Aluwind Infra-Tech Ltd is a leading manufacturer of custom aluminum and glass architectural products, such as curtain walls, windows, doors, and facades. Offers tailored architectural designs for aluminum and glass structures.

Company was incorporated on April 22, 2003 by Mr. MM Kabra and went public on April 4, 2024 Listed in NSE SME.

Current Market Cap - 194Cr, Listed in NSE: SME

Products:

- System Doors & Windows

- Railings & Balustrades

- Curtain Walls

- Structural Glazing

- Unitize Glazing

- Spider Glazing

- Aluminium Composite Panel

- Sky Light

- Canopy

- Powder Coating Facility.

Growth Drivers:

- Robust orderbook (350Cr+) and consistent order inflows.

- Industry Outlook & Market Demand - Growing demand for green buildings and sustainable practices is driving growth in the real estate sector, especially in office and retail segments.

- Industry Tailwind - The Indian facade industry is witnessing substantial expansion, with forecasts suggesting a Compound Annual Growth Rate (CAGR) of 8.3% from 2023 to 2028. The market is expected to reach USD 4,254.5 million by 2028, up from USD 2,638.2 million in 2022.

- Rising public infrastructure, offices, shopping centers, and factories, coupled with rapid urbanization and real estate growth, are driving demand for residential and commercial construction. Additionally, the focus on sustainable and eco-friendly building practices is boosting the need for advanced façade systems.

Clientele:

Clients include L&T Group, Lodha Developers, Hyatt, Godrej Properties, Oberoi Realty, Piramal Realty, McDonald’s, JCB, Thermax etc.

Order Book & Recent Order Inflows: As per my view company’s current orderbook looks very exciting. Nice order inflows from L&T.

Total 302Cr of Orderbook as of 25th May 2025.

+19.2Cr order from L&T Construction on 1st June 2025,

+15.6Cr order from L&T on 7th August 2025. (For Mumbai-Ahmedabad High Speed Rail facade)

+23.8Cr order from Larsen & Toubro Limited on 12th August 2025.

Business Operations and Capex:

-

Use of Advanced Materials: The company uses a trademarked, state-of-the-art aluminum alloy called “Duranium,” a trademark of Hindalco, which has a sleek, modern finish, corrosion resistance, and more strength and better finish as compared to as compare to 6063-T6 alloy. Windows made out of Duranium offers better noise protection and strength.

-

Partnership with Erternia, Hindalco: The company is the Anchor Partner for Hindalco Industries Limited’s (Aditya Birla Group) premium aluminum window and door brand, Eternia, in the Mumbai Metropolitan Region (MMR). This partnership will help Aluwind to build high-performance and reliable fenestration solutions.

-

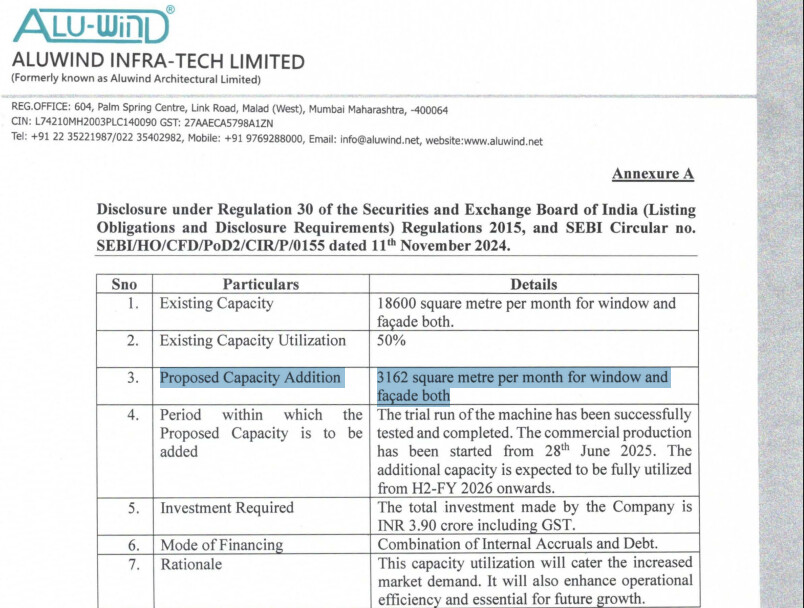

Before June 2025 Aluwind had a capacity of 18600 square metre per month for window and

facade both.

-

Capacity Utilization (Q1 FY26) - 50%.

-

Capacity Expansion (Completed) - 3162 square metre per month for window and

facade both. Additional Capex has been operational from 28th June 2025. A full utilization might be possible from H2 FY26 onwards.

-

Company is using recently purchased CNC Machines to increase production capacity of doors, windows, facades, HST sliding structures.

Experienced Top Management:

- Mr. Murli Manohar Ramshankar Kabra (Managing Director) - He has 20 years of experience and responsible for strategic direction and execution of over 500 projects across India.

- Mr. Rajesh Kabra (Executive Director and Co-founder) - He has over 20 years of experience in procurement and supply chain management. Responsible for logistics and sourcing, with extensive connections in the aluminum industry.

- Mr. Jagmohan Ramshankar Kabra (Executive Director) - Heads the manufacturing unit in Pune and is responsible for production operations. He holds more than a decade of industry experience.

- Ms. Varsha Amrutlal Shah (CFO) - She has over 2 Decade of experience in the field of Finance and Accounts and have been associated with our Company since February

10, 2014. She currently is the Chief Financial Officer of our Company

heading the Finance Department of the Company.

Risks:

- Dependence on subcontractors and supplier.

- Any slowdown in the real estate sector in India could significantly decrease the demand for the products.

- Profit margin depends on Aluminum Prices.

Strength:

- Robust Orderbook (350Cr+) with average execution timeline of less than 24months.

- Timely Project Execution track record.

- Significant Capacity Expansion on Window and facade (3162 Squire meter)

- Use of cutting edge technology and 5 axis CNC Automation Machines.

- Constant focus on R&D and Partnership with Eeternia.

- Reupdated & diversified clientele across various industries (Action Construction, Renewable Energy, Pharma, Logistics & Supply Chain, Nuclear Research & Development, Food & Beverage, Heavy Machinery etc.)

Financial Performance:

- Though margin was subdued in FY25 (11%) compared to 14% in FY 24, PAT remained stable due to 31% Revenue Growth.

Disclosure: Invested at a low quantity level. Kindly do your own Due Diligence before taking any investment decision.

14 Likes

Thanks for the information on a new company. We should present any such new companies that we are tracking.

Having said that, I give my observations as follows:

Capacity addition is not significant. Only 10 percent addition which is generally done by debotellenecking exercise.

So this capacity addition can not be taken as a rerating.

No reason given for significant fall in margin.

Though there is significant tailwinds in order, margin and capacity utilisation are the main issues.

PE ratio is high wrt FY 25 earnings.

So it is presently richly valued, but share may go up as liquidity is low in SME stocks.

So altogether not compelling for fresh investment at prevailing valuations.

3 Likes

Thanks for sharing your point of view.

If we compare Aluwind’s current Orderbook and Execution Timeline with its peers it is still looking slightly undervalued.

Innovators Facade System Ltd: Order Book - 357Cr as of Feb 2025. (66% Growth from Previous Year). Company had Market Cap of around 340Cr. Current P/E: 21.4

Aesthetik Engineers Ltd: Orderbook - 85.6Cr as of Aug 2025. Company has Market Cap of 206Cr. Current P/E: 40

Average execution time of Aluwind’s projects mostly hovers around 16-18 Months.

For Aluwind Even if the PAT Margin remains same as last quarter (~9.2%), based on the orderbook H1 FY26 Revenue and PAT both may show a 50%+ Growth. Aluwind also has Cash conversion cycle of 126 days which is lower than its peers.

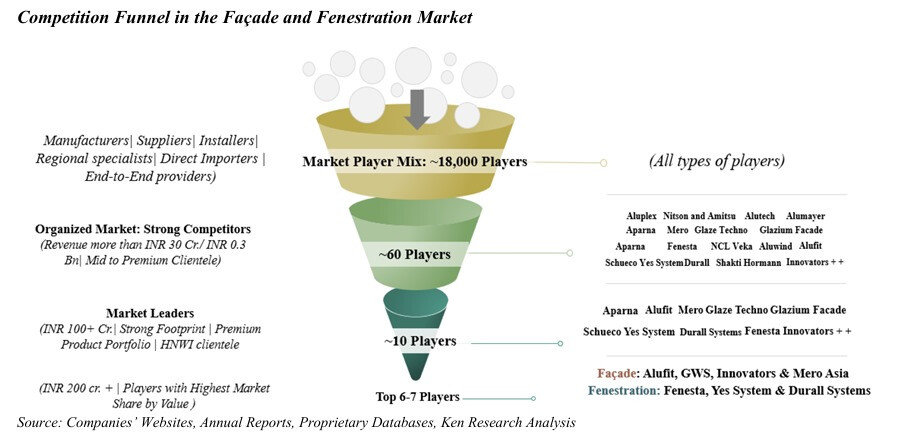

Less than 10% of the players in the facade market are organized. Unorganized markets are giving way to organized ones. In addition to the increasing demand for facade projects, organized players have a competitive advantage in expanding their market share and geographic reach.

3 Likes

Don’t you think Sejal Glass as its peer?

Also, another company named Glasswall systems is coming up with the IPO soon.

2 Likes

Interesting company, I had an opportunity to visit their plant back in June, sharing my thoughts on the company.

- Industry: The India facade market size reached US$ 2,855.4 Million in 2023. Looking forward, the market is expected to reach US$ 5,431.9 Million by 2032, exhibiting a growth rate (CAGR) of 7.18% during 2024-2032.

Why Aluminium doors and Windows are in Demand?

-

The India aluminum doors and windows market is primarily driven by the construction and real estate sector. The demand for energy-efficient and aesthetically pleasing building components has fueled the growth of aluminum doors and windows. They offer durability, low maintenance, and corrosion resistance, making them a preferred choice for modern construction.

-

The use case although is across segments including Residential, Commercial, and Industrial but the commercial sector dominates the facades market due to its emphasis on design, functional requirements, financial capacity, and commercial building growth. The boom in urban projects demand advanced facade solutions for aesthetic appeal, energy efficiency, and sustainability, leading to a favourable demand within the facade sector.

What’re the Tailwinds?

-

Govt. initiatives like Atal Mission for Rejuvenation and Urban Transformation (AMRUT), Formulated by the Bureau of Energy Efficiency (BEE), ECBC mandates energy-efficient building design practices—including façade and fenestration performance standards—for commercial, institutional, and public buildings.

-

Green Building Certifications (IGBC & GRIHA) To promote sustainable construction, government bodies and private developers are increasingly adopting IGBC and GRIHA rating systems, which emphasize energy efficiency, material sustainability, and reduced environmental impact. This trend has accelerated the uptake of solar-enhanced, ventilated, and thermally insulated façade systems.

-

Commercial Real Estate proxy- High-rises, IT parks, airports, malls, hospitals, hotels, corporate HQs**- demand curtain walls, unitized glazing, cladding, double-skin façades. These require large glass panels, structural glazing, and custom aluminium systems, which are capital-intensive and technically complex. Commercial Space Demand Rises 11 Per Cent CAGR in Top 8 Cities

South India’s dominates the Indian facade market as per Aesthetik Engineers RHP. Facades need structural calculations (wind load, seismic, heat transfer) and special installation methods.

Who’re the clients?-

Key projects executed: They have completed over 300 projects executed across 25+ cities. Projects including system windows and curtain walls to skylights, ACP cladding, structural glazing, canopies, and railing. Checkout the recent Annual Report for a great understanding. (https://aluwind.net/residential/)

Right to win and Key Triggers?

-

Strong Client Relationships and Industry Trust: The Company has built lasting relationships with top-tier developers, including repeat projects from marquee clients. Aluwind has been able to maintain a 100% project completion rate with zero project abandonment or defaults.

-

Company’s system window is made using Duranium – World’s first patented Aluminium Alloy offering high strength, large sleek windows for uninterrupted views. As an Anchor Vendor for Eternia (a Hindalco brand), Aluwind plays a pivotal role in elevating the brand’s market presence. The products are WiWa certified for superior production against wind (cyclones), water leakage, noise, and dust.

Its aluminium windows meet the quality and performance benchmarks of both European (EN) and American (AAMA) standards, making them ideally suited for environmentally conscious developments and premium institutional projects.

-

Preferred partner for luxurious apartments and premium architectural projects having completed over 300 projects executed across 25+ cities. In selecting contractors for major projects, customers generally limit the tender to contractors they have pre-qualified. prequalification criteria like net worth, experience, capacity and performance, reputation for quality, safety record, financial strength and bonding capacity and size of previous contracts in similar projects. The company designs bespoke systems for thermal insulation, structural wind loads, acoustic and seismic performance, and fire safety.

-

Expansion: “The 100,000+ sq. ft. Pune facility, enables fully integrated project execution—from design to coating to delivery. This centralization ensures tighter quality control, faster turnaround, and consistent standards across every project site. Investments in next-gen CNC systems, automated powder coating, and streamlined production workflows have enabled us to deliver faster, with superior precision and reduced waste.” - Annual Report 2025

-

New Products: Actively broadening the products range—including advanced curtain walls, high-performance cladding systems, and solar-integrated façades (BIPV) and Facade cleaning services(manual and drones).

-

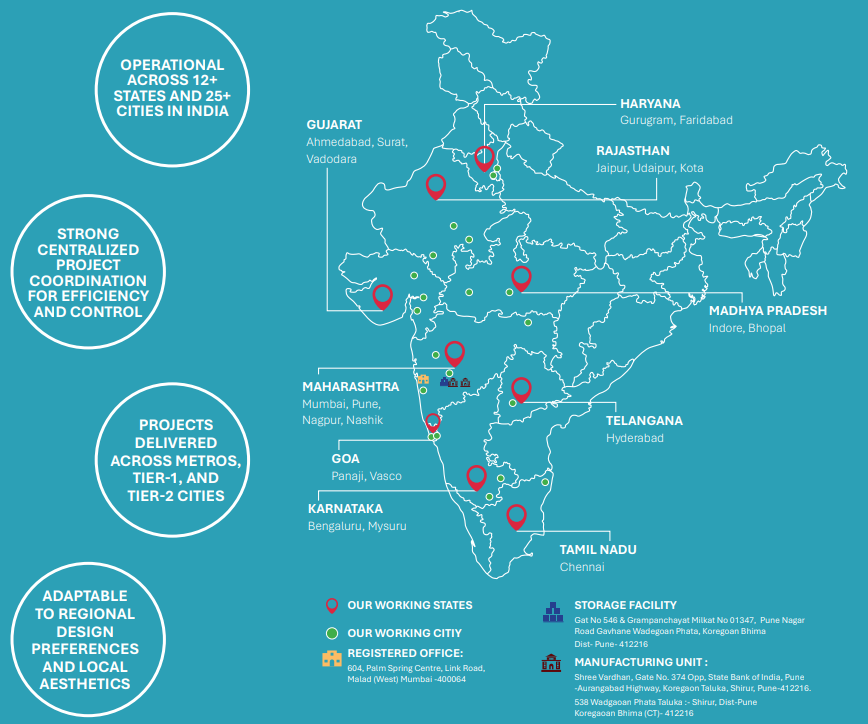

Geographical Expansion: With a presence across major Indian states, the company has

the infrastructure and logistics to manage projects of any size or complexity. This lately is visible in the orders they’re receiving in Southern regions.

“We are actively extending operations into high opportunity regions like Karnataka, Gujarat, and Telangana, backed by detailed market studies, agile execution teams, and competitive pricing structures.”

What’re the optionalities in the business?

-

The Company is expanding its operations beyond architectural work, covering various verticals, including modern interior and exterior works, infrastructure projects, and technology driven solutions. One of the Company’s major strategic initiatives includes the integration of solar façade systems, combining aesthetics with renewable energy performance.

Solar Facades are at a very nascent stage of development at the moment. It can although be a great optionality if things play out well.

-

Ventured into Facade services with Aluwind Clean Tech Pvt Ltd: The services shall include, but not be limited to, cleaning, restoration, and pressure washing of façades, glass panels, cladding, and structural exteriors, either manually and/or through the use of drone cleaning technology. Watch this video to understand the scope: Cleaning it with a Robot

My understanding:

The company is currently trading at a 24x FY25E at a market cap of 195 Crores. The company has an order book of 360 Crores+ (Last year’s topline is 109 Crores) (Including the orders received post May press release) fairly executable in the next 12-24 months and has recently added a new capacity equipped with 5 Axis CNC machine to help them cater to a larger demand with more efficiency, less wastage, lower cost, quick turnaround and also allow them to bif for higher ticket sized orders.

I believe the next few years could mark a high-growth phase for the company, with façades potentially serving as a small but key structural proxy to commercial and residential infrastructure growth in India. The industry remains under-researched, given limited public data and its largely unorganized nature (~10–15% organized vs. ~85–90% unorganized, based on scuttlebutt with peer managements). Peers include Innovators Facade(marquee investors like Vijay Kedia and Chartered Finance hold good stake), Aesthetik Engineers(Small regional player based out of Kolkata) and Unlisted peer include Glass Wall system (Unlisted player with screwed financial performance).

The management is pro-actively diversifying the products bouquet with planned entry into Solar Facades, Facades cleaning service (Drones Focused) and launching new products complimentary to existing products in Windows and Doors as highlighted in AR 2025. Facades are a higher margin business as compared to windows and the company is majorly focused on the facades projects which’ll help them improve their margins as well.

Disc: Invested, Biased and No recommendation. Micro caps are risky bets, Do your own DD.

References:

10 Likes

Glass Wall Systems(A larger peer) has filed its DRHP recently. An impressive visual to note is the layer wise bifurcation of the industry showcasing limited players executing at scale similar to Aluwind and Innovators. Aluwind should be in the top layer soon having crossed 100 Crores in the recent year and going by the order book and execution timelines- Can be a top tier player in next two years.

Link to DRHP: SEBI | GLASS WALL SYSTEMS INDIA LIMITED

Interesting to watchout how this company executes in FY26 and FY27 given decent order book and a supply chain backing by Eternia(Hindalco). Facades as a segment itself could emerge as a structural second-order play on the Commercial Real Estate and Infra cycle. Only time can confirm this but the pathway towards it becoming a credible structural proxy is increasingly visible as order flows remain strong across the industry (something similar to PEB?).

Will drop notes on Glass Wall Systems DRHP in upcoming threads.

Invested and Biased.

5 Likes

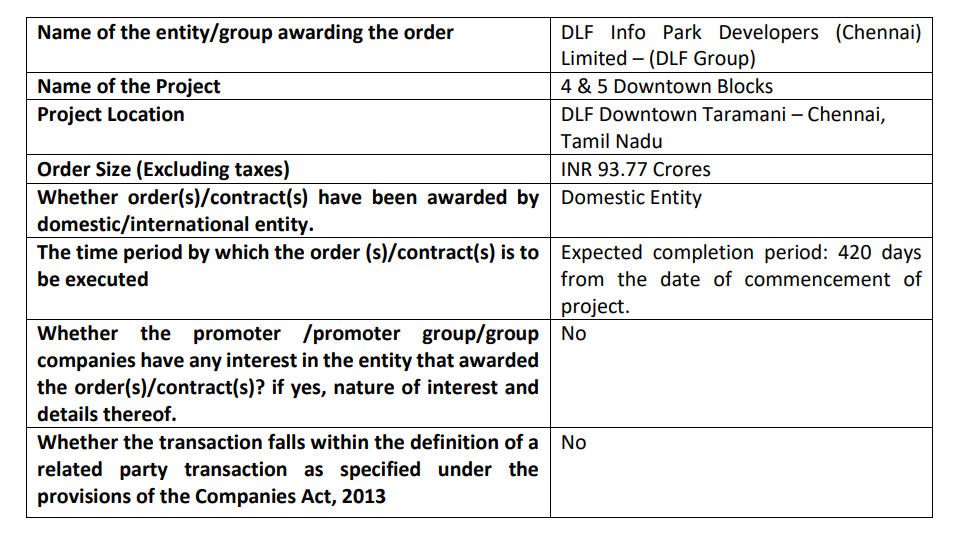

Order flow continues to be strong across the industry. Innovators has received the Letter of Intent for Work Order of Design, Supply, Installation & Commissioning of Façade Glazing Works from DLF Group- again from Chennai.

1 Like

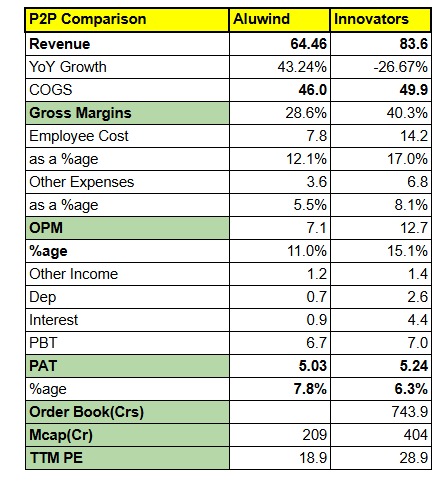

Aluwind H1 numbers look absolute classy with solid uptick in revenues and multifold profitability YoY considering all the monsoon related impact on the construction and realty projects.

- Revenues up 43 pct YoY to 64.46 Crores,

- Operating profit at 7.1 Crores vs 4 Crores YoY

- Operating margins at 11 percent vs 8 percent YoY

- PAT at 5.03 vs 2.26 Crores YoY

- Highest ever inventory at approx 40 Crores (Gearing up for big H2 possibly?)

- Receivables at 33.75 Crores up slightly from 29 Crores in March 25

- OCF is negative but judgement should be on full year balance sheet as H2 tends to be almost 1.5x of H1 going by last year’s trend. (Can we expect 90-100 crores in H2?)

Interestingly the larger peer Innovators posted terrible numbers (Topline declined by 26.7 pct)citing reasons such as :-

- Due to delay in project design approval from clients,

- Delay in readiness of project site of clients; and

- Delay in site mobilization after design approvals

I have done a quick P2P between the two companies and Aluwind execution has been far superior and inline with order execution timelines. Game largely is how efficiently can you utilise your inventories, execute projects early or on time and dedicate the same resources for the next job.

The company did not put up a press release post results but rough calculation on order book announcements bring about an order book of 330-360 crores fairly executable in 12-18 months. With these numbers Aluwind is now trading at a TTM P/E of 18-19 and H2 being the heavy quarter for projects execution I expect better numbers in H2 along with margins expansion as asset turn can be better.

Disc:- Invested and Biased!

ALUWIND_12112025174304_Outcome.pdf (1.4 MB)

3 Likes

Aluwind Infra-Tech has delivered excellent results in H1 FY26, with PAT and EPS growing by 122.75%. The current total order book stands at ₹315 crore, supported by new projects from top-tier clients in major infrastructure and institutional sectors. This robust order book provides strong revenue visibility for H2 FY26 and reinforces the company’s growth momentum.

The company has also recently imported Italian 5-axis CNC machine for its manufacturing facility, significantly enhancing production efficiency and capacity.

Diversified Orderbook: The company’s order book is well-diversified across various sectors, including healthcare (AIIMS Madhuri), commercial (Innovation Campus), major infrastructure (MAHSR), corporate (Capgemini Chennai), residential (Tata Serein, Thane), and port infrastructure (Mumbai International Cruise Terminal), reflecting strong credibility and presence in marquee projects.

Disclaimer: I do not hold any personal positions in the company, but I am interested in investing.

2 Likes

Hi, Slightly on a different topic, how do you get comfortable with the all family involvement in the business? While this is applicable for most nano/micro/small caps, i note most if not all positions are held within family - there are also roles i assume have been made up for members for a 200 odd employee strong company. Taking this along with the fact that members also being in positions at other infra consulting or infra firms. Would it get too many cooks at some stage? Employee reviews online as well highlight this as issues at different levels.

Disc: Not invested, studying the company.

1 Like

It’s very subjective and largely a function of an investor’s style. We have seen companies like Waaree Energies grow from a small-cap to a large-cap in a short span of time, becoming the poster boy of family-run businesses. On the other hand, we’ve also seen legacy players like Liberty Shoes struggle and destroy value, even when the entire segment grew multifold and they had a strong head start.

Facades manufacturing and EPC as a segment doesn’t really have a lot of entry barriers and there are regional players still command significant hold across regions. Aluwind has good order visibility from Southern regions and they wanted to focus more there - would like to see them scaling up profitably across regions and making a mark by finally becoming a PAN India player.

Disc: Invested

2 Likes

Aluwind Infra-Tech – Capacity Expansion Query

As per the recent NSE disclosure, the company has an installed capacity of ~18,600 sq m/month operating at ~50% utilisation, while also announcing an additional capacity of ~3,162 sq m/month.

Query: What is the strategic rationale for adding capacity when existing utilisation is still low? Also, given historical utilisation of ~40–45%, what gives management confidence in achieving near-100% utilisation of the new capacity by H2 FY26?

Would appreciate insights from fellow investors tracking demand visibility and growth plans.

1 Like

i think company have a order book of 315 Cr (approx) while p.y revenue is 110 Cr. Generaly take 12 - 18 (max 24 ) months for execution .

may be that is the reason

This industry definitely has a lot of tail wind and ideally a well managed company should do well over long term.

key points to analyze in greater detail for me -

Its highly competitive and hence not a seller’s market at all. Selling to B2B further makes the working capital management very important and also management of commodity prices (ability to pass on the fluctuations).

But surely a sector with great future potential.