This is the start of my investing journey. I actually have been actively investing for 8-9 months while actively learning for a year now. I am basically an amateur, let alone a cycle: I haven’t even lived past a whole financial year. However, I am only 19 years old and I am keen to make a career out of it and that’s why I want to continue going forward.

The reason I am starting this topic is so that I can journal my investing journey, note down what I learn everyday and observe a change in myself in the coming years.

So lets begin!

My investment approach

My goal is to find businesses which can grow earnings by 20-25% over the next few years and are available at reasonable valuations. As a beginner, I might overestimate the potential of my investments. and pay at a premium they don’t deserve. However, that’s part of the game and I intend to improve.

I prefer betting on sectors first, and then shortlisting stocks in that sector which suit my investing approach of earnings growth+ valuations.

Caps and types of stocks

I do not have a problem in investing in any types of caps. I prefer small caps as they can grow faster but if a large cap can deliver the same, I am fine with it.

I also do not have a problem with investing in cyclicals, turnarounds etc. The only problem is I do not know if I am good enough to tackle them that well, but I am agnostic to that.

Portfolio allocation

I am a very strong believer of concentrated bets. However, no stock exceeds 10% mark in my portfolio. The only reason is because I want to further refine my skills before taking riskier bets.

technicals

I started off as a trader and I still actively trade, so technicals is my strong suit and I use them in evaluating my investments, but not deciding whether to buy or not on the basis of charts. I haven’t exited businesses based off of technicals, but I think they can be a good signal in terms of taking sell calls so I am open to that.

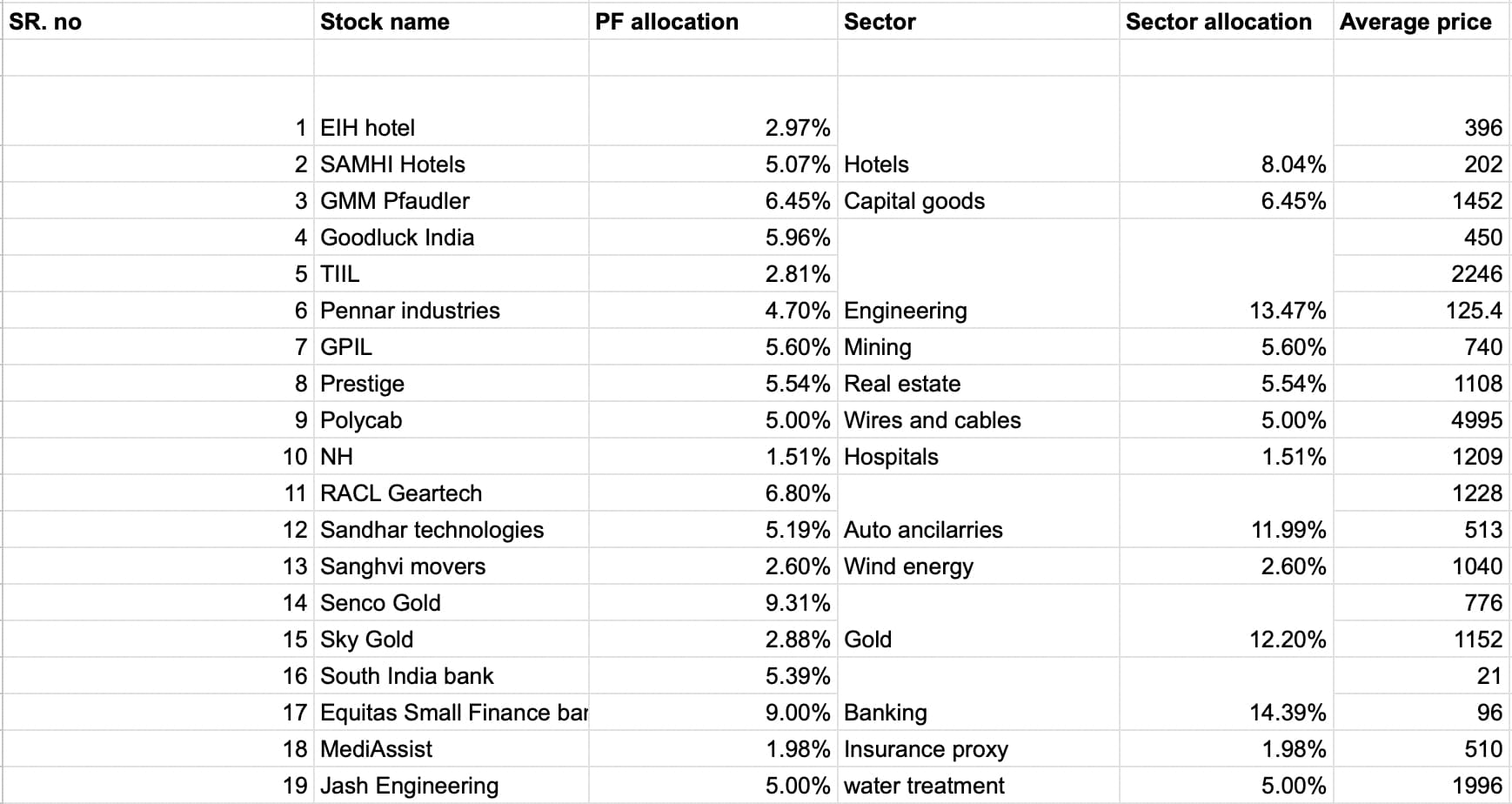

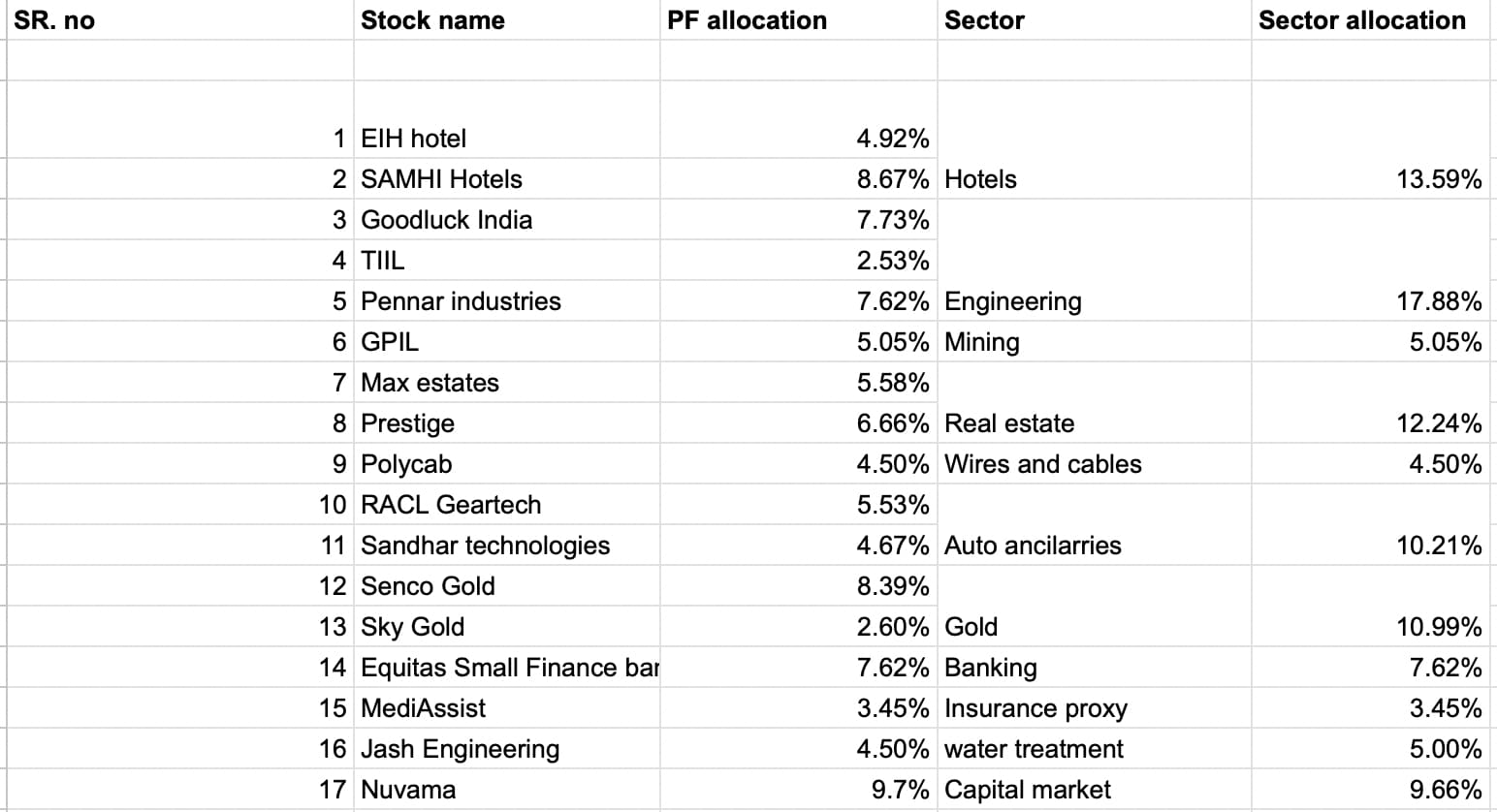

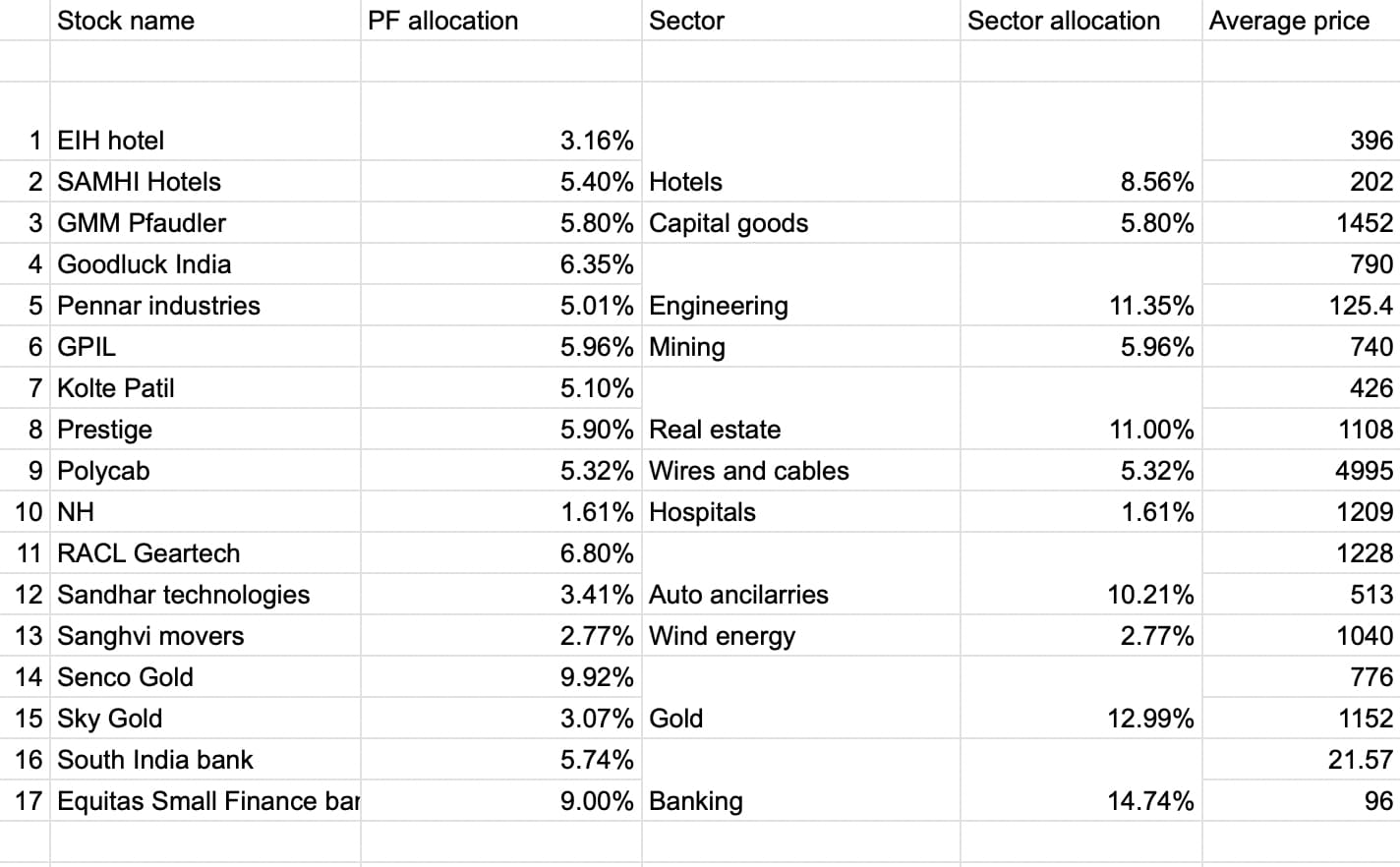

Here is my portfolio, with the exact weightage

I am bullish on the following sectors: Hotels, real estate, Financials, selective capital goods and auto ancillaries, retail jewelry, mining, hospitals and wires & cables.

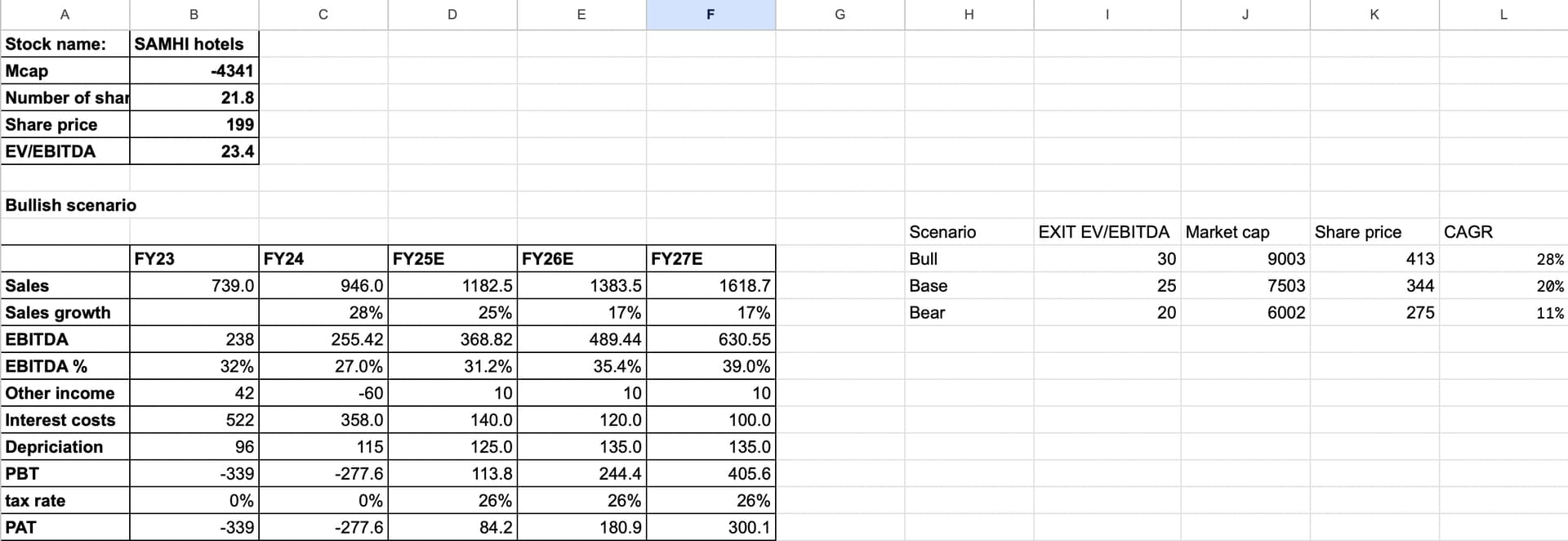

Business I am the most bullish on: Senco, Pennar, Prestige+Kolte patil, Samhi, good luck, GPIL and GMM.

PS. These are not my starting buying prices, I have averaged up in most of them except GMM.

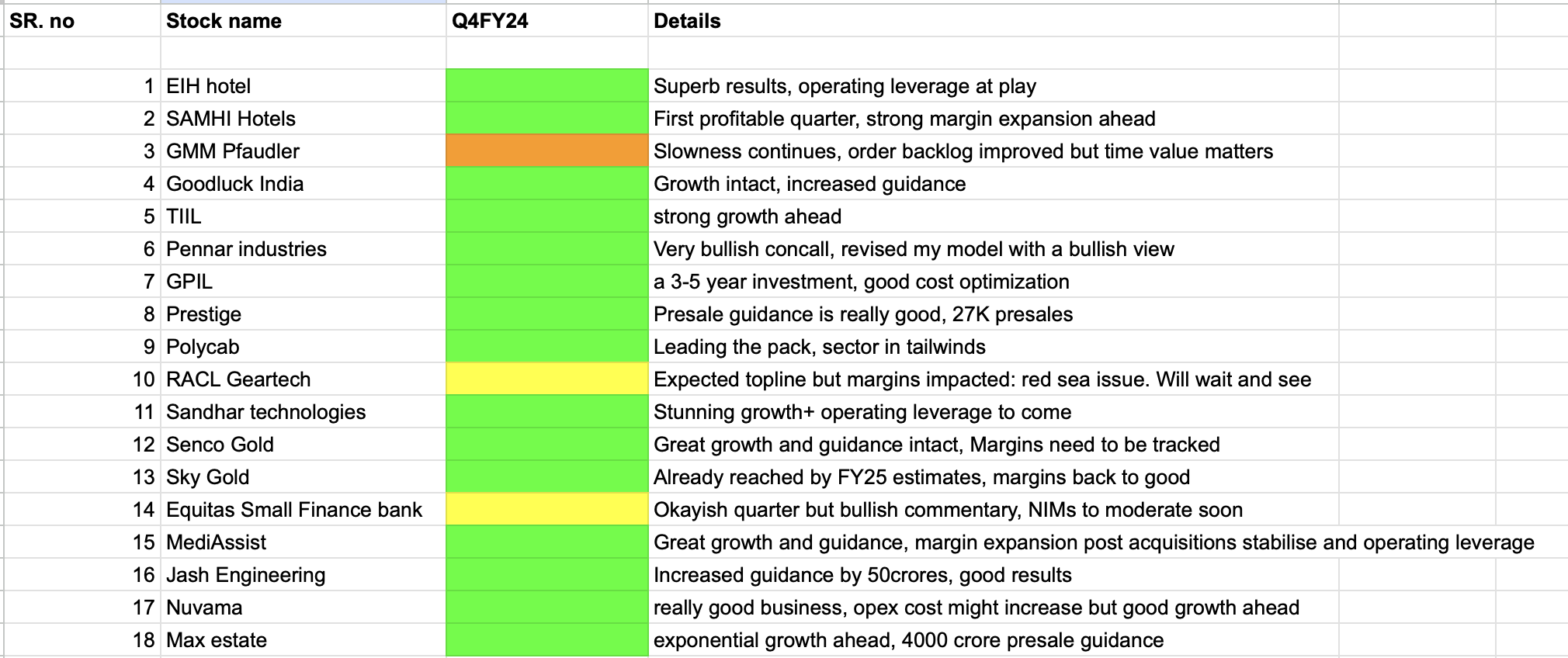

Disc: nothing is a buy or sell recommendation. I will give updates on a monthly basis and share my learnings as I go ahead.