Management considering demerger of data centre business? Here is the disclosure.

The demerger of DC is quite interesting and the need of the hour.

Posted Fab Q4 FY26 as well

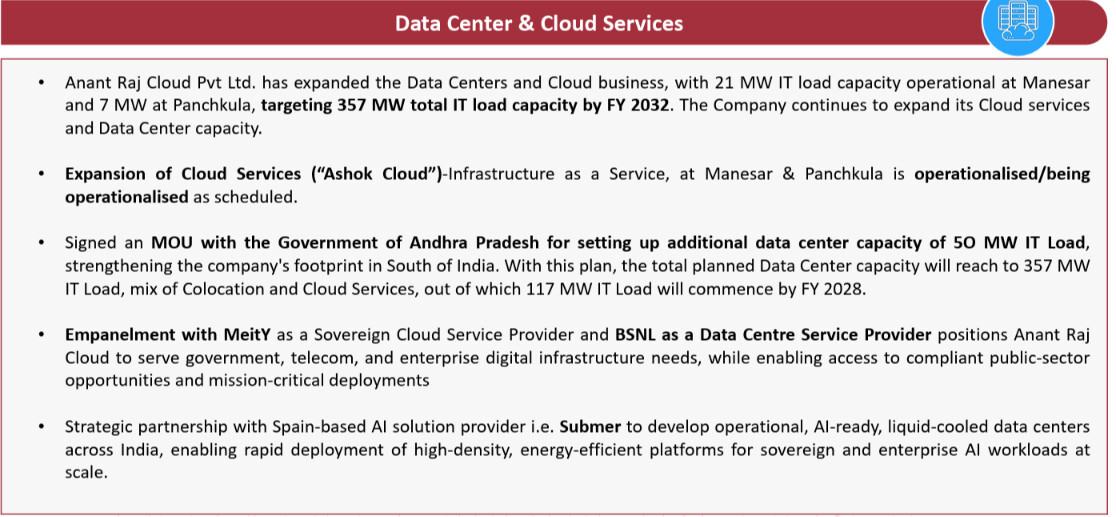

Revenue from Data Center, Infrastructure and Allied services stood at ₹ 176.49 Cr.

3 Likes

They know how to maximize the opportunity of market cap :)

very interesting to watch …they can find good opportunity in data center..better management focus

I dont understand the demerger especially when the datacenter is at such a nacent stage. Wasnt the plan to use real estate income to set up Data centers without taking up debt? In a demerged business, the DC will have to scale up using huge debt as the planned capex is ~20kcr

Source: 2nd page of outcome of board meeting doc.

1 Like

Couldn’t they just transfer the landbank allocated for the data centre expansion to the demerged data centre company?

Its not just the landbank. Datacenter also requires capital for day to day operations and setting up new capacity requires huge capex. I was under the impression all that would be funded by the income from Real estate.

1 Like

100% agreed @Arj_Patel

Either they are gaming investors or they didn’t understand their business properly.

Also I am not happy from the qtrly results, qoq growth is almost null, 30% yoy growth is insufficient to move the stock. Cloud services are still being operationalised since long. Plus they missed out on their 200CR fy26 target. I am damn sure they will again miss 1200cr fy27 target and would be able to do only 600-800 Cr.

1 Like

Yes, it seems counterintuitive to demerge at this early growth phase, but I think it will unlock valuation.

Because Data Centers are valued on EV/EBITDA or capacity multiples, whereas Real Estate is valued on NAV. Demerging allows the market to price the DC business like a tech infrastructure company.

And if Global investors may want to invest specifically in digital infrastructure but have no interest in Indian residential real estate, this could be good for them to bet on Pure Play DC.

(Of course they have better opportunity around world than investing in them.)

Yes, it was the plan; they even got net debt-free in FY26 as per the investor deck. But how will they fund DC capex It is still a question if demerged. The worst thing is we can’t even ask or find answers in a conference call as they do when they want to do it.

@awwwwnuj Are you referring here to the management or people on this thread?

2 Likes

Management. People on this thread and overall valupickr community are pretty good.

4 Likes

A good thing about arc is their newly commenced 15MW colocation was almost fully utilised.

Here is the maths-

28MW → taking out old 6 MW which generates 35Cr → from remaining 22MW taking out 6MW cloud which is still being opertanlised → 16MW colocation remains.

They did 75CR dc revenue subtracting 35CR from 6 MW, 40 CR / 3 / 0.9 = 14.8MW.

So out of new 16MW colocation, 14.8MW was utilised.

I am not interested in their real estate business. Now, with demerger on cards what community members think will be better to do - if it’s good to hold now and sell real estate after demerger or it’s better to sell now and purchase DC later

Ran all my calculations again and this is how at current mcap, you are getting real estate business for free.

Current capacity operational = 28MW

Maximum revenue potential from 28MW = 1220CR

Capacity Utilisation factor = 75%

Revenue at 75% utilisation = 900 CR

Ebitda margins 75% (guided by mgmt plus validated through fy25, fy26 numbers as well)

Ebitda = 675 cr

Avg global EV/EBITDA multiple for DC operators = 22 (source: Avendus report)

I think 30 EV/EBITDA would be possible for Indian market.

So you arrive at 30 x 675=20,250 MCAP

Disc: Biased and invested with 60% PF allocation.

Excellent SOTP Valuations @awwwwnuj

Achieving and sustaining this going forward will require high-quality, long-term anchor tenants. If utilization lags or competitive pricing pressures lower margins, the projected EBITDA will fall significantly, crushing the valuation.

Why the premium for Indian DC companies?

A few things to see from here is:

- cash flow being generated by the operational 28MW.

- Ability to fund their massive capital expenditure plans without diluting shareholders or over-leveraging the balance sheet.

- Quality of their cloud/data partners and the length of their tenant contracts.

- When the Hell they will have regular con-calls?

3 Likes

I feel as per Q3 concall , for 28MW capacity , 24MW will be used for co-locaton and can generate at the max 259 cr ( Rs. 90 lakhs per MW per month) and 4 MW as clound which can generate at the max 48 cr ( 1 cr per MW per month ) so total is Rs. 307 cr max potential. And in Q4/FY 26 they achieved revenue of Rs. 74.51 Cr. so if u annualise this it will come to 298 cr . Further management said they will expand to 63 MW by Dec 26. Also my big concern is they are not doing concalls.

Cloud generates 12cr/MW not 1cr/MW. if you take 4MW cloud, max rev potential comes at 835CR.

I was able to find they have onboarded one of the prominent govt ministry NIC and an edtech company which probably is Classplus as far as I think (Mukul Rustagi is the only edtech founder who follows them on linkedin). This info is not rock solid, only speculation.

Yes, you are correct; I read it wrong.

But we need to keep in mind - AI Cloud

| Item | Approx |

|---|---|

| Capex/MW | ₹250 crore |

| Revenue/MW | ₹150 crore/year |

| EBITDA margin | 60% |

| Asset life | 3–5 years for GPUs |

Much higher return potential,

but much higher obsolescence risk.

They are not purchasing GPUs. They will provide colocation for GPUs, that’s where submer partnership kick in imo.