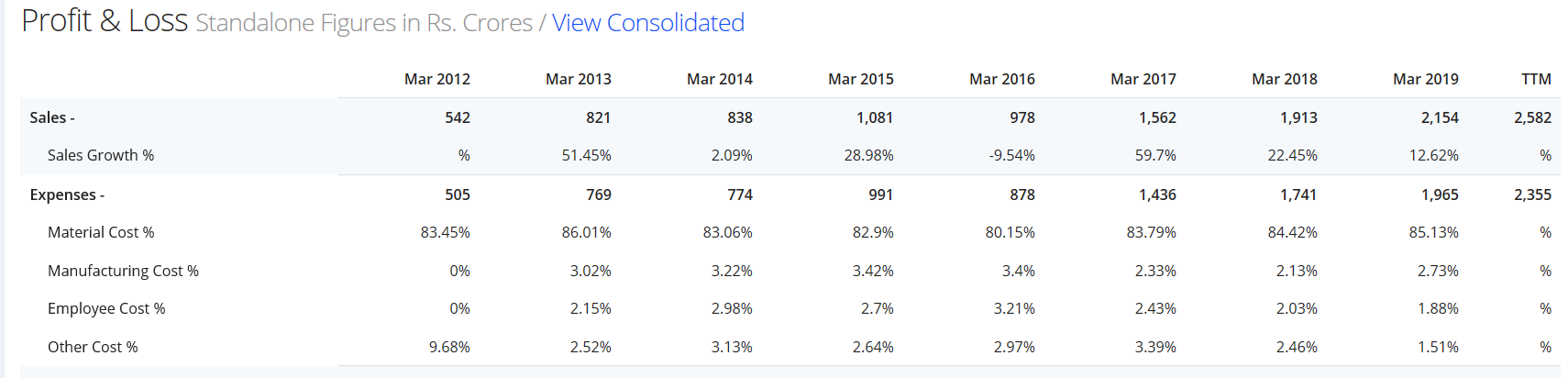

@nityanandparab ji Sorry to respond you late this is the snip from screener

HOW THEY WILL GROW: they can take either organic or inorganic path for growth .But in march 2018 they shows income from shares as 474.68 Crs

COOKED THE BOOKS ( My intent is not that they had cooked the books but there MIGHT be chances i haven’t gone to deep as i was not interested in the company so didn’t dive deep that’s the reason i wrote i might be 100% wrong )

There are many ways that a company can inflate the earning specially during the BULL run .It gave them good chance to raise more money

regards