JM_Financial_Initiating_Coverage_on_Ami_Organics_with_29%_UPSIDE.pdf (2.7 MB)

3 Likes

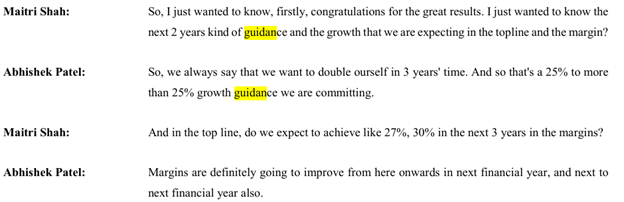

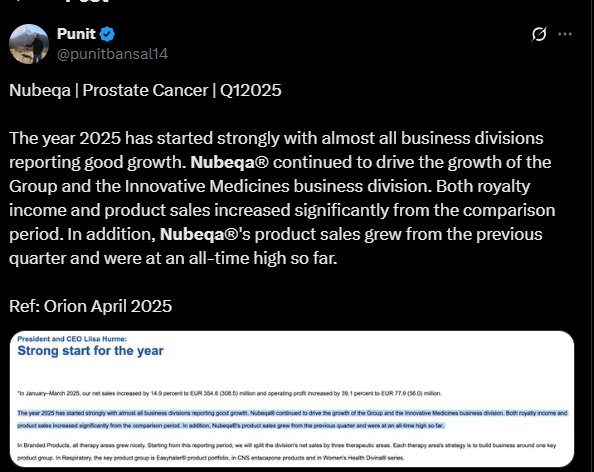

AMI Organics | Management Guidance

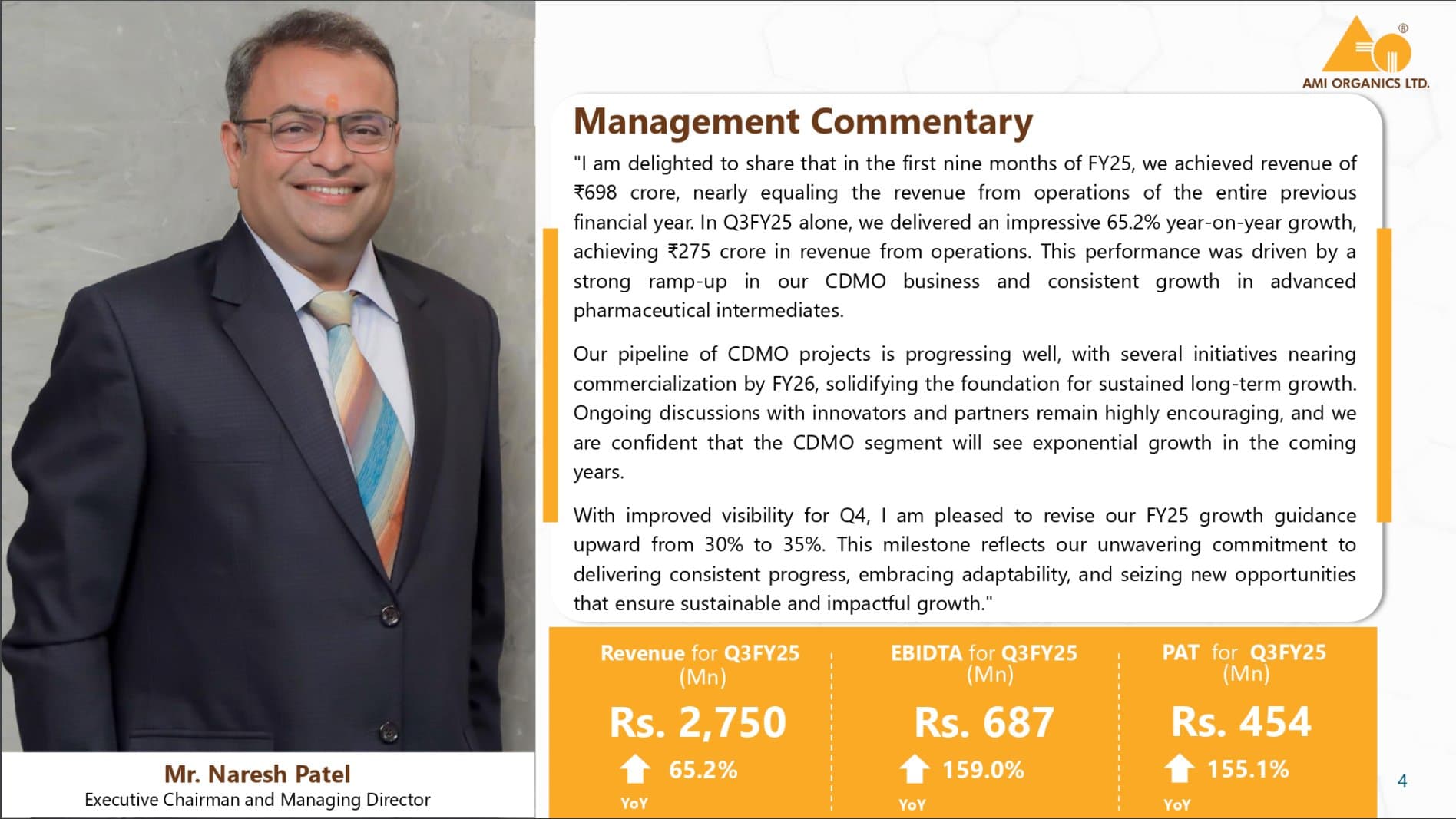

Results Update

Strong Growth in Q3FY25:

Revenue: ₹2,750 Mn (+65.2% YoY)

EBITDA: ₹687 Mn (+159% YoY)

PAT: ₹454 Mn (+155.1% YoY)

CDMO Business Expansion:

a. Significant ramp-up in the Contract Development & Manufacturing (CDMO) segment.

b. Several CDMO projects progressing toward commercialization by FY26.

c. Positive discussions with innovators & partners for future growth.

Revised FY25 Growth Guidance:

Growth guidance revised upward from 30% to 35% due to strong Q3 performance

9 Likes

This telegram channel.

2 Likes

Guidance & Management Insights from Q3 Earnings Concall

- CDMO business to grow from INR 80–90 crore to 1,000 crore by FY28

- Growth guidance was revised upward from 30% to 35% for FY25

- EBITDA margins are expected to reach 27%-30% with operational leverage in upcoming years

- The company aims to double its size in the next three years

- FY26 is expected to have the highest-ever margin for Ami Organics

- Management is confident about business sustainability till 2040

- No plans to enter peptides, staying focused on synthetic chemistry

- Battery chemicals: 4,000 metric tons of all additives planned

- Semiconductors: Focus on high-purity basic chemicals with margins ranging from 40%-65%

- Balanced growth strategy across Pharma, Agro, Specialty, Polymer, and Petrochemicals to reduce dependency on any single segment

Challenges & Headwinds

- Specialty Chemicals: Highly commoditized, pricing pressures, and raw material fluctuations

- Battery Chemicals: Geopolitical uncertainties affecting ramp-up

- Deferred orders in commodity chemicals (cosmetics and parabens)

5 Likes

I am new to the community and hence in learning mode.

Q3FY25 Con call:

Response wrt long term visibility:

Response wrt Baba Fine, Electrolyte and Chinese Competition:

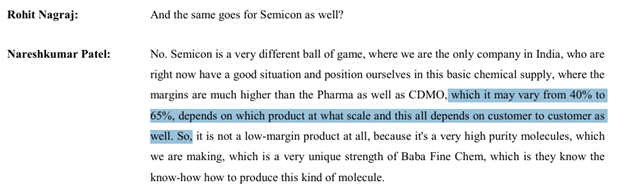

Another wrt Semi-Conductor:

Wrt Guidance and Margin for next 3 years:

I believe if management shall be able to deliver what they promise then share should give good return here onwards. However valuations have already priced in above factors. Hence any fresh entry will lead to high risk for high reward.

I am invested in the stock and hence may have biased view.

2 Likes

As per Incred Equities research report of March-25, Earnings growth of AMI Organics will taper down and the valuation is too high.

• Ami Organics’ FY25F EPS growth is primarily driven by 100% growth in Nubeqa sales, which, in Bayer’s own admission, will taper to 15-20% in CY25F.

• While there is optimism about Nubeqa’s sales, high treatment costs and limited growth potential in developing markets are areas of concern.

5 Likes

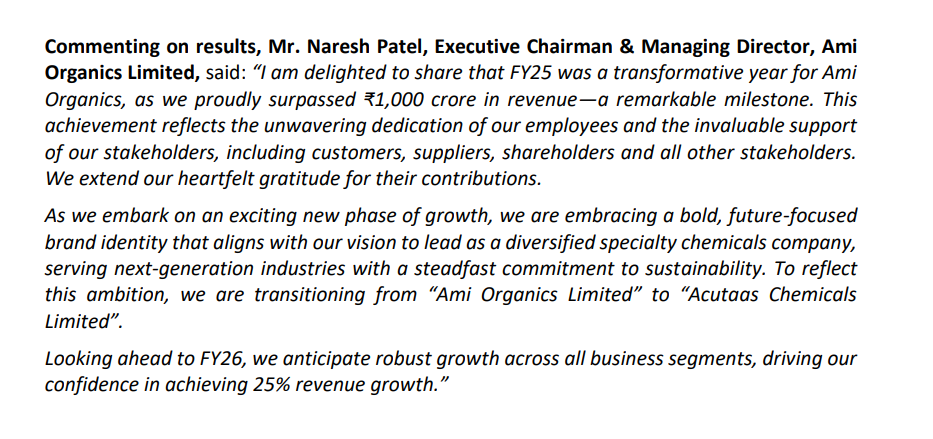

Company going change their name now new name is acutaas chemical ltd

b03ba366-8277-4c92-b1f8-f2c3a2e63fda.pdf (386.9 KB)

2 Likes

Going through Ami’s conference call, the management recently stated this about their CDMO segment: “We anticipate our overall CDMO business to reach approximately 1000 Cr by FY28 compared to 80-90 Cr in the last FY.” This interested me and i wanted to dig deeper.

Broadly, the sales of the company are split between

-

Pharma intermediate - 80% of sales

-

Specialty chemical - 20% of sales

CDMO vertical falls under the Pharma intermediates. AMI organics wants to be only in the intermediates space and not move in to API segment per the mgmt.

They are investing in the Ankaleshwar facility, which currently has a capacity of approximately 450KL and three units. One of the Units (number 2) is dedicated completely to Fermion alone. Fermion is a subsidiary of Orion Pharma (Finland).

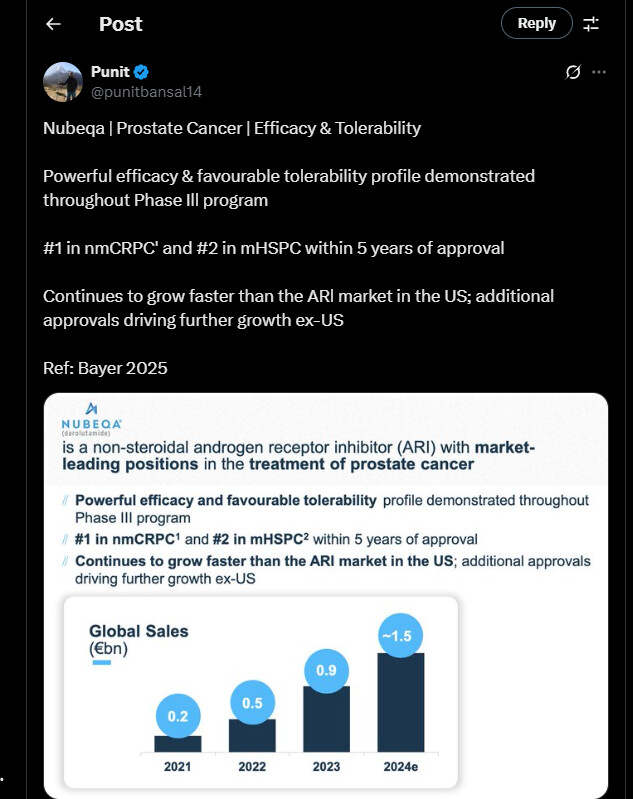

Ami is currently supplying 5 intermediates for the molecule Darolutamide. Bayer is selling NUBEQA as the end product to patients/customers.

This was a collaborative effort by Bharani @phreakv6, Nirvana @nirvana_laha, and me to determine whether the molecule Darolutamide, marketed by Bayer as Nubeqa, will be a meaningful driver for Ami Organics.

From Bayer’s conference call, the co-innovator has tagged the molecule Nubeqa as a blockbuster drug.

- They had touched €1.1 billion by 9 months of CY24.

- For the entire CY24, their sales was €1,523 billion.

Q2CY24

Q3CY24

Based on the EC filing, lets look at what are the steps involved in leading up to the final API, Darolutamide, is made ( as far as the EC docs go and there is some educated guess up until the final API):

Now let’s look at the intermediate molecules

| Intermediate | Molecule name |

|---|---|

| DARO-II | 5-acetyl-1H-pyrazole-3-carboxylic acid |

| DARO-III | (2-chloro-4-(1H-pyrazole-3yl) benzonitrile (DARO-III) |

| DARO-IV | Tert-Butyl((1S)-2-hydroxy-1- methylethyl)carbamate (DARO-IV) |

| DARO-V | S) - 4(1-(2- AMINOPROPYL) -1H-PYRAZOL-3- YL) -2-CHLOROBENZONITRILE |

Daro II:

There is no explicit callout of Daro I in the filing document; we assume it is Methyl-5-Acetyl—1H-Pyrazole-3-Carboxylate(M5AP3C) which is the key raw material for making Daro II. They did not have the capacity for this before the filing, and they have proposed to make 10MT per month (thus, 120 MT per year)

20 Kgs of M5AP3C gives an output of 78 Kgs of Daro II

Daro III:

The route of synthesis for Daro III is a two stage process as shown below:

Based on these reactions:

70 kgs of raw material [1-(tetrahydro-2H-pyran-2- yl)-5-(4,4,5,5-tetramethyl- 1,3,2-dioxaborolan-2-yl)-1H- pyrazole] for this step produces 95 kgs of Daro III.

Daro IV:

100kgs of 2-Amino Propanol and 272 kgs of Di-BOC which are the raw materials produce 100 kgs of Daro IV

Daro V:

Daro III and IV are both needed to make Daro V. 110 kgs of Daro III and 239 kgs of Daro IV along with a few other raw materials- are need to produce 402 kgs of Daro V.

The capacities they have proposed to add for this process are:

Intermediate Molecule name Capacity (MT/Month) Capacity

(MTPA)

DARO-II 5-acetyl-1H-pyrazole-3-carboxylic acid 10 120

DARO-III (2-chloro-4-(1H-pyrazole-3yl) benzonitrile (DARO-III) 10 120

DARO-IV Tert-Butyl((1S)-2-hydroxy-1- methylethyl)carbamate (DARO-IV) 10 120

DARO-V S) - 4(1-(2- AMINOPROPYL) -1H-PYRAZOL-3- YL) -2-CHLOROBENZONITRILE 10 120

The sales number for Nubeqa, as reported by Bayer is:

Now, moving on to the economics:

The daily dosage is 1200 mg/day (2x300 mg tablets - twice a day)

Link: https://www.accessdata.fda.gov/drugsatfda_docs/label/2022/212099s002lbl.pdf

- So this implies it’s 36,000 mg/month (1200x30)

- As per online sources, Nubeqa’s cost is approximately. $14,890 for 30 days of supplies (4 tablets a day x 30 days in a month = 120 tablets)

- So, cost per patient per year = 12 x 14890 =~ $178,500

- How many patients are eligible for the currently approved labels? ( not considering the in-process, to-be-approved label expansions) = 200k-300k. So, let’s take an average of 250k patients.

- And how many gms/day is each patient consuming in a year?

- 1200 x 365 = 438,000mg/year = 438 gm/yr

- So, 1 MT capacity of API should cater to how many patients?

- 1000,000gms/438 =~ 2250 patients

- Assuming a conversion ratio of 1.5:1 for the Daro V intermediate to the final API = 2250/1.5 = 1500 patients.

- So 1500 patients can be catered to, with 1 MT of Daro V. To cater to 250k patients on average, how many MT Of Daro V are needed? = ~ 160-170 MT.

Ami Organics, as per the EC document, has 100 MT capacity currently. This roughly means Ami’s capacity can cater to 60% of the demand.

Looking at it from the reported sales number of Bayer perspective and reverse engineering a bit, their 4th quarter sales figure was 443 million Euros, which approx to 478 million USD.

- Using the same numbers as above, $14890/month of supply of Nubeqa/patient. Per quarter (3 months), the sales cost is ~$44,500/patient.

- We need to take this number with a pinch of salt as the final price that Bayer gets might differ after rebates, discounts with the PBM (pharmacy benefits managers). Also, the supply chain will have its margins. Assuming the supply chain has 20% margins for simplicity’s sake - Bayer receives 80% of the revenue. $44,500 X 80% = $35,750

- This would approx. give us $478M /$35,750 = 13,400 patients.

- Also, the reported sales number is for global sales, and the US might be all but a portion of this 443 million euros. Assuming the US share is 50%, since the prices are highest in the US relative to the remaining 86 countries for which Nubeqa is approved. So, assuming 50% of sales = $239M/$35,750 ~= 6,700 patients. [Please note that only regulated markets can fetch higher prices; other countries have reduced selling prices.]

As of now per reports - NUBEQA is now the fastest growing androgen receptor inhibitor in the U.S., with nearly 45,000 patients in the U.S. and 100,000 patients globally treated as of the end of 2024.(link & link) This is well on the way to the 250k-300k patients addressable market & beyond. They are in the process of submissions for the 3rd indication in US, EU and China. If they get approval in China, that also would unlock additional patients and a major market.

Few points to note:

- Bayer’s sales numbers might also include inventory stocking and not just filling prescriptions (patient count - inflated)

- There are several assumptions/ approximations I have used in the above calculations. If the Daro V to Daro final API ratio of 1.5:1 is different, say 1.25:1, 1.3:1, or 1.1:1 - the MT needed to manufacture will be lower (~140 MT for 1.25:1, 145 MT for 1.3:1, etc.).

- Real-world efficiency might be very different from theoretical efficiencies used above. As stated above, a lower ratio can reduce the demand estimates.

- The 20% supply chain margins can be very different. Bayer’s net sales per patient can be lower if the margins are higher - 30%, 35%, or 40%.

Disclaimer:

Ganesh - invested (tracking position)

Nirvana - not invested

Bharani - not invested

27 Likes

Excellent result from Ami, Overall 37% growth in Top line yearly qtrly basis and138% growth in profit y-o-y .qtrly .will be waiting for mgmt commtary…my objective will be ignore noise, pharma being a very complex subject and listen only to mgmt comments…now onwards..folllowing the mgmt who spent millions in capex in last 2-3 yrs..

25% Revenue growth guidance now..last year, they gave the same number after Q4 2024, then upgraded it, after Q2 2025…

8 Likes

Further to add, Ami mentioned in concall, Margin in FY 26 will ‘definitely’ improve from here,

in H1 , 40% and H2 60% revenue will come..

7 Likes

Fabulous end to the year.

Some points captured from the Q4 FY25 concall yesterday. Usual disclaimers E & OE apply.

-

Guidance of 25 % revenue growth and margin improvement

-

H1 accounts for 40 % of the topline and H2 60 %. Margin also varies accordingly

-

In Q4, Gross margin improved due to better product mix and EBIDTA margin improved due to expansion in GM and operating leverage

-

Pharma CDMO - Rs.1000 crore revenue by FY28 expected. Have a strong pipeline

-

BFC - Expanding into Taiwan, Korea, Japan. Will ramp up in the next 1 or 2 years. Samples are going to customers, approvals in progress.

-

Ankleshwar facility Block 1 - Marquee CDMO. Block 2 - Fungible multipurpose facility Block 3 – Dedicated to marquee customer

-

Margins for FY25 - Advanced Intermediates - 24.5 % Spec Chem 14.7 %, Average - 23 %

-

Sachin Pilot Plant - Will help scale up R&D products. This expansion required since existing pilot plant is not enough. We are also getting into High Potent molecules (which requires special facilities, I think)

-

New CDMO contracts - On track. Qualification stage going on. Revenue will come in H2 FY26

-

CDMO sales for FY25 - we are not disclosing.

-

FY26 - Rs.200 crores capex - Spillover capex Rs.130 crore for Electrolytes + Maintenance Capex, Pilot Plant capex is Rs.70

-

Savings from solar power plant - when 16MW is completed, we will get Rs.16-18 crore p.a. savings. Currently 11 MW is completed

-

Spec Chem - growth is slow due to BFC. Rest has grown 27 % (I think this is the number mentioned, but need to check)

-

No new debt expected for next 1 year at least

-

CDMO - we have visibility of pricing also since pricing is fixed in the signed contracts

-

Pharma generic business is also growing well; RM prices & output prices are both stable currently

-

We don’t have any direct sales to US

-

We have no idea whether current revenue include any inventory build-up at customer’s end which may impact future sales

-

Capacity Utilization for Spec Chem is 60 %

-

Margins for Spec Chem (electrolytes & semiconductor) business will be at current levels only

-

Rs.300 crore investment in electrolyte salts announced earlier - no change in status. No movement on that issue

-

Electrolyte additives - 2000 MTPA going commercial this year in H2 FY26. Will reach full utilization in 3 years

One additional observation of my own (not discussed in the call):

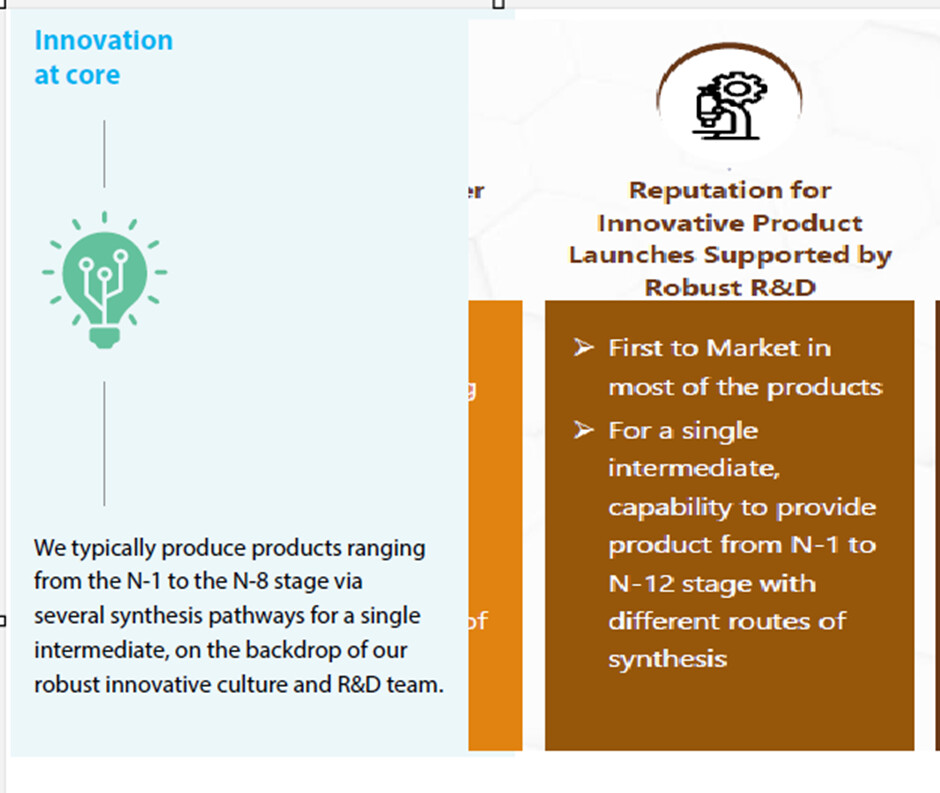

In the past (e.g. FY22 AR), Ami used to mention ‘capabilities to execute products from N-1 to N-8 stage’ but sometime last year, Ami has moved beyond. The presentations now mention ‘N-1 to N-12 stage’ which is a significant enhancement of capabilities from N-8.

(FY22 Annual Report (left) Vs. FY25 presentation (right))

This progression represents a significant advancement in the company’s capability, since each additional step introduces exponentially greater complexity across multiple dimensions, such as reaction expertise, purification techniques, documentation, impurity management etc. It also allows companies to capture a larger share of the product value chain, create their own IP etc. thereby yielding higher margins. This is particularly significant as the industry is moving toward increasingly complex molecules. Research reveals that the average synthesis for drug candidates required 8 steps in 2006, but by 2017 it had increased more than 20 with some complex candidates requiring as many as 92 steps (for the final API)!

I am not a technical person, so I asked AI (after a series of prior questions not given here) what level of sophistication does a N-12 level of capability indicate, and where would it rate it on a scale of 1 to 10 where 1 is the lowest and 10 is the highest level of sophistication achieved by a pharmaceutical / chemical manufacturer. It answered 7 – 8. Here is detailed answer for those who are interested. Those with a technical background are welcome to comment.

N-12 Capability.pdf (312.4 KB)

(Disc.: Invested)

28 Likes

Kotak Mahindra MF acquires 6.6% stake in Ami organics for Rs 301 crore.

Ami Organics promoters Vaghasia Chetankumar Chhaganlal and Nareshkumar Ramjibhai Patel divested the same number of shares at the same price on the NSE.

After the stake sale, the combined holding of promoters and promoter group in Ami Organics has declined to 29.36 per cent from 35.96 per cent.

I’ve compiled everything I know about the company into this PDF. It might be helpful for new investors. Please let me know if any corrections are needed. Also took the help of ChatGPT.

Ami Organics.pdf (1.5 MB)

12 Likes