Amber touring USA, expect some buying by overseas investors soon!

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c1e2d624-17c7-47e3-9dfa-9042e0e5eb41.pdf

Disc: 7% of portfolio @ avg 1500.

Amber touring USA, expect some buying by overseas investors soon!

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c1e2d624-17c7-47e3-9dfa-9042e0e5eb41.pdf

Disc: 7% of portfolio @ avg 1500.

Con call transcript, held on 31 Jan.

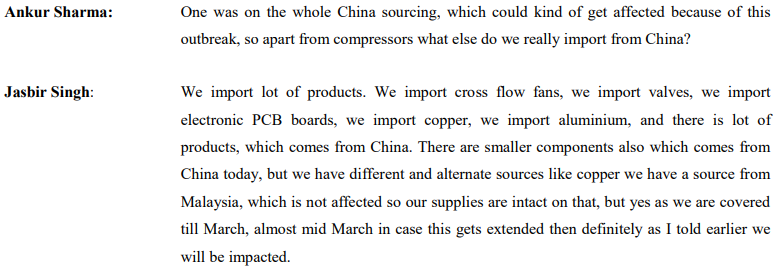

Compressors are sourced from China, Korea and quite large part from India.

No sourcing from Wuhan/Hubei, but there maybe some impact due to delays in China in general.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d441f12a-3a0f-446f-ba6a-13992c6ca196.pdf

Would like to understand more around the cash flows of the company for the last 5 years, seem very abrupt which stands at (-)79 crs for FY 2019. Any views here?

How is Amber doing now with the Corona Virus and the lockdowns affecting most industries? are they getting their parts from China? thanks

Amber said it intends to raise funds for capital expenditure required for the long-term growth of its businesses; extend loans to and invest in its subsidiaries for their long-term and short-term business purposes, repay debt, and make strategic acquisitions or joint ventures.

Need to see how profitable the subsidiaries are.

Amber

Conference call highlights:

RACs: Industry demand momentum sustained in Q4 too, with channel inventory normalising for the industry (in a better position compared to last year as on date).Volumes for RAC in FY21 remained 2.1 mn units (excluding AC gas charging units) for Amber while industry saw volumes of 5.8mn units for FY21. Furing Q4 RAC industry grew by 19-20% while Amber grew by 16%.

PLI scheme: Broad Contours of the scheme has come however narrow down version of the scheme yet to come. Broadly PLI classified 1) Higher value components where Amber is still contemplating opportunities and exploring right partner 2) Lower value components (PCBS, Motor forms etc.) where it is present and will be investing accordingly (waiting for fi ner details). Thirdly other opportunities like injection moulding, sheet moulding, heat exchangers can also come (not sure though and company waiting for fi ner details of PLI) and Amber is present in this and can explore opportunities here too. Accordingly, capex on the same is yet to be decided

Commercial AC line: The company has started commercial AC line for 3.5-tonne and 4.5-tonne products with a focus on developing products till 17-tonne capacity.

Import ban on Air-conditioners with Refrigerants: Amber had earlier signed six new customers since the government has imposed an import ban on CBU with refrigerants. At the initial stage, the brands are looking for gas filling (industry will see 2 million units due to the import ban) and expected to covert these customers from gas charging to complete manufacturing remains encouraging.

In-house manufacturing from other brands: Brands are also looking for enhancing in-house manufacturing.

However, this will not impact Amber as component supplies will continue.

Exports: The company submitted exports samples to US customers in 2021 has passed and will take 8-10 months for certification if approved while it has got certif i cation for Middle East for its products and will be supplying from FY2022. Components exports continue under PICL. Over the next 4-5 years, the management is hopeful of substantial contribution from exports to total revenues and its negligible cost currently.

Commodity impact/ Costs: Commodity price inflation have driven up end-consumer prices by 10-12% and company has passed on the impact of commodity inflation across the customers in time bound manner.

Subsidiary PICL: PLI augurs well for PICL and opportunities in the same provides opportunities to ramp up its revenues and company endeavours to double the revenues in couple of years.

Subsidiary Sidwal: The subsidiary won one new order in Q4. One more is in the pipeline, with that total order book now stands at Rs. 350 crore to be executed in 24 months. Opportunities ahead remains healthy with modernisation across railways and new metros and rapid rail announced.

Capacity expansion: The company has completed the land acquisition (10 acres) for the Supa Plant that will be operational by Q4FY22. The facility will have a manufacturing capacity of 1 million units along with components while it has completed the land agreement in Chennai and expect to start construction in next 2-3 months.

Capex: Overall company expects capex of ~Rs 350 crore for the next two years.

Outlook: The company remains optimistic and confident of capturing the opportunities market presents with better volumes if lockdown eases by end June as extended summer may help in north, despite the short-term challenges posed by second wave of Covid-19.

This is my first detailed thread on Twitter where I have tried covering Amber enterprises from the con calls conducted by the company.

It would mean a lot if you could go through the same. Thanks

how do you see PG eletroplast ?

have any one studied PG eletroplast?

PG electroplast is good company. They are competing with Amber in Indoor AC units. Valuation is stretched…

Keeping it in Watchlist.

Credit Rating Report:

Amber Concall Brief:

2.Another important update during the quarter was on acquisition of majority ownership in ‘AmberPR Technoplast India Private Limited’ erstwhile ‘Pasio India Private Limited’. This acquisition will help our company to grow its component segment with focus on providing more backward integrated solutions in key component of RAC segment which is cross flow fan along with solution of injection molding component for other industries which is refrigeration and auto engine segment.

We are glad to announce the commencement of production at our three new facilities: Kadi in Gujarat for injection molding components, Chennai in Tamil Nadu for sheet metal components and heat exchangers, and Supa in Maharashtra for our sheet metal components in phase I. The expenditures incurred for the commercialization of these three new plants led to a decline in profitability for the standalone operation. However, once the revenue starts flowing in we expect profitability to normalize.

Update on PLI scheme. During the quarter, Amber Enterprises India Limited (“Amber”) has received approval for the manufacturing of AC components under the ‘Normal Investment’ category for a threshold incremental investment of Rs. 300 Crs. Our subsidiary IL JIN Electronics India Private Limited (“IL JIN”) have also received approval for manufacturing Lower value intermediaries of ACs under ‘Large Investment’ category for a threshold incremental investment of Rs. 100 Crs. We believe the production-linked incentive (PLI) scheme approved by the government would help provide a level-playing field to domestic players and create an enabling environment for the industry to compete globally.

Mobility application division which includes Sidwal: . Our order book stands healthy at more than around Rs.450 Crores. We have already onboarded good customers like Alstom and Bombardier…

As a company we definitely would be looking forward to grow at EBITDA level. We will be able to try to maintain 25% absolute return on EBITDA levels moving from FY22 to FY25.

Update on motor division which includes PICL: We have increased our product offering to our customers by adding new models for both the domestic and international markets. We are also adding new customers in this division. We expect our motor division to double in revenues while also increasing margins.

Update on electronic division which includes IL JIN and Ever: As a part of diversification, we have started production of new-age applications like wearables and hearables. We have recently added Boat as our customer. As the market is moving rapidly towards inverter ACs, we are confident of growing our revenue share from this division going forward. We are also getting a lot of queries and approvals are already in process for refrigerator and washing machine and other new products also. So we are hopeful that in electronic division also we would be doubling the revenue in coming two years from now.

Component division which includes both AC and non-AC components: Our component division has played a very positive role. Contribution from component division has increased to 54% in nine months FY22 from 50% in nine months FY21. We are adding new products, new customers and new geographies. We have onboarded new customers like Samsung for sheet metal components and heat exchangers and Voltas Beko for injection molding components for washing machines and refrigerators.

Update on RAC division: Our RAC division is performing in tandem with industry; industry growth on a year-to-date basis is at single digit. It seems that industry would touch around 6.2 to 6.5 million units this financial year; however, at Amber we are expected to touch around 3 million units this year. Inventory levels have been normalized. Inverter ACs are witnessing good growth.

So in total like for the financial year as I told we are expected to be nearing 3 million AC units while in 9MFY22 we have done around 1.1 million units.So, expecting approx. 2 million AC in Q4

Which is anyways strongest quarter for the company.

Disclosure: Invested @800/- level…5% of the portfolio.

In the Q3 FY22 presentation on slide 7, they mentioned that Cross Flow Fan is a high entry barrier product, and domestically only Pee Aar Automotive Technologies Pvt Ltd and 2 other foreign companies manufacturers them. But PG eletroplast also has the capability to manufacture these fans.

Link: https://www.pgel.in/pdf/PR16May2022.pdf

Thanks!!

Amber Enterprises looks interesting to me.

• It is the market leader in room AC manufacturing, holding the highest market share.

• It is a vendor for most other AC companies, including Blue Star, Voltas, etc.

• Last quarter was very strong compared to one of its main competitors, EPACK.

• Annual sales growth is 30.3%, and profit growth is 54.8%.

• The stock has corrected roughly 18–20% from its all-time high (ATH).

• The current P/E ratio is 101, whereas the ATH P/E was 140 just 20 days ago, before the market correction in January 2025.

• There was strong volume action in the last week of December 2024, suggesting the entry of a big player.

• The current price is at the 10-week EMA, where it has historically found support multiple times.

• Further correction from here does not seem to exceed 7%.

• Since Q1 is typically strong for AC manufacturing businesses, the upside potential could be solid.

• Negatives: Margins and ROE in this sector are generally low.

This is just a quick analysis—I still need to dig deeper.

Does anyone know about BIS? I

Apparently it’s causing some issue with importing some components required for these manufacturers.

Disc ; looking not invested.