Angel One --CNBC Interview with CEO N Gangadhar --Q2FY23 -Earning Highlights --17th Oct22 :

–Payout in 1st Friday of the Qtr will be beneficial for us. We are tech enabled so it did not have any impact. Infact the next Monday of the friday transfer --the no. of orders actually went up by consumers.

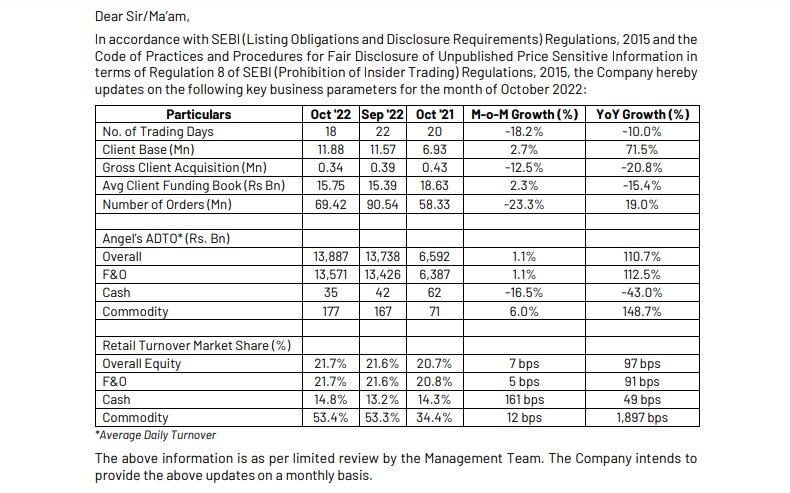

–Revenue per client has been declining ( Q2FY23 its at 430/-per client from 544/- per client last year Q2 ? --As the mkt has expanded , the volumes have gone up and its at all time high & ARPU has declined and it will trend down-wards.

With Economies of scale the order volume is going to go up so we are not really focused on ARPU decline but focus on client acquisitions and tech/innovations.

–The tech and product innovations will increase our margins, we are currently at 45/50% OPM & for the last 3 Qtrs we are operating at 52%

–Added 1.2Mn new clients last Q2FY23 , run rate will be ? --Out of all the brokers in India only a few of us are adding clients , The rate of cust. addition is going to increase as equity participation is only 5% and nationally the country has 8 to 10% additional head-room for growth. So the next 3 yrs we will see the broking industry grow 3 or 4 times & we dont see any slow-down here.

–FY23 growth ? --Client acquisition to grow at 3.5 to 5 lakh clients per month and this will continue for the next 6 months.

–We are a growth company and solely focusing on topline and bottom-line to create share-holder value.

How is the company looking from a Valuation perspective?

FY23 Q3 numbers seem okay, with flat revenues but a rise in PAT and Market share. Currently, the company is trading at a P/E of 13 with a median of the last 2 years of 21, Market Cap/Sales of 3.9 with a median of 5. As the company got listed during the quantitative easing time, it won’t be reasonable to compare the ratios.

CapitalMind Podcast where Deepak Shenoy has explained the recent SEBI proposal to make available the fund blocking feature available to the primary market investors in the secondary markets too and how this proposal, if implemented, may disrupt the broking industry revenue.

CEO Narayan Gangadhar Resigns… Many investors have liked this company due to tech heavy leadership as the differentiator. With him gone and potential ASBA for secondary market coming, this stock will have tough time in near future

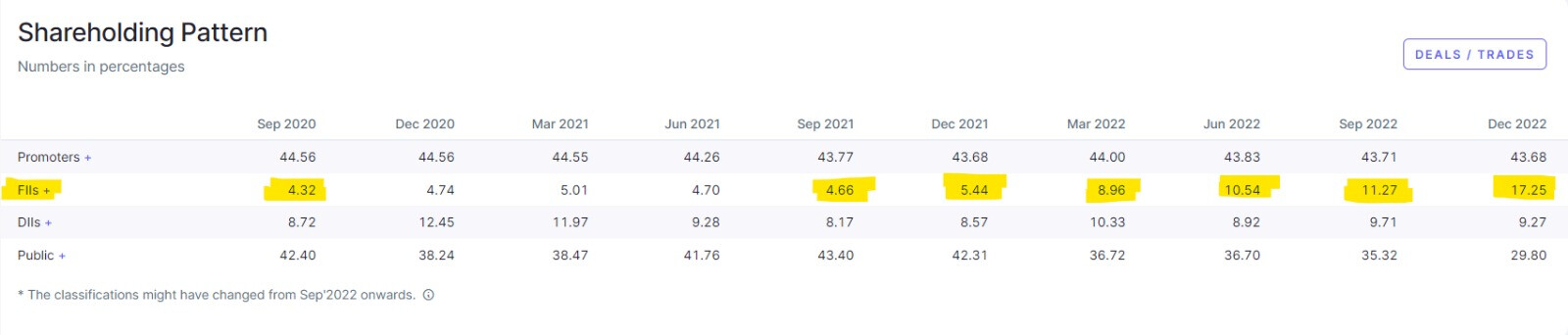

FIIs have significantly increased their shareholding in the company from ~4% to 17% in the most recent quarter filing. Even as the stock is correcting more and more instituational investors are taking interest in the company. Very rare to find a 40% ROCE business at PE of ~10x. Such are the times. This interest from FIIs is interesting.

I think with retail participation slowing, it will continue to weigh on the stock. The stock has been close to 10X for someone who times to perfection.

The daily market average volumes of non-institutional investors, mainly retail investors and high-net-worth individuals, stood at ₹22,829 crore in January 2023, the lowest since March 2020 and 61% below the peak of ₹58,409 crore in February 2021.

Technically, its bearish significantly below 40WMA and 200 DEMA. Next strong support around 950-975 which is also 38% retracement from ATH. If breaks that, even 600 is possible. Good company but will test patience.

Discl: based on limited knowledge, markets are supreme, sentiments can change.

Anybody know why is there such a stark difference between the capital structure of ICICI Sec and Angel one? Angel has a D/E Ratio of 0.36 whereas ICICI Sec has a D/E Ratio of 3.3?

Must be because of ICICI SEC having a far bigger size of MTF book where the broker offers margin trading facility to the borrower by charging interest to him against funds provided by the broker ( which are either raised at lower rates from Banks or out of his own reserves and surpluses )

Trying to gauge down the Float Income earned by Angel, found the following:

From FY 22 Balance Sheet:

Trade Payables - This mostly includes Client Deposit Money + some Settlement Payables to Exchanges - 4046 Cr

Cash Equivalents - 4452 Cr

In the Cash Equivalents the most important Item is Fixed Deposits under Lien with Stock Exchanges - 3165 Cr because this maps directly to a P&L entry. This is major constituent of Float Income in my opinion which is under attack from ASBA implementation.

From P&L:

Total Interest Income - 365 Cr

MTF - 252 Cr

Lending Activities - 12.6 Cr Interest on fixed deposits under lien with stock exchanges - 67.2 Cr

Interest on Deposit with Banks - 32 Cr

For FY23 the total Interest Income is - 519 Cr up by 42%

MTF Average Size for FY22 - 1484 Cr

MTF Average for FY23 - 1490 Cr

Avg ADTO FY22 - 6476 Cr

Avg ADTO FY23 - 13608 Cr

Trying to establish that a larger ADTO leads to larger Margin & Deposit Requirements and thus larger Float Income. Thus a major trigger for the Interest Income in FY23 can safely be concluded to be the Float Income from Fixed Deposits under lien with Stock Exchanges.

With Upstreaming of Client Funds applicable from 1/07/23 the impact is ~ 60 Cr. Add tax benefit PAT impact (50Cr).

Thus Cumulative Float Income under Impact can be said to be 200Cr. While this number relatively looks huge on PAT of 890 Cr there is a way out for Brokers which many decline now to implement but most likely will in the future.

Gross Broking is roughly 70% of Total Revenue - 2080 Cr. A 10% increase in this number can cover for the Float Loss which again directly flows to the bottom line due to Operating Leverage.

For Traders the biggest charge is STT & Exchange Turnover charges. Broking is relatively a small amount in the total cost for an order.

Thanks for the analysis. Overall it looks like this is 20% or so of current PAT runrate. It will be interesting to see how the industry responds to this asba implementation if any large broker like zerodha implements it, then everyone will have to do it to maintain feature parity. While this can lead to a small loss of income in 1 year, but imo leads to structural improvement in protection of market participants so imo is a good move.

Whether the loss will actually materialize also depends on how brokers treat the implementation. 3 options :

Dont implement (lose market share to other brokers potentially)

Implement & absorb costs to p&l (i believe will lead to flatlining of p&l for 1 year & then a growth on top of it subsequent year onwards)

Implement & pass on costs to clients in form of higher brokerage

It will be interesting to see which of 3 options industry participants end up picking.

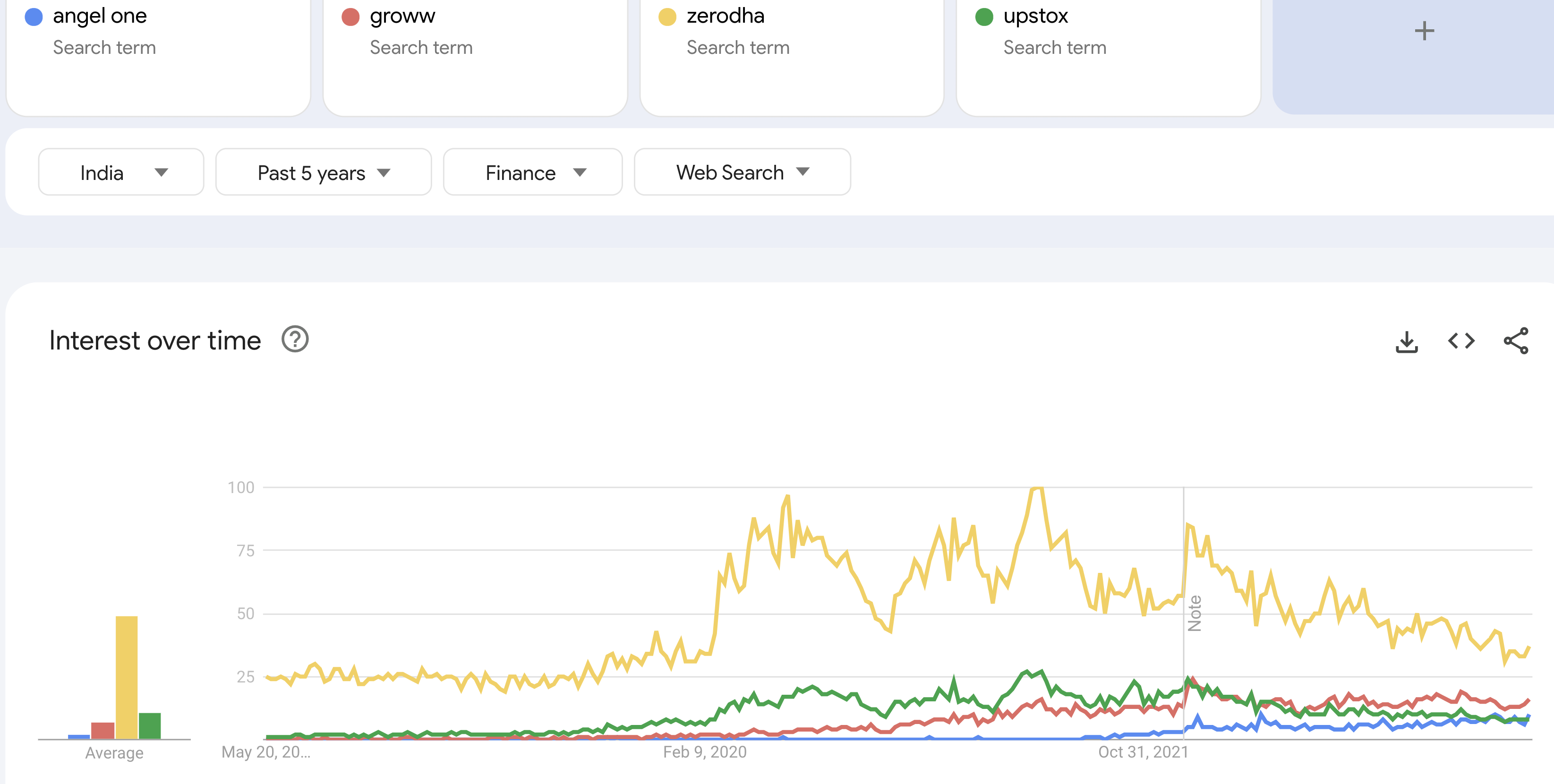

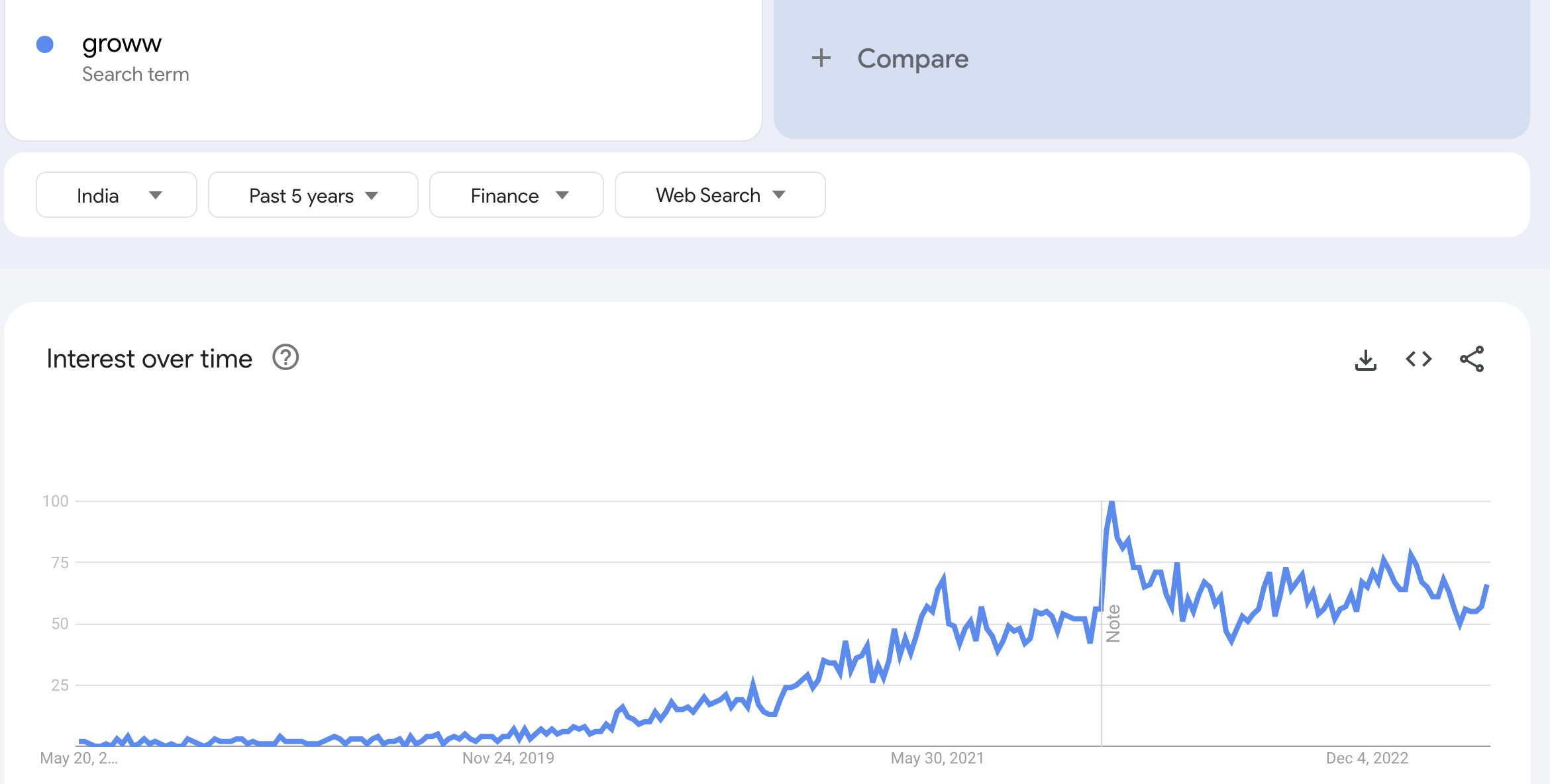

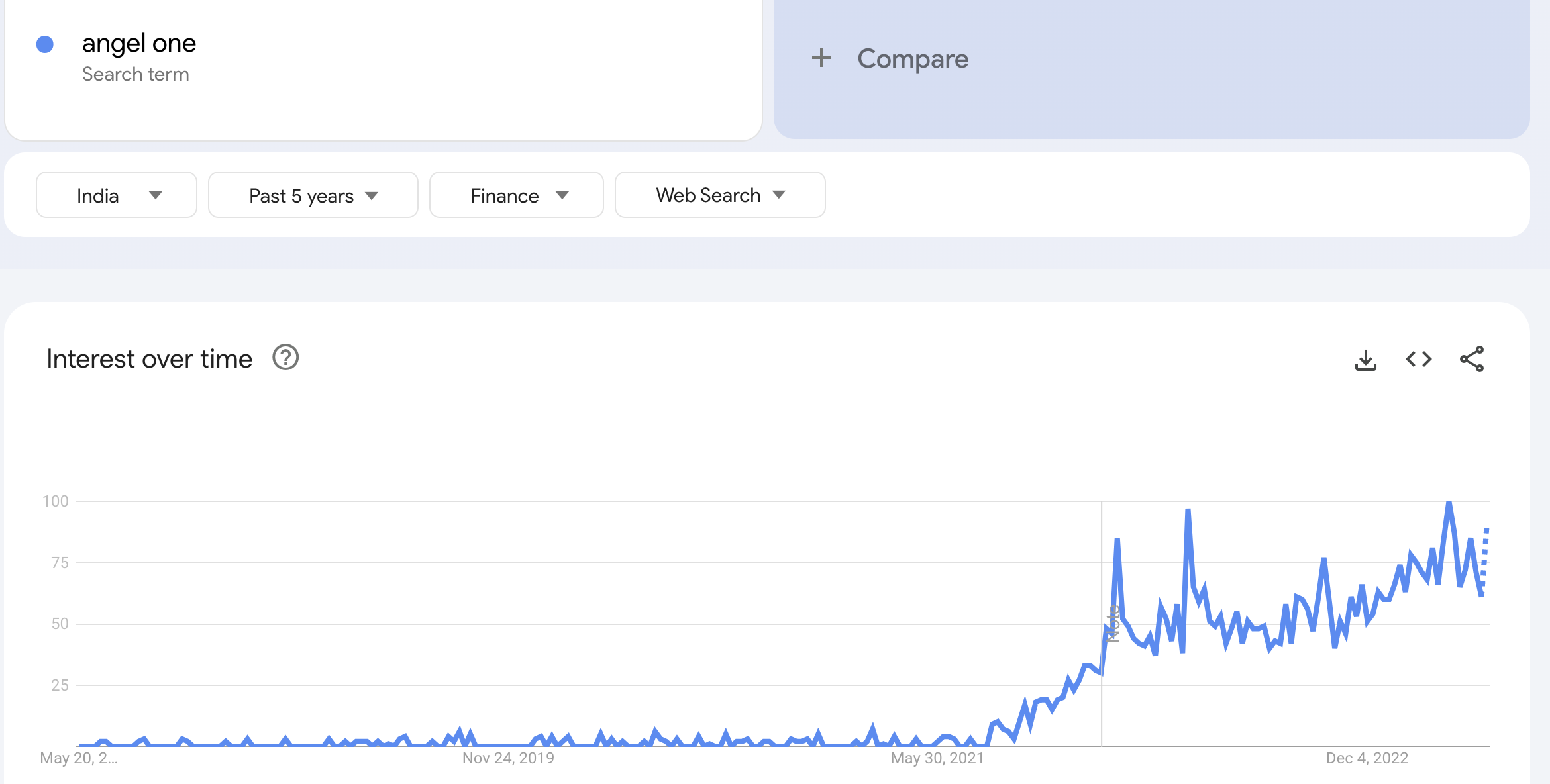

Zerodha remains the king in absolute numbers but the search interest trend is downwards.

Was Upstox was just paid acquisition?

These are just Google search trend. The above points are just my inferences of the data. For me its a proxy. You may questions that this data is incomplete in various aspects. Google search includes search made by existing client, searches by potential new users who eventually did or didn’t signup after the search.

One interesting thing I observed is Angel One’s Instagram has 1.1M followers however most posts have <300 likes which definitely to me indicates they would have acquired some click-farm followers.

Nothing related to the business in any way but it just felt weird. I even compared it with the account handles of other brokers and it seemed unnatural.

I am not able to understand why this business is trading at 12x PE.

ROE is >40%, Good growth, Net cash is >40% of the market cap. Dividend paying company.

Can anyone shed some light on what are the key concerns in Angel One?

Why should this not command 20x PE?