Symbol: 506248

Listed exchange: BSE

Sector and industry: Chemicals

Market Cap.: ₹ 206.88 Cr

Current Price: ₹ 37.60

Book Value: ₹ 10.36

Stock P/E: 15.88

Dividend Yield: 0.53%

Face Value: ₹ 2.00

Promoter holding: 73.16%

BUSINESS DESCRIPTION

Amines & Plasticizers Limited (APL), incorporated in the year 1973 as a Public Limited Company, registered under the Indian Companies Act of 1956, having its Corporate Office in Mumbai, India and manufacturing facilities in Navi Mumbai, is the pioneer and one of the largest producers of Ethanolamines, Alkyl Alkanolamines, Morpholine Derivatives like NMMO 50% & Gas Treating Solvents in India.

Company’s products are well accepted in overseas market and exporting about 50 % of its total production. Company is the market leader of Ethanol amines and Alkyl Alkanolamines in India with a market share of 75 %.APL is also the world’s largest producer of N-Methyl Morpholine Oxide ( NMMO). The technology for producing NMMO is indigenously developed by company’s own R&D wing.

APL has also now diversified its activities into producing various Specialty Ethoxylates and Propoxylates, Block polymers and Co-Polymers of EO and PO besides Fatty Alcohol Ethoxylates and Propoxylates, PPG’s (of various molecular weights like 425, 900, 1020, 2000 & 4000), Cement Grinding Aids, TIPA 85%, DEIPA 85%, Phenoxyethanol of High Purity and Oil field Chemicals such as H2S scavengers, Demulsifiers, Acid Corrosion Inhibitors, Flow improvers / Pour point Depressants for Crude oil as well as Lube oil, Bactericides, Emulsifiers & Mud Surfactant, Dispersant for Oil spills etc. http://amines.com/corporate-profile.html

As a novice investor, Prima facie looks like a very good long term growth opportunity, inviting useful insights or feedback from Senior VP and other fellow members.

Amines & Plasticizers has been growing at a steady pace for the last few years. It manufactures organic chemicals used in Petrochemical & oil refineries, Gas Plants and Textiles. This R & D based Co. has developed its own Pipe Leak detection software which could potentially change the fortunes of the Co. going forward.

The Co. has been steadily increasing exports in a bid to improve margins. The Co. enjoys healthy return ratios. High promoter holdings in excess of 73% also inspires confidence.

Attaching the link to the latest AR for a better understanding of the working of the Co.

Doesn’t seem like a stock with a lot of liquidity, I cannot find any major trades done recently. Please correct me if I am wrong, but this looks like Apis India, that stock also looked good on paper, but did not have much depth.

APL seemed like a good company (few pointers on what I like about it at the end) to begin with however a further look into historical numbers and annual reports raises some questions on sustainable quality of the business. Laying out my questions/comments here -

Cash flow generation has been poor over last decade (cumulative CFO/PAT is 0.4x)

Looks like high dependence on oil & gas sector (I could be wrong here since management does not provide industry wise sales mix but reading through last 10 annual reports that is the impression i got) which is very cyclical in nature. So we should be well aware that it is more of a cyclical story than secular growth story. And future outlook of oil & gas industry is very difficult to predict. This cyclical aspect is also visible through return on capital/net worth profile of business over last decade.

Last ten years history of gross margins (21% - 37%) indicates that there is less pricing power. Clients are able to get better pricing terms either because of consolidation at their end (less number of total buyers in industry) or may be there is high competition. Companies such as Dharamsi Morarji, Alkyl Amines and NGL give more comfort on this parameter.

Things which are interesting about APL -

Management’s focus on new chemicals to enhance their market opportunity is very commendable. Almost every year they come up with some thing new that too across industries.

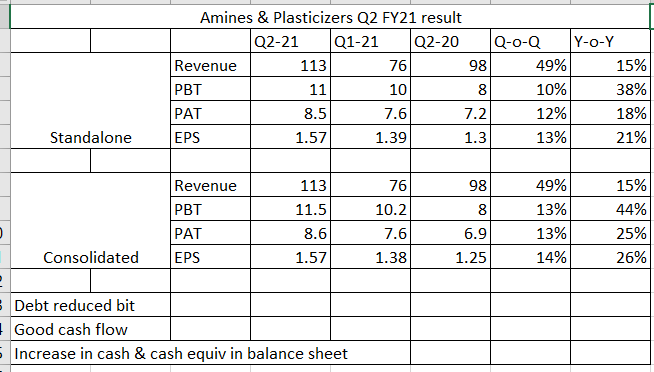

Historically company had heavy debt but the same has changed since FY17. Debt ratios improved meaningfully only over last 2.5 years; an unlevered balance sheet provides more headroom to grow in case opportunities arise

market leadership and long term relationship with key clients

Would love to have counter views on the points above.

Anyone tracking this company now? The price performance has been quite strong. Given, that the company has large exposure to Oil & Gas Industry, is it fair to extrapolate the optimism towards the specialty chemicals industry to this one. Having said that…these are not easy numbers for even the best of the companies to exhibit.

Is anyone tracking this company now? I have done some analysis & below are my findings. The stock seems to be undervalued at current price and looking at the financials

Sales growth-

5yr CAGR- 9%

10yr CAGR - 8%

Operating profit-

5yr CAGR- 12%

10yr CAGR- 15%

PAT-

5yr CAGR- 23%

10yr CAGR- 29%

CFO-

5yr CAGR- 17%

10yr CAGR- 12%

EPS growth-

5yr - 22%

10yr- 30%

5yr & 10yr cumulative PAT & CFO-

5Yr 10yr

PAT 80 95

CFO 87 132

CFO/PAT 109% 139%

All figures looks good except the cash flow is fluctuating every alternate years. Also the receivable days has increased in past 2 yrs to around 63 days from earlier 50-55 days.

There is not much information available regarding the promoters of the company however from the annual report I have noticed that the MD is part of both Audit committee & remuneration committee which is a negative sign.

I have some confusion regarding the products that they manufactures whether it’s same as what is manufactured by Alkyl amines or Balaji amines or it is different. From the annual report, it seems like their products are majorly used in oil & gas industry and not in pharma industry. Anyone with technical expertise kindly clarify.

Regards,

Udipta

This type of Amine used in Natural Gas processing industry in Dryer for dehydration process. Largest supplier to domestic Gas processing industry and few pharma company…

The operating margin has come down to 12% in current quarter from 17% in previous quarter due to increase in RM cost. Also other expenses has gone up significantly- could not find out the reason since there is no concall happens for this company.

In last quater there was significant contribution from Hydroxy choloroquine (HCQ) supplies while the normal MDEA and Nmma business was weak due to global lockdown. HCQ requirements have come down and other two key products are used as gas sweeteners and in textile processing.

Now that business is picking up and also capacity expansion will play out. Hopefully business will do more better.

They have unique products and strong R&D. Globally they compete with Huntsman and BASF.

They supplied ingredient for manufacturing of Hydroxy chloroquine.

This is the USP of the company. Since they are multi product speciality chemical company, They can manouvere their products according to the market demand.

Their key products find application in Natural gas industry (gas sweetner) and textile industry.

The company has announced that they are “Investing in a Company (26% Equity upto Rs. One Crore) involved in production of Solar energy and entering into a Power Purchase Agreement with them to procure power at discounted rate”