AngelOne Q2 Concall Highlights

Highest ever Revenue & PAT

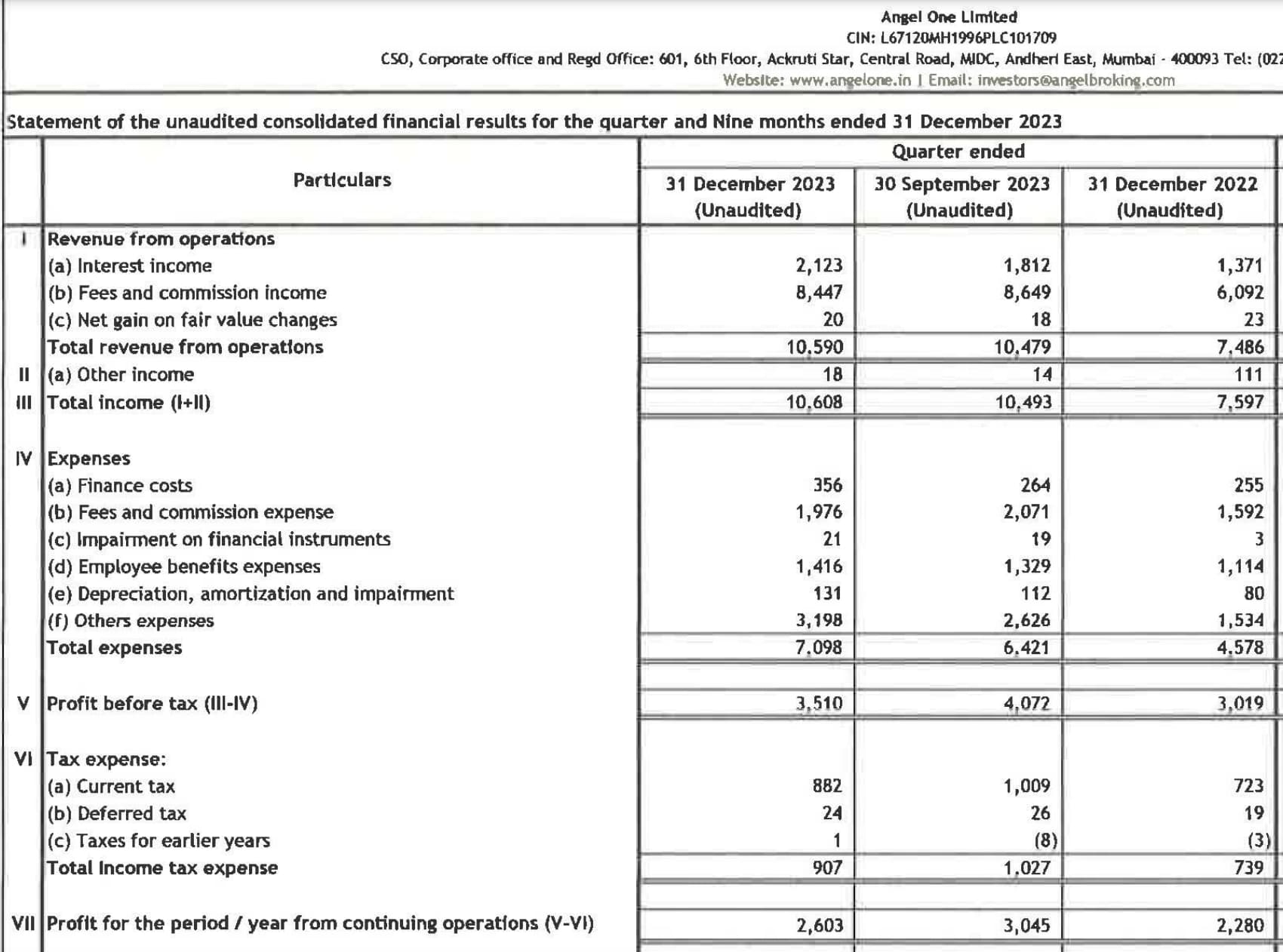

Total Income up 41 % YoY at 1049 Cr v/s 746 Cr

PAT up 43 % YoY at 304.5 Cr v/s 221 Cr

Dividend to be paid 12.7/ share

Total client Base at 17.1 Mn, up 48 % YoY and 13.3 % QoQ

Gross Client Acquisition Highest at 2.1 Mn up 80% YoY and 60% QoQ

Share in Active NSE client at 14.6%

Market share gains for the company in all the segments

Client Funding Book at 1946 Cr v/s 1193 Cr QoQ

Saw a good recovery

Net worth at 2612 Cr

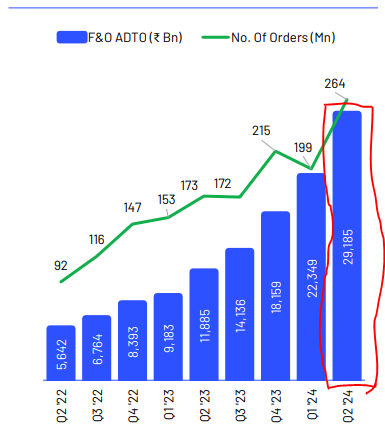

Cash Segment saw a good recovery in ATDO & No.of Orders

For F&O and Commodity segment there is secular growth every Quarter in the ATDO and No. of Orders

-New Business Verticals Update

1)Lending 2)AMC 3)Wealth Managment

The main focus of AngelOne is to expand the addressable market and product offerings.

It wants to scale up its existing broking business and diversify into a comprehensive fintech model.

It aims to leverage the benefit of its wide distribution, tech capabilities,and its existing user base.

Timeline of New Business Verticals:

-

AMC - To commence from Q4/Early Q1 FY25

The final approval was filed in August,business and tech infrastructure are in progress

Finally, it will be approved by SEBI through an onsite inspection, taking two quarters for approval.

-

Lending Vertical - Going live by Q4

-

Wealth Management - More details will be shared in the next quarters; it’s currently in the concept stage

More Details on New Verticals

-

Consumer Lending Products: AngelOne wants to become a distributor of consumer lending products (Unsecured Personal Loans) by partnering with NBFCs and Banks, with the balance sheet risk not being with AngelOne

It doesn’t aim to be just a vanilla distribution company but wants to utilize tech capabilities and AI/ML models using customer data to create customer profiles

It aims to assist with underwriting and collection processes, increasing commissions for AngelOne. There is tremendous potential in the retail credit business

-

AMC: The AMC will be based on Passive Managed Funds, Angel to benefit from the extensive distribution network

-

Wealth Management Solutions: AngelOne is also trying to enter the wealth management business, focusing on clients with a ticket size above 50 L/1 Cr or beyond.

They aim to use their technological capabilities to provide high-quality products and cater to HNI/Ultra HNI clients

Cross-selling to the existing customer base presents a significant opportunity without the need to spend on acquiring customers for verticals like distribution and lending businesses

Client Acquisition Ramp Up Due to:

1.Rolling out of New features

2.Product Improvement

3.Multiple Expiries

4.Buoyant Markets

New Features Introduced to Elevate the User Experience:

1.Launched TradeBuddy, vernacular educational videos.

2.BSE derivatives were launched for its users.

3.Sensibull was made free for all AngelOne users to compete with Zerodha

Some New Developments in the Pipeline:

Open Interest Analytics & Global Indices in the Super App.

More features to help clients with stock discovery

Unique SIPs Registered Trend in the last three quarters:

1st Quarter: 108,000

2nd Quarter: 431,000

Latest Quarter: 725,000

This trend helps in better client retention and engagement in the Super App

These users can be the future potential customers of various products

The top 5 digital brokers constitute 63% of the NSE total active base

This share remains at the highest level, and discount brokers continue to gain market share, with AngelOne leading

While the industry shrunk,AngelOne expanded its market share

Multi-Year Revenue Visibility from Clients Making This an Annuity-Based Model

Revenue has Stabilized from the 3rd Year.

Digital Transformation is Increasing Client Revenue.

There is strong revenue visibility of acquired cohorts for multiple years

The 4th-year revenue contribution has stabilized at 63% compared to 26% in the pre-digital era

Contribution Margin Expansion for Acquired Clients:

Year 1: 56%

Year 2: 92.6%

Year 3: 92%

Enhancement in the Lifetime Value:

- Acquired clients are profitable from Year 1

- From Year 2 onwards, contribution margin is 90%+.

- 3-Year Revenue/Cost of Acquisition is robust at 7.9x

Revenue/CoA will expand further as clients contribute revenue in subsequent years

Gross Client Acquisition at 2.1 million, the highest in the last quarters

90% of the Gross Clients are from Tier 2-3 cities

Rising Share of Revenue from Longer-acquired Clients:

2-3 Years: 7% to 22%

3-5 Years: 9% to 14%

Disc Biased and Invested