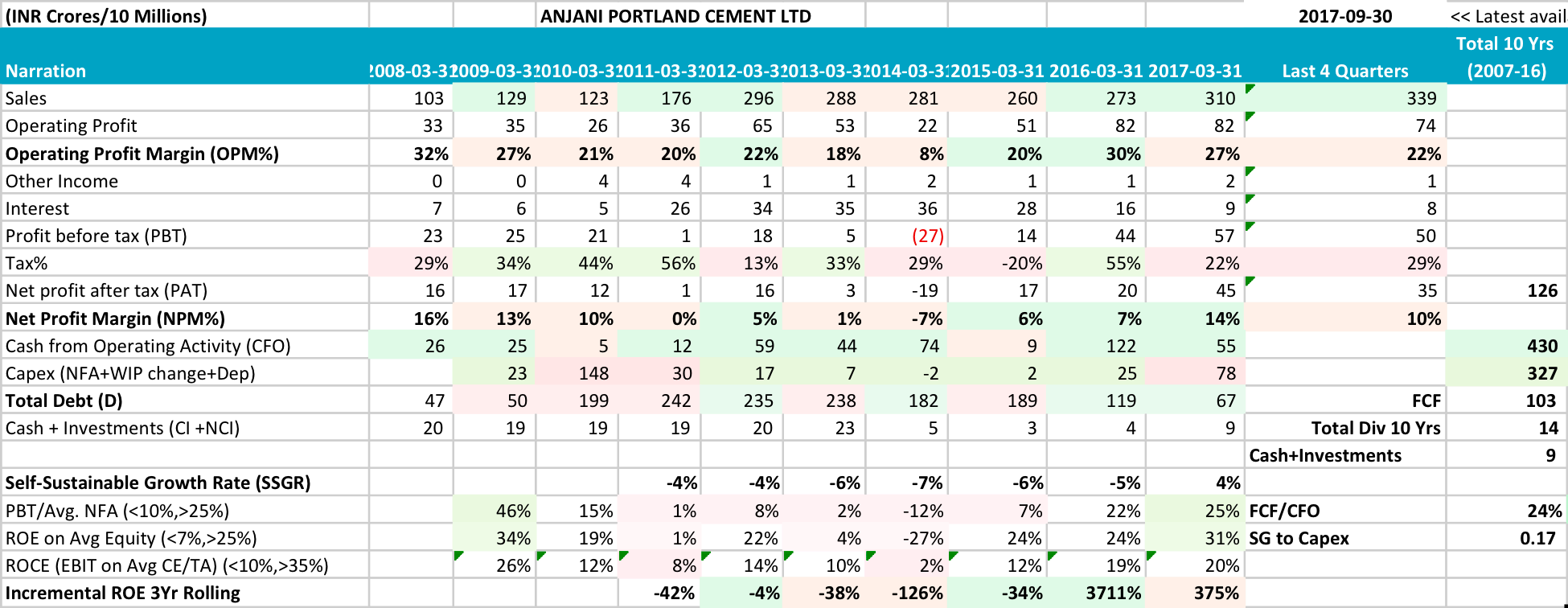

Anjani Portland is a small cement manufacturer with presence in Andhra Pradesh. It is closely linked to the cement cycle, as is evident from its financials. However, the firm has been able to pay down its debt significantly- from 242 cr in FY 11 to 80 cr now. This makes it far better placed to weather a downturn. For instance, an increase in the price of coal as well as increases in freight charges ate into operating margins in Q2FY18. However, the NPM did not decline as drastically as in FY12 and FY13, since interest costs are far lower now. Like most cement cos in the south, the firm operates at ~70% capacity. EBITDA margins have been at their lowest for the last 4 quarters yet Anjani is valued at just 7.8x EV/EBITDA, which is at a significant discount to many of its peers who have more leverage.

I see this as a mispriced bet. The replacement cost of a 1 MT cement plant is estimated to be USD 135-140 per MT. With 1.15 MT capacity and given that Anjani’s capex still has 80% of its life remaining, this would put its replacement cost at ~ INR 800 cr + another 80 cr for its captive power plant = a total of INR 880 cr. It currently trades at a market cap of INR 600 cr, which provides a 30% margin of safety.

Risks:

Freight costs are up 150% this quarter and the explanantion provided by the management is that the have moved from ex works pricing to FOB. However, other cement cos have not seen such a sharp rise in freight costs

Their presence at a single location may restrict their growth in the future.

Did u compare Anjani with NCL Industries which is a small sized cement company in Andhra. They recently came out of CDR, paid the money to Piramal through QIP and also have panel division which is doing good. They completed their capex and expecting to pickup after the infra push in Andhra.

Anjani being a Chetinad group, have experience in cement and their financials seems to good, recently reduced the debts and capex is increased.

Also DII are accumulating NCL and not Anjani. May not be a major criteria, but why are they doing is another question. Also some of the reliable stock letters also recommend NCL instead of Anjanji.

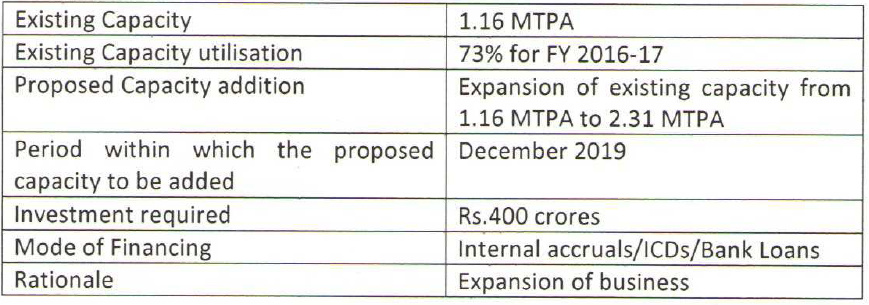

Anjani is adding capacity which is operational from 2019 whereas NCL is already with ready capacity

Below point mentioned in the AR 2017,

in AR2017, there is no related party transactions expect loan and interest which is already paid. But below message AR is worrying,

“RESOLVED THAT, pursuant to the provisions of Regulation 23 of the SEBI(Listing Obligations and

Disclosure Requirements) Regulations, 2015, consent of the members of the Company be and is

hereby accorded for transactions relating to transfer of resources, services, obligations, between

the Company and Chettinad Cement Corporation Private Limited a related party of the Company

as per the provisions of the Companies Act, 2013 and Listing Regulations, for an amount not

exceeding ` 300 crores.

This company seems to have decent top level financials: 21% 5 year ROCE, 11% Sales growth in last 5 years and is available at ~1.2x pre-covid sales. I wonder why it is so cheap, whether this is due to the low market cap and thus low institutional ownership. Looks like a mispriced bet worth studying specially with revival of the cement cycle.

Hello Sahil, any finding in particular after studying?

Looks like value buy at CMP.

Technical suggests Consolidation and might be ready for takeoff.

Some VPers mentioning about Sugar like Momentum might come to Cement sector.

I had actually thought of investing in anjani Portland. Was highly undervalued but I quickly realized that investing in cyclicals actually goes against my fundamental nature since I am always worried about when to exit: have valuations run too far ahead of fundamentals. Which itself is dependent on price of a commodity. Requires a lot effort to track macros too: demand of cement in region X, infra projects in X, other competitors entering the region. All of this because commodity producers cannot set prices. Market sets prices. My key takeaway from this experience was to know my circle of competence and to stay inside it, lest I burn my hands and the capital with it.