apollo inventory loss has been the biggest contributor to reduced pbt. Steel prices have corrected during the quarter. Going forward this scenario shoukd improve.

Concall will provide more details and guidance

5 Likes

This was known. One could gauge from Ashok Gupta’s investment in Shalimar paints and the amount of time he was spending there.

Highlights of Q2 fy 20 concall.

realizations:

Hollow section-Rs.40,500/tonne

GP pipe-Rs.48000/tonne

GI pipe-RS.50000/tonne

Black round tubes-RS. 40000/tonne

• EBITDA per tonne-Rs.2104.

• Cause for low EBITDA per tonne:

- lower capacity utilization

- inventory loss due to steep fall in steel price.

- branding expenses.

• On inventory loss: there is 8-10 days of window period for passing on change in raw material price. Inventory days is 37 days. Both above factors result in loss of value of inventory whenever HRC prices fall.

Inventory days can be brought to 25-30days. Lower volumes lead to higher inventory and hence higher the loss. In Q4 19 and Q1 20, when volumes were above 4 lk tonnes, there was no inventory loss. but in this quarter, volumes fell so faced loss.

• Inventory loss is to the tune of 20-30 crores.

• Maintain full year target of 20% volume growth (including tricoat).

• Working capital days may increase slightly in H2 due to higher volumes.

• Net debt will be reduced in H2. Finance cost is around 9%.

• Break up of Increase in fixed assets:1) 250 cr in tricoat.

2) 70 crores for acquisition of secunderabad plant.

3)122 crore for cold rolling mill and expansion at Raipur plant.

• Current market share is 40%. second largest player has 12% market share and 30% lower EBITDA and twice more debt than us. gaining market share from both organised as well as unorganised players.

Disclaimer: I hold this stock in my core portfolio at an average price of 1100. Have carried out transaction in past 3 months.

5 Likes

I echo the same view. Despite the fact that both entry and exit transactions were done at the same price, there seem to be old links/history with the previous owner (Saket Agarwal) which makes the whole transaction structuring very fishy.

Time gap between the two transactions – Rahul Gupta acquiring Apollo Tricoat and APL Apollo buying stake in APL Tricoat from Rahul Gupta is not even 2-3 quarters. Primary explanation given was land – which seems like a made-up explanation. Surprized that they didn’t know this 3 quarters back.

Saket (previous owner) was well known to the promoters earlier as well. See links below:

- Saket was amongst top 10 shareholders in APL Apollo at one time, held around c.8-10% https://www.bseindia.com/stock-share-price/apollo-pipes-ltd/apollopipes/531761/disclosures-insider-trading-1992/)

- Saket was a shareholder in Lakshmi Metal Udyog Limited as well, when it was acquired by APL Apollo (see this http://www.capitalmarket.com/Company-Information/Corporate-Actions/EGM/APL-Apollo-Tubes-Ltd/12334

There was allegedly stock manipulation in Best Steel logistics before it was acquired by APL – see article dated Nov 2017 (https://www.moneylife.in/article/stock-manipulation-best-steel-logistics/52248.html)

This price was rigged up, volume weighted avg price during 60 days prior to open offer was Rs 110 and open offer was at rs 120. The price was probably rigged up to present a picture that the acquisition was being done at fair value. (https://www.sebi.gov.in/sebi_data/commondocs/apr-2018/beststellfinallof_p.pdf)

The above links makes me suspect that this was definitely not an independent market transaction. On the face of it, the promoter bought and sold the stake in Apollo Tricoat at the same price, but there could be more behind the scenes.

The underlying business at both APL Apollo and Apollo Tricoat is doing well, but the above points are quite concerning. Would be keen to hear other perspectives on the above.

13 Likes

Hi All,

Any reason for the recent rally in APL apollo? Looks to me like a shift from large caps to quality mid caps as there’s a limited room for further price movement in large caps. Do you concur with this view?

P.S. I’ve been holding APL from the last one year at ~1350 level

Having been invested into this story since 2014, I can say with some degree of confidence that the stock usually has the best run when the steel prices are on an upswing. The biggest problem plaguing the business is inventory losses when HRC prices turn volatile, one can see inventory losses in Q1 and Q2 this year which hits EBITDA per MT and PAT margins badly.

Once HRC prices stabilize and start to move up, company gains on existing inventory and EBITDA moves closer to their stated goal of INR 3400 per MT. Of course this also increases the borrowing for the company due to WC needs but that is a decent trade off in favor of higher PAT margin.

If anything the market situation of the company has gotten stronger over the past 2 years, they are planning to spend 50 Cr on adverts, one can see the ads pretty regularly now. I am guilty of needling them on the Q2 conf call on this point since 50 Cr for a start is large ASP spending in a category where no one has done ASP spending so far (I still don’t buy the hypothesis that APL falls into the building materials category on the lines of Cera, Kajaria, Greenply etc. Spending 25% of PAT on ASP unless one is very confident of ROI is not something I am convinced about, however I do hope the management is right and I am wrong on this front). A stable/good run in HRC prices should naturally get investor interest back into the stock, especially after the PAT number starts getting better. Will be interesting to see how Q3 and Q4 pan out

Disclosure: Invested for self and customers, have added to position over the past 30 days. This continues to be the biggest holding in my personal portfolio and my views may be biased.

21 Likes

Very strong 50%+ growth in Q3 volumes Link

Looks like advertising spend is showing results.

Disclosure: invested. Top 3 holding

6 Likes

Company sharing its quarterly volume performance on the 1st day of the next month… never heard it from industry like pipes and tubes. If they are doing it every quarter, then I am fine. If not, this is clearly an attempt to share information only when it is good…

Disclosure - not invested, not in watchlist

They share it every quarter.

Disclosure

Invested

3 Likes

Won’t go too much into the Q3 results, what is interesting are the possibilities from here and how the market view towards the story could evolve…

Steel prices were struggling till Nov post which they bounced back to some extent. So there must have been some inventory losses till 3rd/4th week of Nov, this shows up in the EBITDA/MT number which is just around the usual range of INR 3400 per MT. Apollo tricoat products work at much higher EBITDA per MT, so adjusted for that the core business has only done a decent job on this front, not yet a great job.

If steel prices continue to be stable/favorable over Q4, possibility of higher EBITDA margin goes up. This combined with healthy volume growth offers the possibility of -

- Healthy revenue and healthier PAT

2 Since there is no capex planned immediately, high OCF and FCF. OCF yield for 9M (Op Cash Flow/EV) is more than 6% - Debt levels coming off and quality of the balance sheet getting materially better

During the positive cycle in such stories (which have to live with some extent of cyclicality) market starts looking at such mini virtuous cycles that can play out, during the negative cycle the business suddenly becomes an average quality business with ROCE < 18% and looking not so appealing.

Come to your own conclusions, the market reaction to this over the next few sessions will tell the story on how this is being viewed in the context of rating/rerating/derating. Time to get second level thinking hats on, everyone knows what the numbers are anyway ![]()

Disclosure: Invested for self and customers, my views may be biased

19 Likes