thanks @Prasad_H

this company is super exciting…i was doing research on this stock and its indeed very interesting… below is my views… i have few questions if you can answer?

So below is the rough estimate of the 35cr massive CWIP i can do based upon various information online although i am asking company on this point ( which should also be part of next annual report so waiting for that)

| Cr | Particulars | Expected date | Profit/Cost Saving per year |

|---|---|---|---|

| 5.33 | 1.4MW Solar plant | 2020-21 probably Q2 | 1.6cr cost saving in full capacity |

| 14 | Production expansion from 9000 to 13500MT | 2020-21 probably Q2-Q3 | 8cr profit to be added if sales realisation is good? |

| 15.67 | Jordan project | 2021-22 | No idea at the moment |

Lets take 1 items at time and what i have noticed till now

Point 1: 1.4M Solar Plant

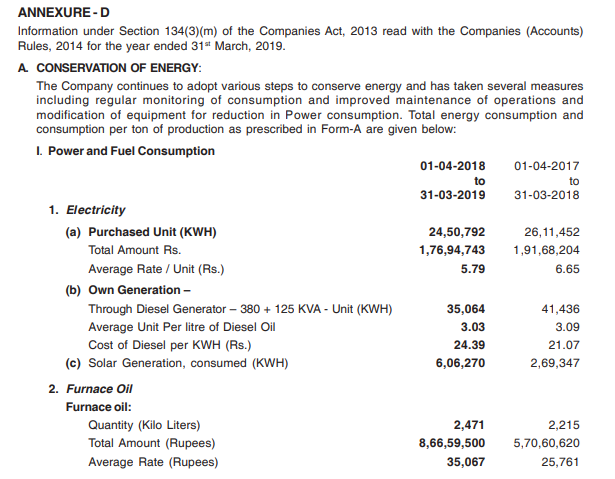

Company currently spend 1.76cr on purchase of electricity and its roughly 1.76cr for 2019FY

its new solar plant should give it 1000KWH24252= 60,48,000KWH on annual basis

Company new production will also consumer additional roughly 12,00,000 KWH vs its existing 24,50,792 thus making it 35,00,000KHW. Do we know why so much additional then is required? could company have done away with just say 40,00,000KHW? given these are large one time cost so maybe for future expansion?

anyway even taking current expansion and new capacity into account, it can nearly save 36,00,000*(5.79 cost of purchase - 3.03 disel cost ) which is roughly 1cr /yr and it can go upto 1.6cr per year once maybe they further expand in future for which they require this additional spare capacity.

my view, very good investment with break even potential in 5yr

Point 2: Production capacity of 4500MT to be operation by Q2-20

so below i can find from annual report and also tried to imply the sales realization / unit. Noticed company did well in both last 3yrs. I dont have details on 2019-20 but seems company benefited due to china situation and china strict laws on environment is giving company good advantage

refer below article : New contract cycle and raw material sourcing holds promise for re-rating of Alufluoride

so once annual report comes we will have more clarity on why it posted good sales this year .

now interesting part is it currently has 8800MT capacity and new expansion will increase it by 4500mt further thus potentially with same 20% operating profit and sales realization, it can add massive 8cr to operating profit

Can you check and see if this make sense to you? so overall under normal scenario we cna expect comnpany operating profit to jump from 16 to 24 cr with same margin. I think this year due to lockdown sales and margin might be impacted so maybe close to 20cr? still quite good upside

Point 3: Jordan project

As per my rough estimate for CWIP , it seems they might have spended 15cr on this, I cannot find details anywhere online on how much it can generate as revenue etc but looking at investment vs its expanded production capacity it seems massive investment? does it have the potential to generate further 10-20 cr and that could be a game changer then?

I am getting more clarify on cost and expected revenue from this project as this is where the future of this company lies in my view.

Conclusion so overall this year profit was 10cr

2020FY : it seems with expanded capacity and cost saving on power …it can add on a prudent basis maybe 4-5 more cr on a conservative basis it seems

2021FY : Jordan project should be a game changer. Need to dig more information on this

would be great to have your views and details on the missing pieces if you have, I will keep digging - super exciting stock