Hi Guys,

Did an analysis on PSU banks, idea was to see how they did during the last down cycle of 1998-2002 and look for any patterns that might exist. Posting here the full note, link to blog is here:

At the moment public sector banks (PSBs) are going through a rough patch – increasing stressed assets and scarcity of capital are two major causes of worry. This has meant very low valuations for these banks and inability to grow at historical rates even if the economy starts to pick-up in near future.

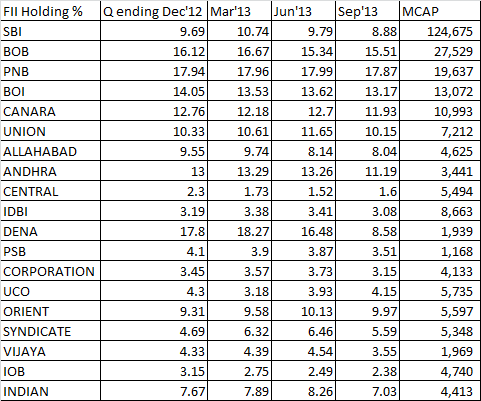

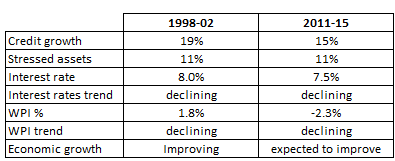

Last 3-4 years have been very challenging for banking sector as a whole and more so for PSBs. Low credit off take in the economy coupled with crippled risk management at PSBs ensured poor asset quality. Below is a snapshot depicting how situation has deteriorated over last 4 years –

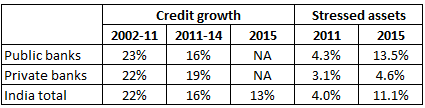

A look at previous down-cycle of 1998-2002 shows that PSBs had stressed assets at ~13% of loan book. Couple of the banks# had stressed assets as high as ~30% of their respective loan book. Credit growth slowed down to 16%. Banks* traded at an average P/B valuation of 0.6x during this period. What followed after that is history – from 2002-2008, loan book grew at a CAGR of 24%, stressed assets declined from 11% to 3%, stock prices** returned an average of 800%. During the same time period benchmark index BSE SENSEX returned 350%. What triggered this outperformance? There are several reasons for that, all intertwined with each other, namely 1) decline in interest rates, 2) GDP growth, 3) declining NPAs 4) recapitalization by promoter

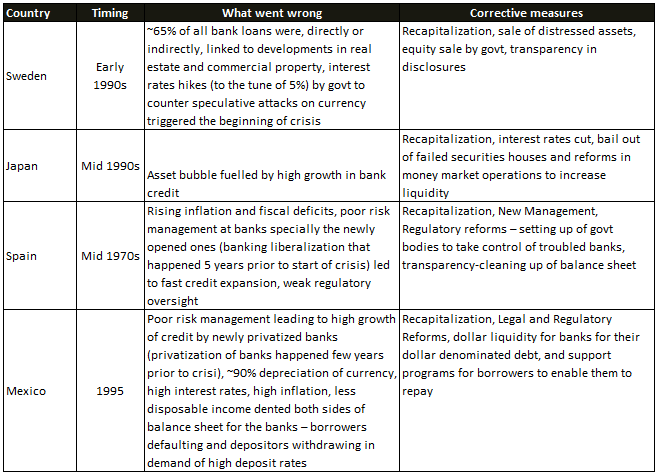

There are similar examples of banking crisis in other countries. Common measures undertaken to improve the situation of banks were, recapitalization by respective govt, interest rate cuts and regulatory reforms. Please see below for a brief summary of banking crisis in Sweden, Japan, Spain and Mexico.

Changing Scenario

Economic growth seems to be the top priority for the Modi govt. As per Madan Sabnavis, chief economist, CARE Ratings, 8-10% real GDP growth (base year 2004-05) will require credit growth of 18-20%. Historically, credit growth has seen a multiplier of 1.3x of nominal GDP growth rate. PSBs form 76% of total credit in the system and their full-fledged participation will be crucial for the desired economic growth rate of 8-10% (base year 2004-05). As per some estimates PSBs are expected to grow at a meagre rate of 8-10% for next 4-5 years because of scarcity of capital. This will lead to slow credit growth of ~12-13% in the system which will not be sufficient to grow the economy by 8-10%. From the above argument, we can deduce turnaround of PSBs should be the indirect top priority of Modi govt. In fact there are some early sings of changes already in place such as declining interest rates, improving macro numbers such as inflation, IIP etc and announcements around banking reforms which include more autonomy to banks, top management hiring from private sector, performance linked salary structure for top management, longer duration of MD, separate posts for chairman and MD for better board governance, construction of bank board bureau, recapitalization and reforms in industries causing maximum NPAs etc.

MD for better board governance, construction of bank board bureau, recapitalization and reforms in industries causing maximum NPAs etc.

Is there a pattern that we can draw between last down cycle and the current one? Table below compares two down cycles on few key metrics:

In addition to this, the other pattern that emerges between the two down cycles is recapitalization^^ by govt of India. Until 2002, recapitalization was done to the extent of 12,000 Cr, which provided enough liquidity to grow by the time economic growth picked up, which acted as a strong catalyst for turnaround of PSBs. Between FY02 - FY08, loan book of PSBs grew at a CAGR of 24%. We see similar pattern emerging this time around, by fiscal 2015 end, govt had already infused ~65,000 Cr of capital into PSBs and has further plans to infuse 70,000 Cr during next 4 years. Capital being the life-line of a bank, these recapitalization plans might, once again, provide required breathing space to PSBs. Using this capital, they, once again, have an opportunity to improve their balance sheet enough to attract outside capital which can further provide them breathing space to grow like before.

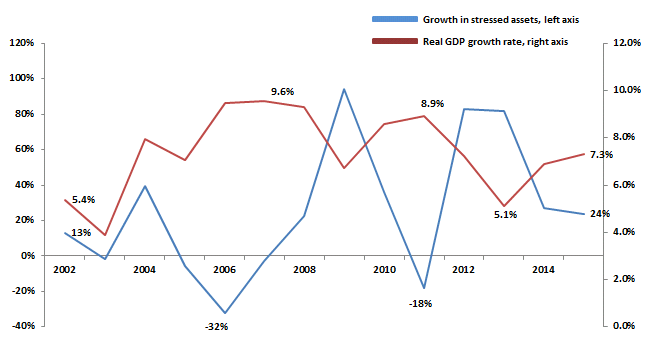

Inverse Relationship between growth of GDP and of Stressed Assets

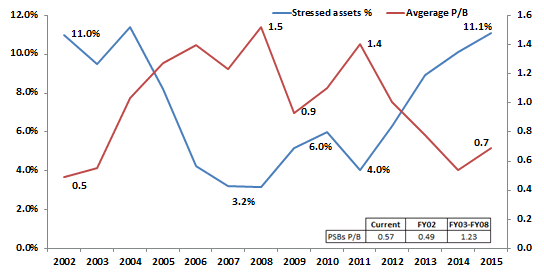

Banking is a cyclical industry in-tune with economic growth. Asset quality of banks deteriorates sharply when economic growth engine slows down because of poor cash flow generation at borrowers’ end. Asset quality situation reverses when growth picks up as visible from the chat below:

Current valuations of PSBs seem very attractive if we compare them to last down cycle and how they improved during the ensuing economic recovery. Chart below demonstrates strong correlation between asset quality (stressed assets) and valuations (P/B):

We might question quality of the book PSBs carry on their balance sheet making P/B metric irrelevant. Well, that has always been the case, is this time any different?

Comments Invited!

Notes –

- There were 10 PSBs listed on stock exchange starting 1998

** There were 17 PSB stocks listed in 2002

^^ During whole of 1990s govt infused ~16,000 Cr of capital, 2% of GDP and over the last 15 years govt has infused 81,000 Cr of capital into PSBs, majority of which came during last 5 years

Source: Ace Equity, RBI, Press Search

Disclaimer: This is not a recommendation to Buy/Sell/Hold. Registration Status with SEBI: I am not registered with SEBI under SEBI (Research Analysts) Regulations, 2014. As per the clarifications provided by SEBI: “Any person who makes recommendation or offers an opinion concerning securities or public offers only through public media is not required to obtain registration as research analyst under RA Regulations”