INTRODUCTION

We all know that a buy and hold (aka: shut up & wait/buy & forget) strategy has worked for investors investing in INDEX FUNDS in the US equity markets. But how has this approach fared for domestic Indian investors in an Indian INDEX? To answer this question I have analysed returns of an Indian index investor over the past 20 years ACROSS VARIOUS ROLLING TIME PERIODS.

In addition to analysing whether index fund investing has worked, I have also tried to analyse whether index funds have beaten Fixed Deposits, what is the ideal holding period for an index fund, how are the returns been for SIP investors, etc

METHODOLOGY

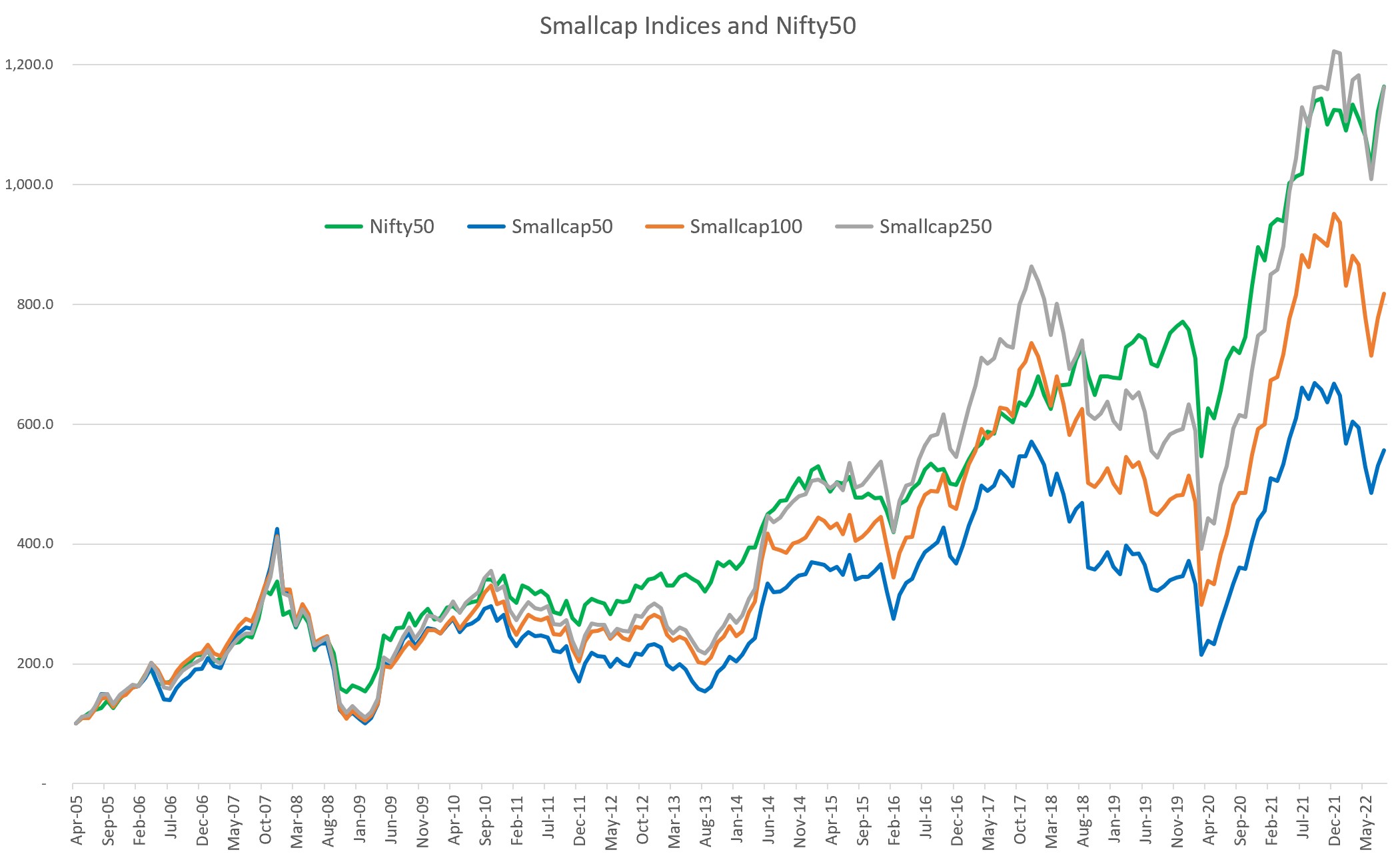

To analyse the returns for Indian Index investors, the first thing to decide is which index to use. I chose the most popular index – the NIFTY 50. However, if we just the Nifty it would understate the actual returns as it does not consider the returns arising from dividends. To get a true & complete picture of returns, the dividends received also need to be factored in. This is where the Nifty TRI (Total Return Index) comes to our aid as it provides the return including the dividends. NSE provides historical data for the Nifty TRI from June 1999 onwards on its website.

The second question to decide is the timeframe. I have come across several misleading posts/write-ups/brochures, etc where people cherry pick the starting and ending date of their analysis to make their point. In order to address this issue I have taken every month from January 2000 until July 2021 and provided returns for every possible rolling One year period, Three year period, Five year period, Seven year period, and Ten year period.

For e.g. January 2000 to January 2001 is the first one year period, February 2000 to February 2001 is the next one year period…………July 2020 to July 2021 is the last one year period. The same thing has been done for the other time periods as well. Consequently, we get 247 One year periods, 223 Three year periods, 199 Five year periods 175 Seven year periods, 139 Ten year periods.

The next question to decide is the method of investment: whether a lump sum investment or whether a Systematic Investment Plan (SIP). To get a comprehensive view, I have calculated the returns for all periods for both methods of investments. For the SIP calculation, I have assumed that a SIP investor will make a fixed investment ONCE every month (on the last trading day of the month) and shall continue to do it for the entire time period without fail. It is important to note that even a monthly SIP can be broken into many smaller investments over the course of month (instead of one large investment at the end of month) but I have not considered the effect of this complication (yet).

Now that we have the returns for the 1/3/5/7/10 year periods, we can run the usual descriptive statistics on them. However to make it more intuitive & visual I have also plotted the returns for each period on a histogram that has the same scale and same bucket size so as to make comparison easy.

Thereafter, I compared the Nifty TRI returns with the Fixed Deposit (FD) rates prevailing exactly at that time period and calculated the excess return over the FD for all the aforesaid time periods. The data regarding the FD rates is taken from the RBI website

NOTE: You may ask why January 2000 and why not earlier. The reason for this is that NSE website provides data for the Nifty TRI only from June 1999 onwards and consequently only from January 2000 onwards we get data for the entire calendar year. If someone knows of any reputed data source providing NIFTY TRI data earlier than June 1999, then please do let me know and also provide me with the data ![]()

AN IMPORTANT FACTOR TO KEEP IN MIND

Before talking about the results, one must keep in mind that the Nifty has shown a secular growth trend in the past 20 years (you can see it here). While there have been some years of flat/negative returns, our market is yet to see a LARGE time period (say a decade or more) of flat/negative returns. Hence, in the past 20 years, if you remained invested in the Index for longer time periods of 7 years & more you have ALWAYS got positive returns and that too greater than 5% even if you invested in the worst periods. No wonder that the mutual fund industry always tells that investing for longer periods yields good returns and treats the same as gospel truth.

However, this has not been necessary true for all indices even in the case of growing countries. For e.g. If you see the Shanghai Composite Index, it is around the same level today as it was in July 2009 and AT THE INDEX LEVEL there have been no returns. Now of course if we include dividends & buyback then the returns will be better but then if we invested in such a period then, intuitively, our returns are almost bond like as they are restricted merely to dividends/buybacks. If I manage to find the time, I shall try to do a more detailed study of returns for such markets in a follow up post.

Hence, in case we extrapolate the results given below into the future we must remember that we are implicitly also stating that the future will continue to remain like the past. While that may be the case it may not necessarily be true. Also the returns must be viewed in the context of prevailing inflation. With this in mind let us see the results below

ANALYSIS OF RETURNS OF INVESTMENT DONE THROUGH SIP

-

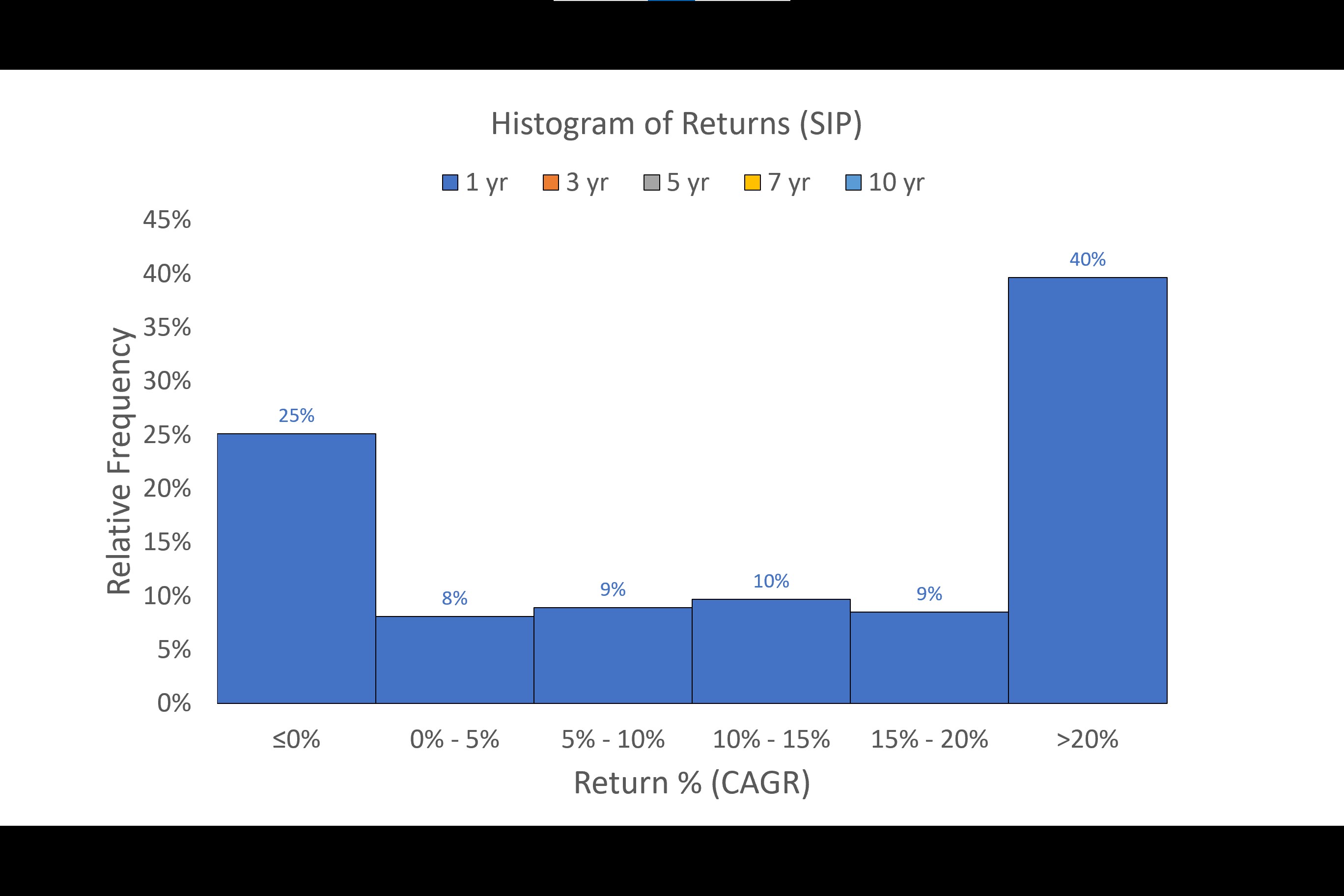

One Year Period: As expected, the returns from one year periods were very volatile as seen from the wide range (max-min) and high standard deviation. Importantly, in 25% of the time we lost money and 1/3 of the time our returns were below 5%. The data seems to be normally distributed (though this is not evident in the above histogram due to the way I have made my buckets)

-

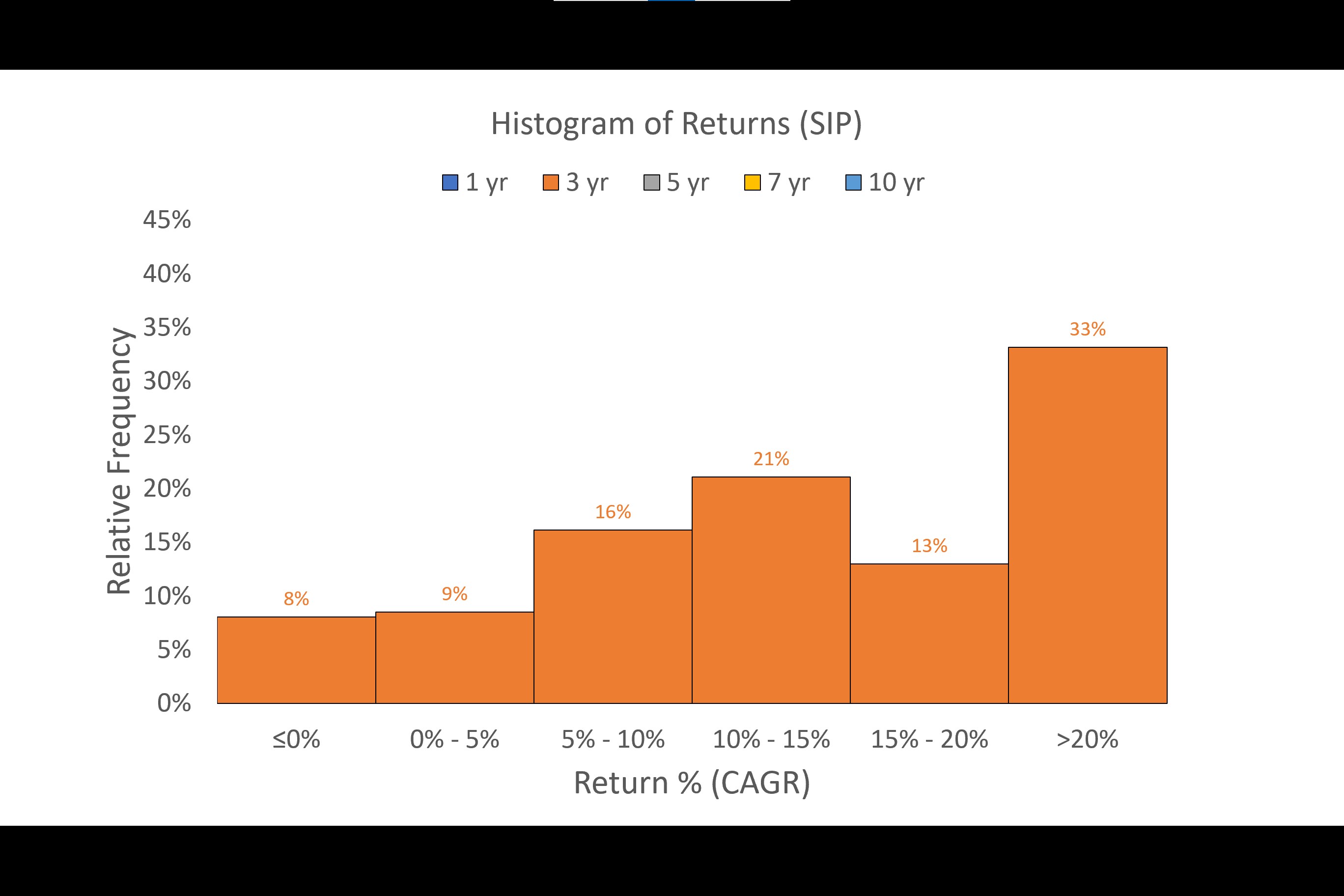

Three Year Period: The 3 year returns were much less volatile and range & standard deviation drop significantly. We lost money only in 8% of the time (as compared to 25% in the one year period). The data is moderately skewed to the right

-

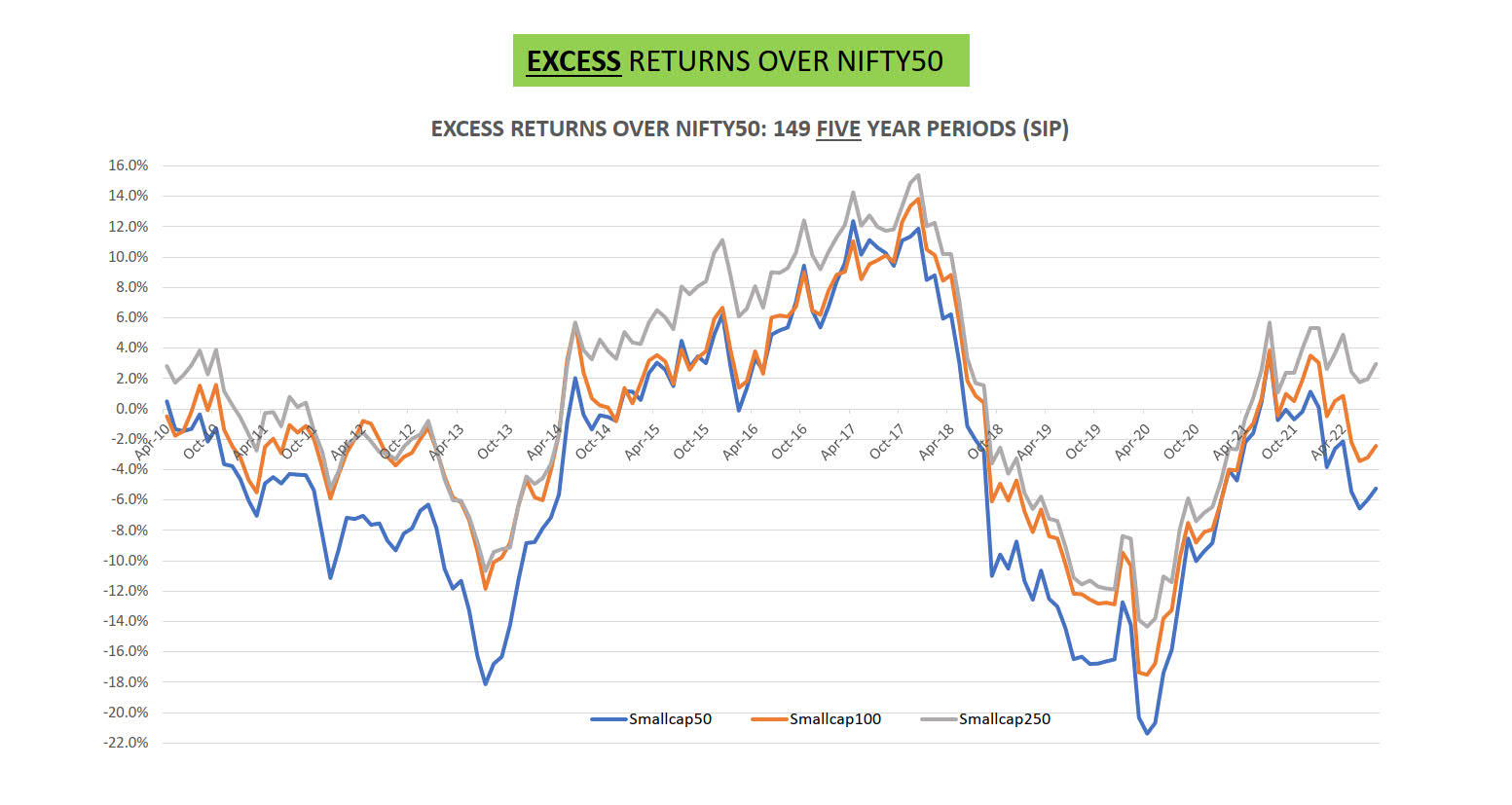

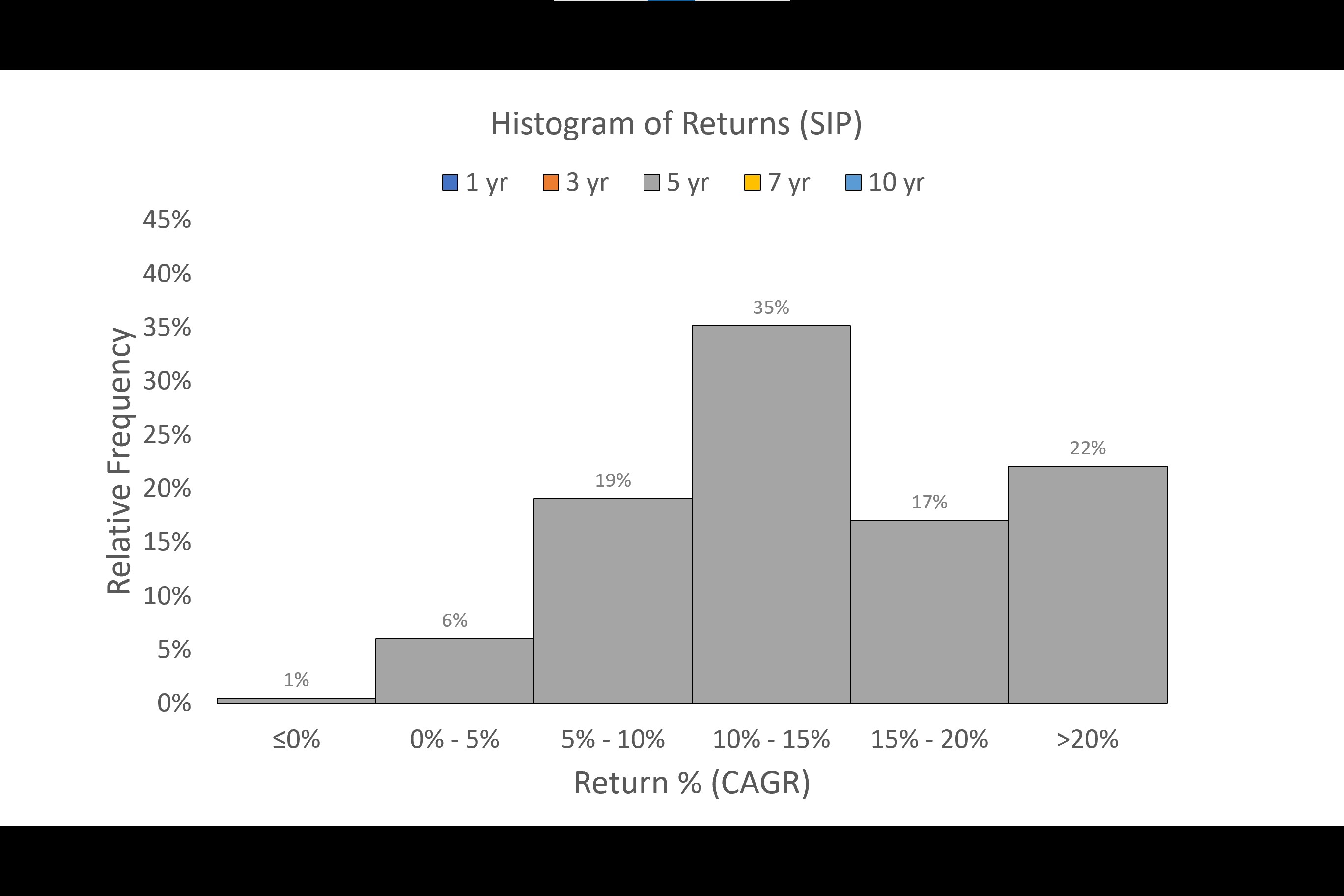

Five Year Period: The volatility further reduces in the 5 year period. Also we did not lose money in any of the periods. Furthermore in 54% of the time our returns were in 5%-15% range. The data is heavily positively skewed

-

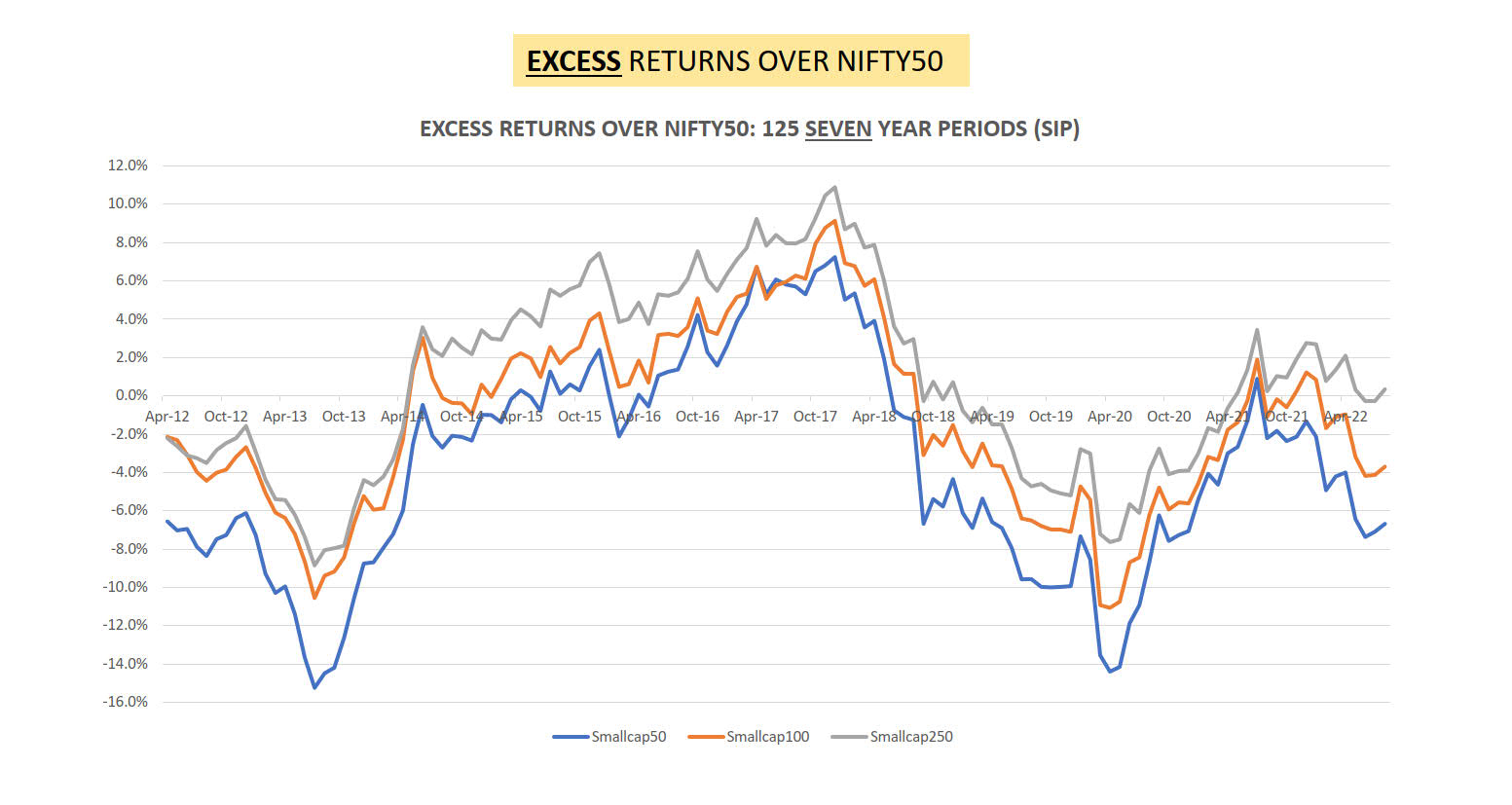

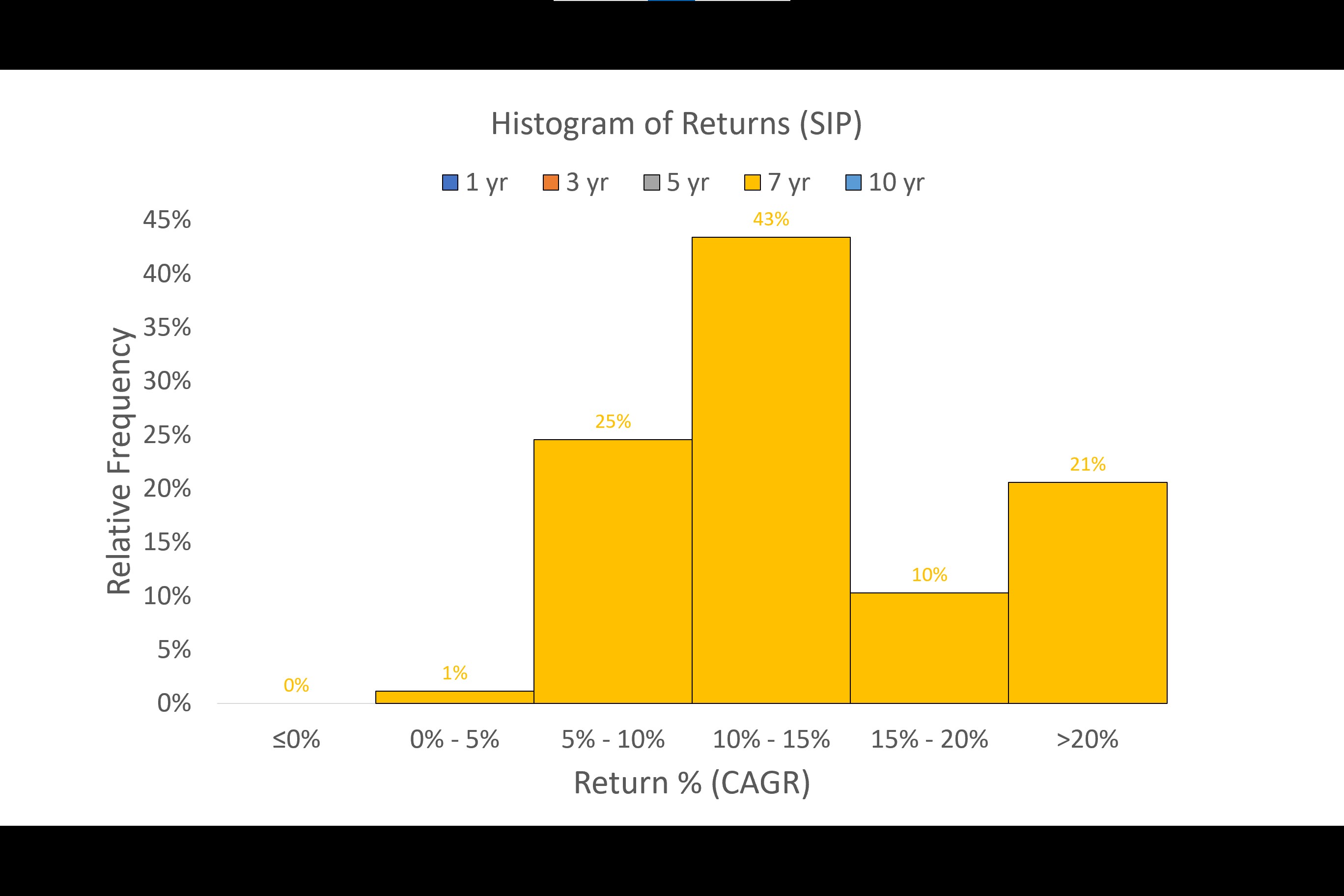

Seven Year Period: From this period onwards the results start getting interesting. The volatility continues to narrow and the dispersion of the returns is closer to the average. Not only there is no loss of money, but also the returns in virtually all periods were above 5%. Furthermore 74% of the time our returns were above 10%. The data is heavily positively skewed and with high peaks

-

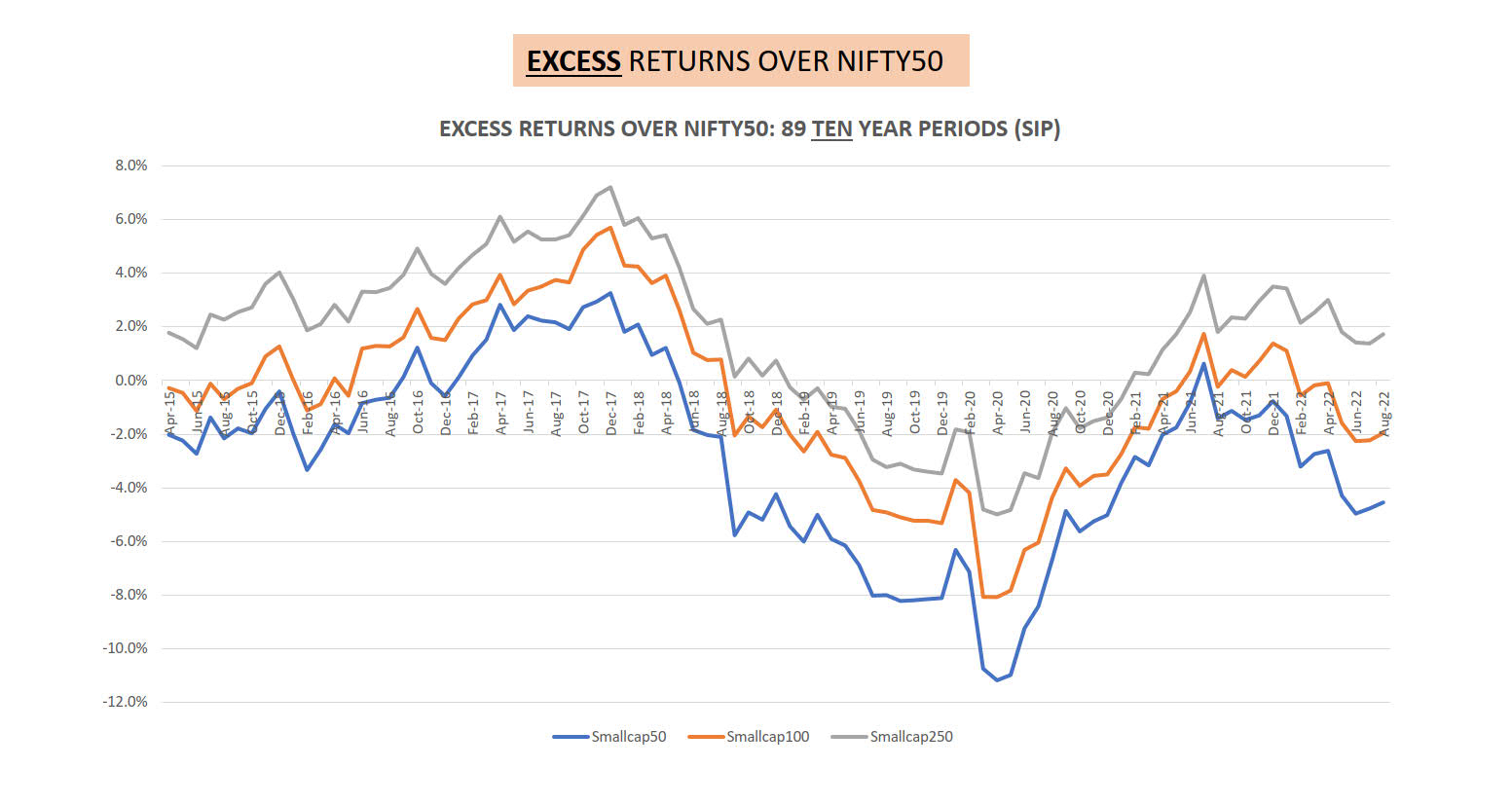

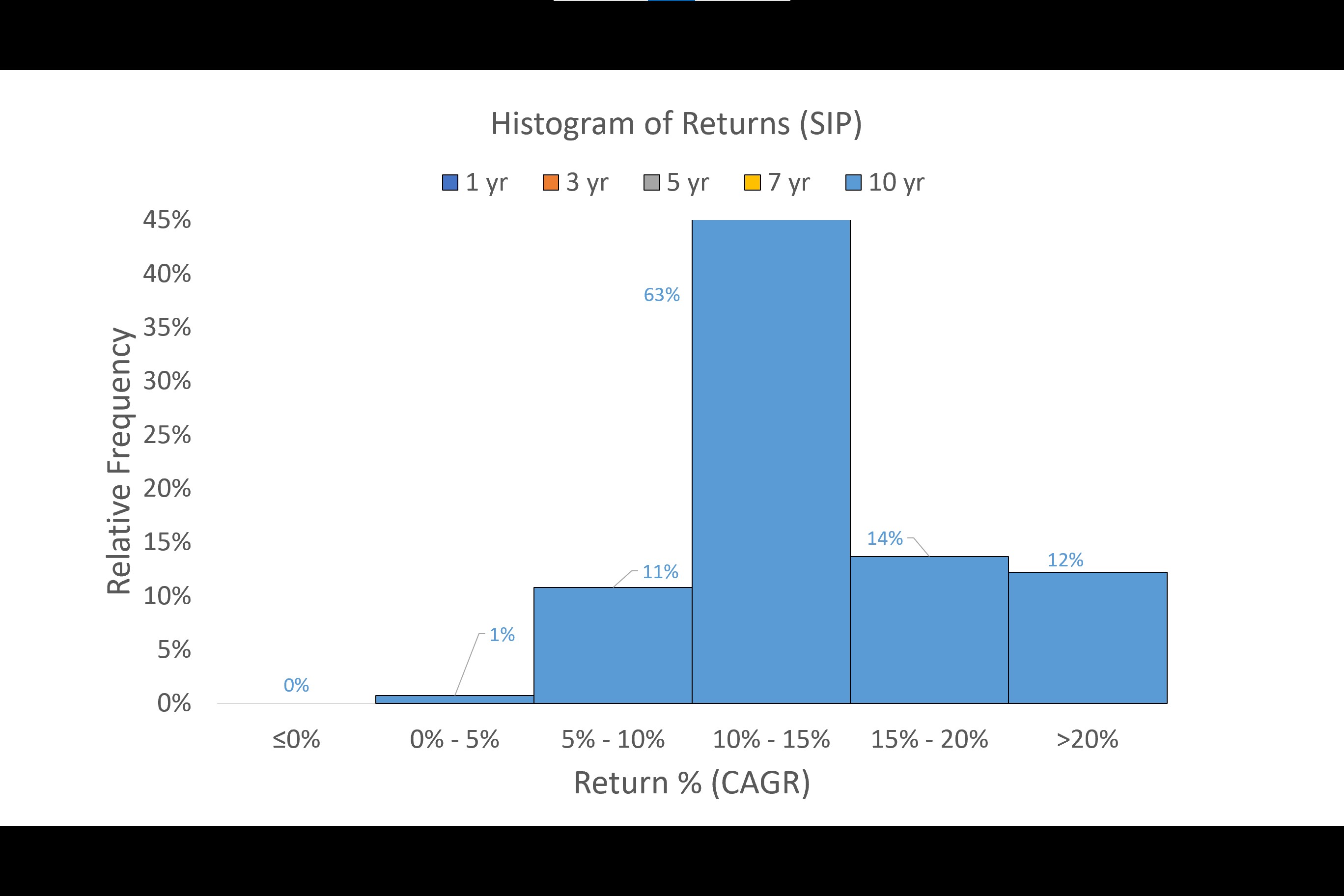

Ten Year Period: The results continue to get better and a staggering 89% of the times, the returns were above 10%. However the returns>20% were only 12% of the time compared to 21% of the time in the 7 year period. NOTE: y-axis has been topped at 45% despite the fact that there is a data point above that number because I wanted to maintain comparison with charts of other time periods

ANALYSIS OF RETURNS OF INVESTMENT DONE THROUGH LUMPSUM

I have done an analysis of even the lumpsum investment and the detailed images for the same are on my blog post. Not posting it here as this write up already has too many images ![]()

However, the key takeways are:

*The results of even a lumpsum investment across the 1/3/5 year time periods mirrors the basic pattern seen in the SIP histograms. However the 7 and 10 year periods are different.

- The 7 year lumpsum return has a lesser range of 24% vis-a-vis 38% in the SIP return and thus the dispersion of returns is much lesser. This can also evident from the negative kurtosis of the lumpsum return vis-a-vis the positive kurtosis of the SIP return. A negative kurtosis typically means lesser data at the tails as compared to a normal distribution

- While the 10 year lumpsum return shows the same average, standard deviation and range as that of the SIP return, it has a significantly different distribution. As evident from the high negative kurtosis, the data shows a kind of uniform distribution which is very different then that of the SIP. It shows that 40% of the time the returns were in the 15-20% bucket as opposed to only 14% in the SIP. But 22% of the times, your returns could also be in the 5%-10% bucket as compared to only 11% in the SIP.

OUTPERFORMANCE OF LUMPSUM INVESTMENT OVER A FIXED DEPOSIT

As seen above, the times when the Index outperformed the Fixed Deposit improved significantly from the Year 7 onwards

CONCLUSION

If you want only one single takeaway from all of the above (with the caveat that the future would be similar to the past as stated earlier) then it is this: The ideal time frame for investment in an index is 7 years and above as not only did you not lose any money but also managed to get a return>5% in ALL of the periods. Furthermore, also remember how a return is calculated: it assumes that you WILL exit after your timeframe is over even if the market is pessimistic at that point of time. However, if you are not in need of any funds but are willing to wait till the tide turns (and even assuming that you don’t invest further money) then your returns could improve and more so in the case of an SIP where your exit matters more than the entry

If you want to print the results and wish to share them I have made a handy PDF for you to download from my blog. I would love to hear your critique on my process as well as your take on the results through comments / twitter.

There are many follow through analysis that can be done and if I get the time to do it I will post it here.