Thanks to all for the contribution. I am a new entrant and like to seek clarification on the profit visibility as per below approach.

At the end of Financial year 2016-17, orders on hand worth 1200 crores ( majority should be NSP - Source : Annual Report).

NSP contract duration is Sept 2016 to Sept 2019. Assuming 7 quarters to complete the order ( FY 18 and FY 19 – Excluding July – Sept Quarter) revenue for each quarter should be about 171 Cr. ( 1200/7)

Considering the profit realization of 14.6 % ( Average of consolidated profit for two financial years - 2016 -17 : 16.4% and 2015 – 16 : 12.8%)

The profit per quarter should be 24 Cr and per year ( FY 18) should be 72 Cr ( Ignoring July Sept Quarter and any additional order income – specifically the recent ONGC order of 154 Cr not included – being conservative)

This should translate into a EPS of ( 72/0.612) 118Rs for FY 18.

Assuming PE of say 9.5 - 10, this should translate to a price band of 1121 – 1180 Rs towards end of this financial year.

I am not sure this is correct approach . Request your views/ Comments.

Disclosure: Invested in this stock recently

Guys, just one suggestion. We should not look at pe as the basis of valuation for such one off large orders. Gives false picture. P/E will be abnormally low for next 2 years due to windfall gains for large ONGC order. Mgmt have themselves said we should not expect similar run rate going forward (post 2019). So, one should normalize things in order to value such companies.

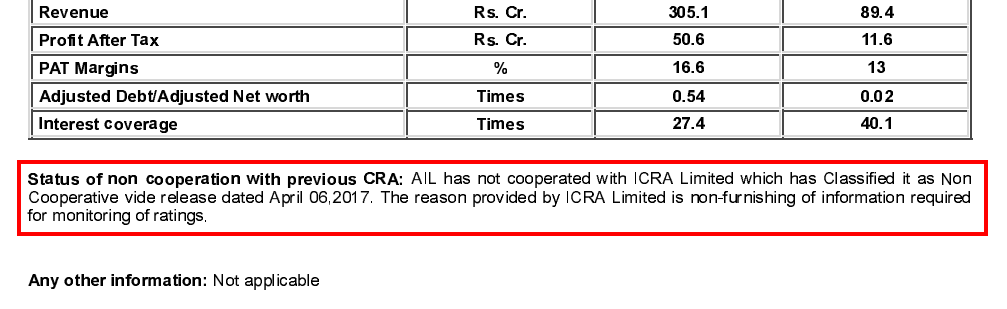

Hi, do anyone know why did the company refused to share the details to ICRA for credit rating purpose in Apr, 2017? Just curious. It is mentioned in the rating rationale published by Crisil on Sep, 2017

Also that the book value or dividend would go up due to the higher cash generation following this order. If the runrate slows down after the order completion, the new normal should be higher price. If however the cash is paid out as dividend, the cost of holding should come down materially. Current price presents a decent entry point.

Thanks @raj1968 for starting the topic, excellent analysis and answers to most questions raised.

I am new to VP, but have got very interested in Alphageo since I saw this company on my screener. Has all the makings of a value stock. High ROE, Low debt over extended period, niche business, low cost leader, low market cap.

Btw, the latest quarterly result does say that the new order would be executed by January 2019 so that’s further good news for coming few quarters.

The only open question in my mind is management right now, given Mrs Savita Alla got a total compensation increase of 21 times in the year ending March 2017 including 3.67 Cr as Commission (% of profit) (Source AR 2016-17)

@mohammedsaqib: Please could you share whether you wrote to the CS of the company and her answers?

Thanks!

Disc: Not invested yet, but very interested in investing at current levels.

Have a couple of queries. Why did trade receivables climb from INR 39 Crores in FY 16 to INR 157 CR in FY 17? Is it because of the nature of the business, that the net trade receivables is usually more than 50% of the topline? Overall company is required to do short term borrowings in order to run the business and cash flow from operations (after working capital change) also do not mirror the bottom line enough.

Also the remuneration of the promoters coupled with low stakes in the company, is that of any concern?

Disclosure: not invested, but looking to invest based on above clarity.

Please have a look at the half yearly BS published by alphageo. Receivables down to 54Cr. They need some time to bill and get the money from ONGC. As per the management they never had a payment issue with ONGC.

Regards,

Raj

Disc: Invested. No trading in last 30 days.

in notes they have mentioned that revenue of 6.6 cr is doubtful so they have not included it in the revenue whereas the costs related to the same have been accounted so a dent in the profitability.

They have also provisioned 1.59 crs for that. So overall there is a net effect of 8.2 crs in the bottomline.

Anyone with knowledge about the company’s potential gain from OALP round 1 bidding? Can we expect them to get additional orders from the winners? If yes, by when?

Anyone with information on this? The stock looks highly attractive at its current price with its large order book, and also potential for more orders through OALP.

Just want to be sure how much and when will the OALP benefits be realized.

The cfo evades shareholder questions saying he’s busy. Surprising that he’s an employee and gets to decide whether or not to respond to shareholder queries. Can sebi help?