Anand Rathi Wealth Ltd is a prominent player in the financial services sector, boasting a rich legacy spanning over two decades. Founded on principles of integrity and innovation, the company has established itself as a trusted name in wealth management and investment banking.

With over 20 years of experience , Anand Rathi Wealth Ltd has earned a reputation for reliability. The company offers a comprehensive suite of financial services, including wealth management, investment banking, and advisory services.

Business of Anand Rathi Wealth

They are a leading non-bank wealth solutions firm in India, being ranked amongst the top three non-bank mutual fund distributors in the country. The company offers a wide product portfolio of wealth solutions, financial product distribution, and technology solutions to its clients.

Business Vertical

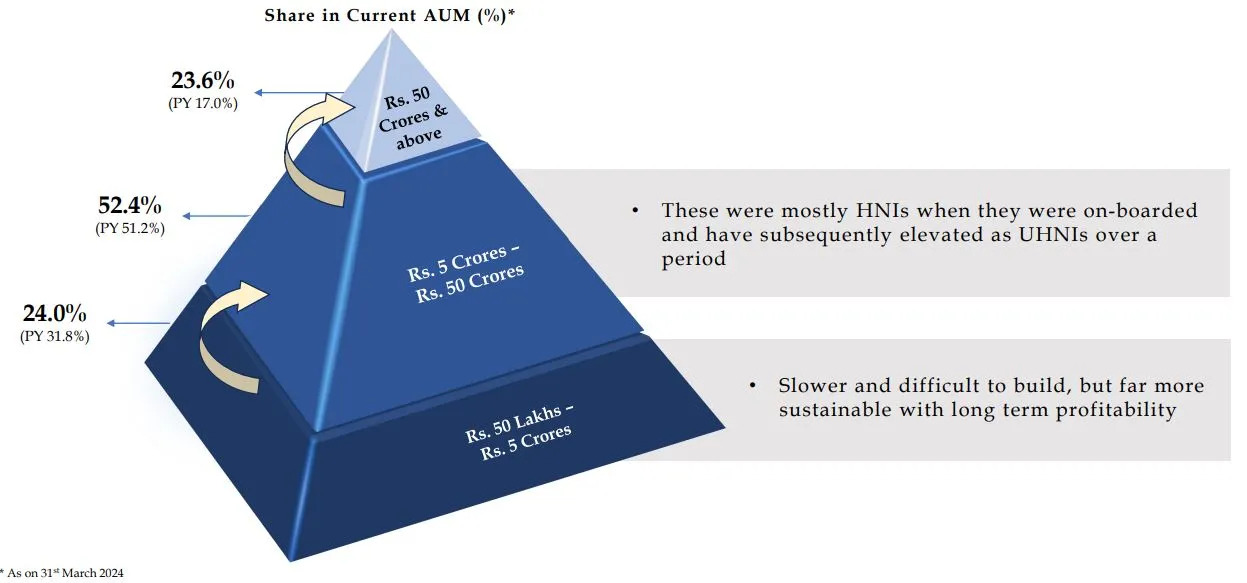

Private Wealth Segment

This is the main vertical of the business. In this segment, the company caters to the HNI and UHNI (5 to 50 Crs).

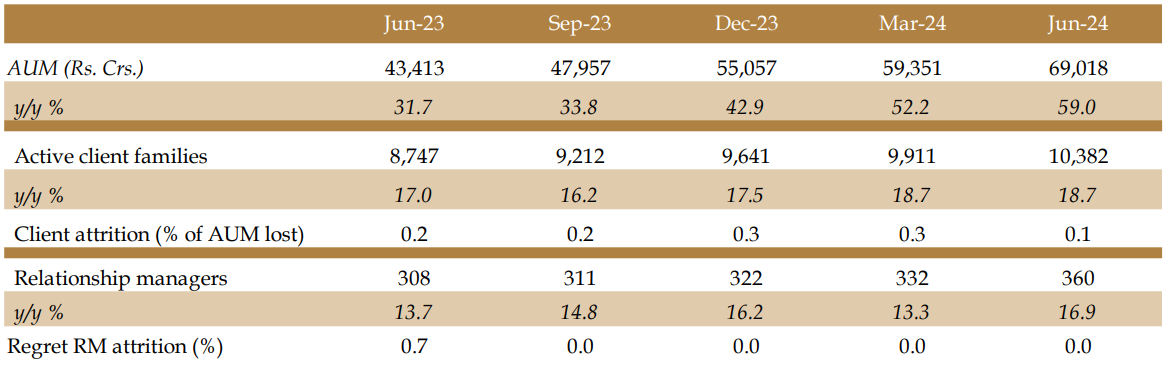

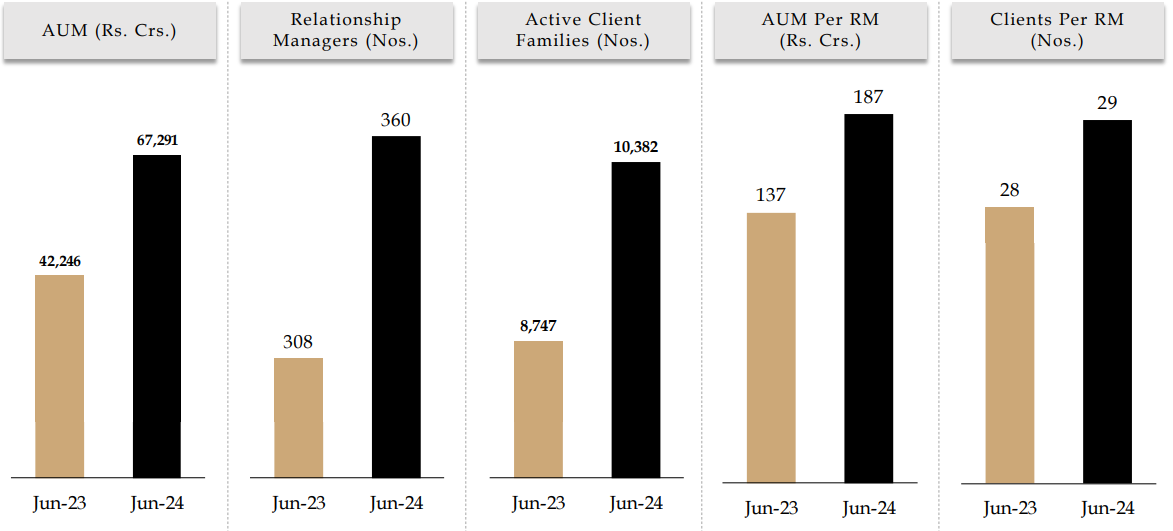

As of FY24 this Private wealth vertical

- AUM stood at Rs. 57,807 Crores.

- It caters to 9,911 active client families.

- Serviced by a team of 332 Relationship Managers.

**As of FY24, 60% of their clients have been associated with them for over 3 years , representing 79% of total PW AUM, which shows ARWL’s strength in vintage of both clients and their AUM.

Digital Wealth Segment

This segment is a fin-tech extension of their proposition , to address the large mass affluent segment of the market with wealth solutions delivered through a ‘phygital channel’.

Customer Segment : Mass Affluent having existing financial assets: Rs. 10 lakhs – Rs. 5 crores

They have a unique approach to wealth solutions -

- They deliver service through a ‘phygital channel’ i.e., a combination of human distributor (physical) empowered with technology (digital)

- They seek to build a scalable and profitable model by using this blend of technology capabilities and human interface.

- Also, attempts to build a partner led distribution through whom a packaged investment solution is delivered.

**As of FY24, It has an AUM of 1545 Crs and 4862 clients.

Omni Financial Advisor

This is the company’s strategic expansion for capturing the wealth management environment, which leverages technology to cater to the retail segment through a B2B2C model.

They also provide a technology platform to the Mutual Fund Distributors (MFDs) and to their clients. This is their target segment.

Why is this an advantage for OFA segment?

- Small MFDs lack infrastructure and technology, so they provide them a Mobile led Tech - Infrastructure.

- MFDs have Poor Client Engagement – Sell & Move on model, which OFA provides them with Client Reporting, Transaction & Engagement as a solution.

- MFDs majorly struggle with Client Acquisition & Client Retention, here OFA provides Pre Sales – Sales – Post Sales enablers.

****** As of FY24, this segment comprises 5,994 mutual fund distributors . This segment handles 20.6 lakh clients.

Lets talk about Growth Drivers in this Business

Major evolution that we notice happening in the country can be linked to this -

- Rising mutual fund penetration in India.

- Increasing affluent population & household income. (People are getting richer)

- MF assets are expected to grow from Rs. 39 lakh crores (Mar 2023) to Rs. 455 lakh crores by Mar 2027.

- Ultra HNI population projected to grow at 15.7% CAGR between 2022-27

- Well-poised with diversified model, tech focus & strong industry tailwinds (Positive factor)

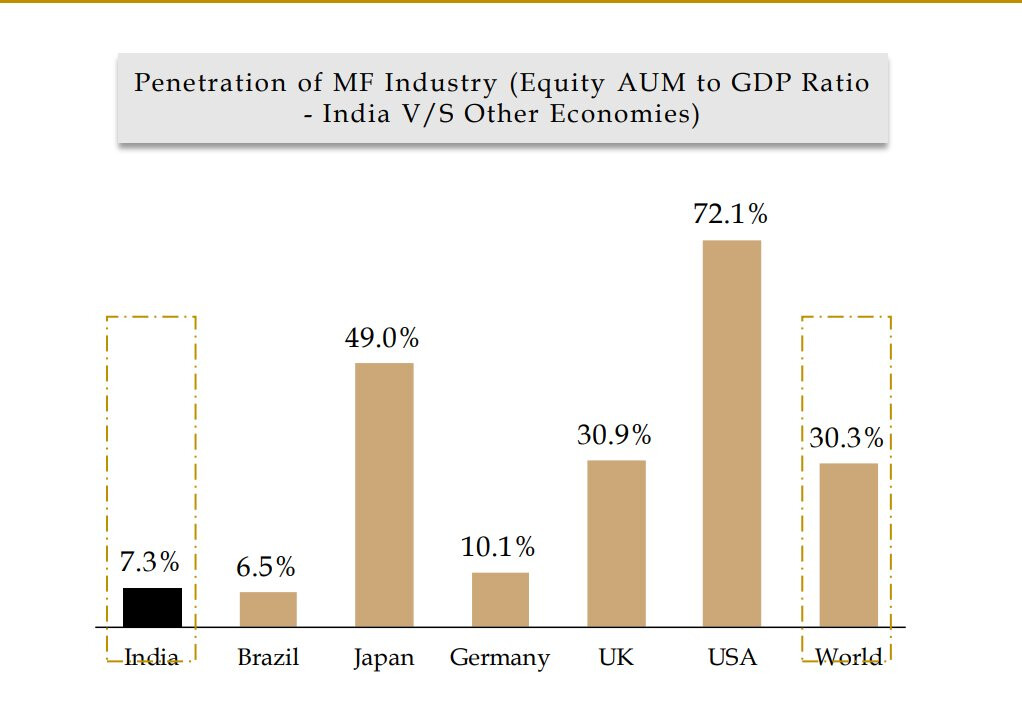

India has a huge scope of penetration towards professionally managed financial assets like mutual funds when compared to the global average, which is 4x of India.

This creates more opportunity for wealth management industry.

Financial analysis of the company

Anant Rathi has no surprise here. Yet again tremendous fast growing financials.

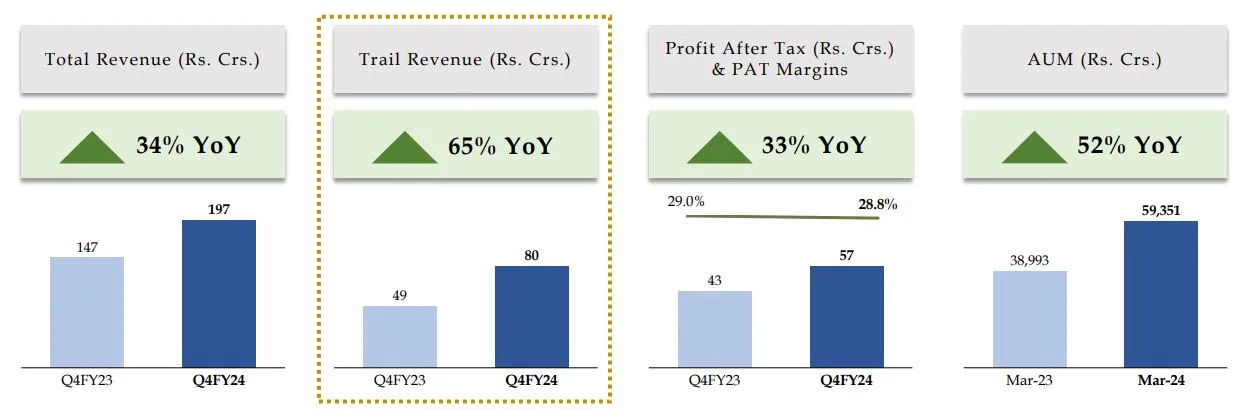

Here are the Q4 FY24 Financial performance :

- Company is sitting at highest ever sales and highest ever profits at an OPM of 44%.

- Last 1 year company has given a return of 330%.

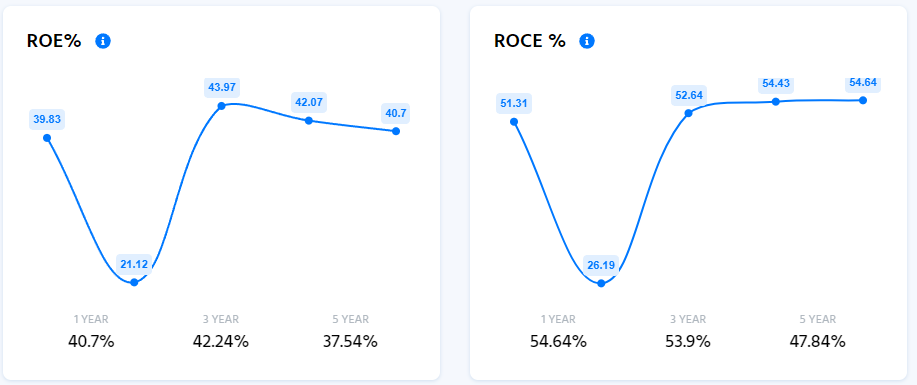

- ROCE & ROE: 48% and 38%.

Great news by company

The company boasts a final dividend of Rs. 9 per Equity Share of Face Value of Rs. 5 each of the Company (180% of FV)

Not just that but also approved a proposal to buyback upto 3,70,000 Equity Shares at Rs. 4,450 per equity share representing 0.88% of the total shareholding.

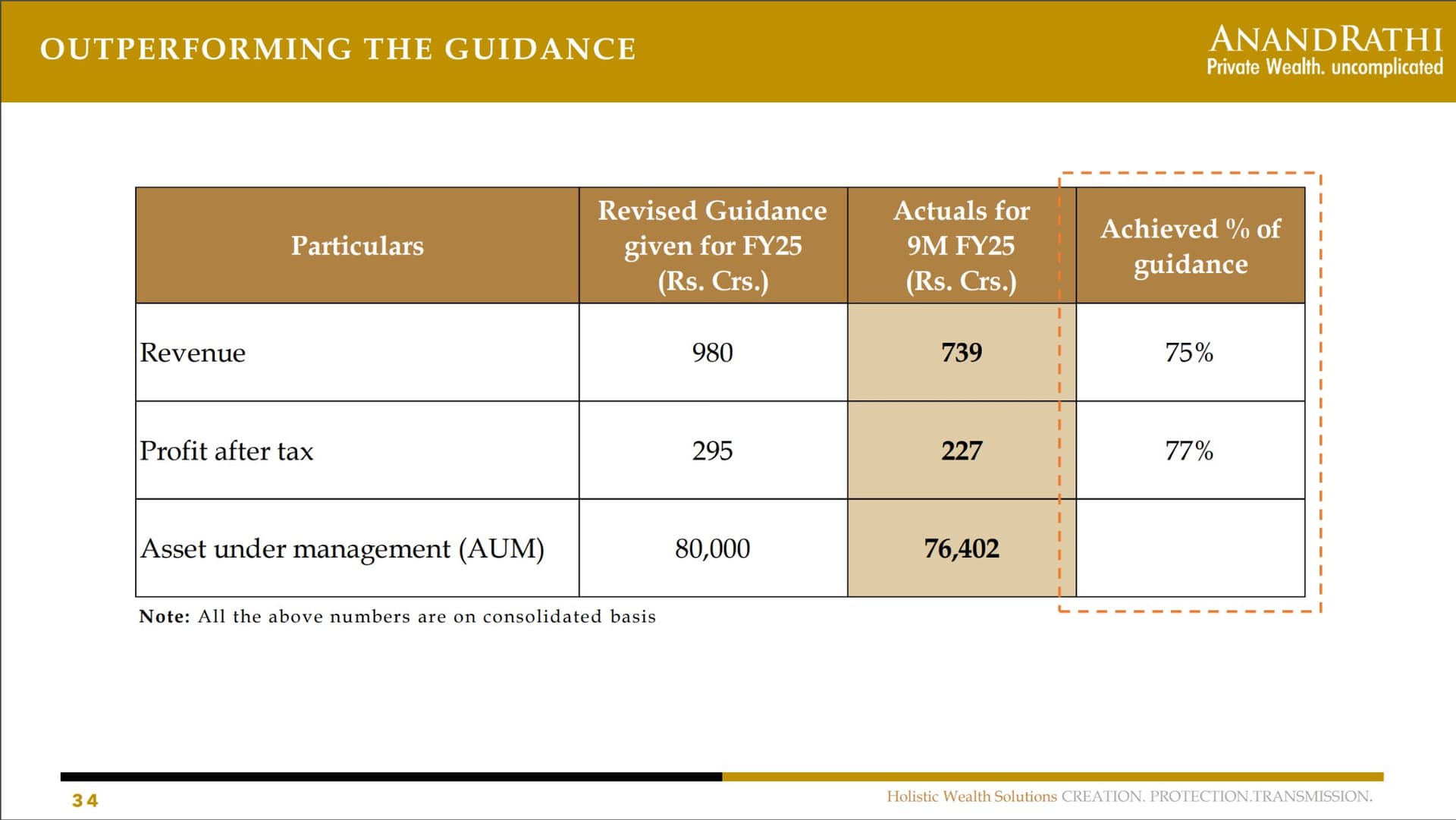

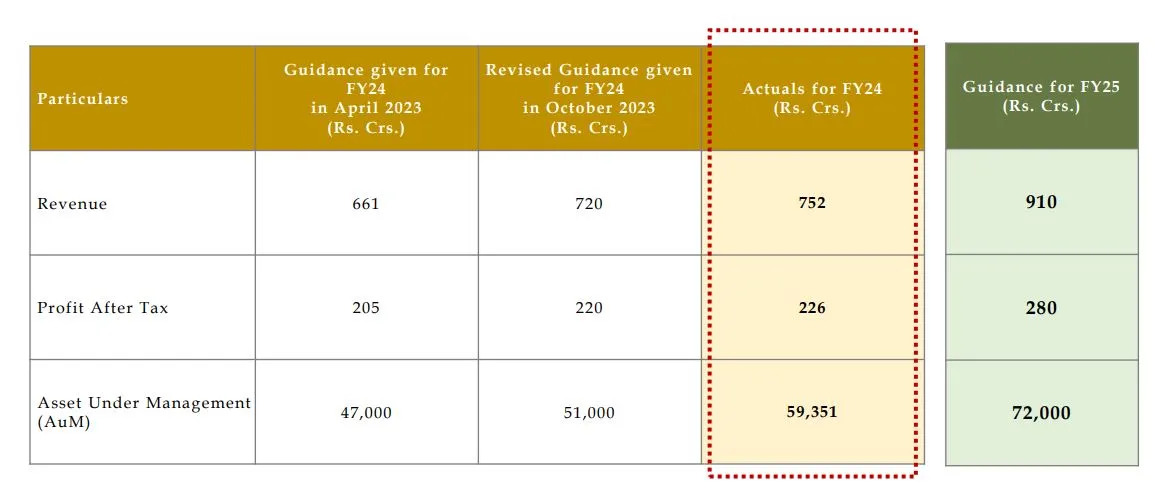

Guidance given for FY25

They have outperformed the FY24 guidance. Which is brilliant.

Now if they manage to hit 280Cr PAT for FY25 then their EPS would jump to the north of Rs 67 a share. After buyback it might even go till 70 EPS.

Now let’s do some interesting calculation.

How did I get to that EPS?

EPS = PAT/ Total outstanding shares ![]() EPS = 280/4.18 = Rs 67

EPS = 280/4.18 = Rs 67

Total Outstanding Shares = Market Cap/ Stock Price ![]() Outstanding shares = 17447/4171 = Approx. 4.18

Outstanding shares = 17447/4171 = Approx. 4.18

How to get to the stock price valuation?

Now, The current PE is around 77 (which is high) and EPS is Rs 67.

The stock price should hit = PE*EPS = Rs 5,150

Current Market Price - Rs 4171.2

With some realistic PE contraction it should give about 7-10% from here.

Conclusion

In my view, Anant Rathi Wealth is a cash-cow and AUM kind of business with very high margins.

The Asset Management Company sectors itself are under-valued and have great potential for growth.

They generate healthy cashflows and even if they are stalling or not much growth, the money they generate is free cashflow.

The only concern is the PE ratio which is 77 but other than this everything looks great.

The company is run by able and proven management and exhibiting accelerated growth.

Finally, as long as they are making the rich get richer. The company will thrive.

Disc : Invested.