Incorporated in 1987, Alphageo (India) Limited is engaged in providing seismic survey services to the oil exploration & production sector. The company provides various services, including design and pre-planning of 2D and 3D surveys; seismic data acquisition in 2D and 3D; seismic data processing and reprocessing/special processing; seismic data interpretation; generation, evaluation, and ranking of prospects; reservoir data acquisition; reservoir analysis. Alphageo also offers topographic surveys with GPS and RTK; tape transcription; digitization of hard copies of maps, seismic sections, and well logs into CGM, SEGY, and LAS formats; and third party quality checking for acquisition and processing. The company is headquartered in Hyderabad, India.

The company has been engaged in seismic data acquisition, processing and interpretation for the last couple of decades. Its comprehensive service range makes it possible for customers generally oil and gas exploration companies - to identify subterranean deposits with efficiency and effectiveness.

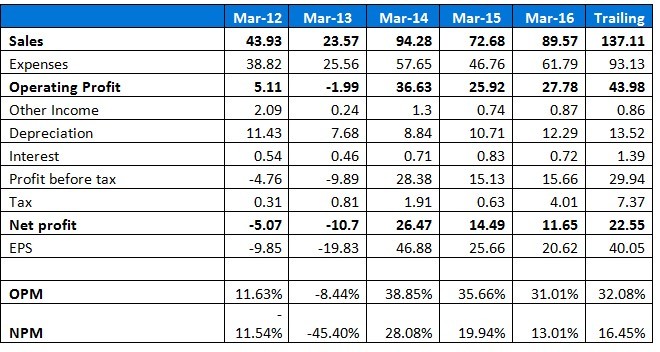

Annual Results (Consolidated):

Source: http://www.screener.in

You can go there for more financial details.

Investment Thesis:

The Company is one of the few seismic survey companies in India who have survived the downturn of last 3-4 years. During those years company ventured out of India and got some order from Myanmar. This enabled the company to survive where most of it’s peers perished. Management must be complimented for keeping the company debt free and adding/upgrading their systems with the latest available. The company recently won a massive order of Rs. 1482cr from ONGC under the national seismic program. The company’s balance sheet is in a good shape to execute the order by taking some leverage. Their OPM has been of the order of 30%+ in the past and management seems to be quite conservative ans sane.

The company whose highest ever sales was around 100cr is sitting on an order book of 1700cr to be completed by March 2019. It’s sales will increase 6 times and accordingly profit as well.

Risks:

Execution of order is going to be a major challenge as the order is almost 6 times higher than what the company has ever handled. The coming quarters will show how the execution progresses.

Since the business is order driven, hence there is very little visibility on what happens after these large orders are completed. Although management has indicated that there might be 3D orders coming in future post the auction of the oil blocks.

As per the management interview post order win, they need to raise 100cr to execute the order which will be a combination of equity and debt. There may be a dilution as well.

References:

I found an excellent blog on alphageo which provided an excellent insight into the company. However, these blogs were written before the company got their mega order of 1482Cr from ONGC.

I am invested in Alphageo with more than 10% allocation from a lower levels. There was no trading done in last 3 months.

This is not a buy/sell recommendation. Please do your own due diligence before taking any action.

@Administrator This is my first story on VP. If I have missed anything or not in compliance with forum rules, please do let me know. I will correct the story accordingly.

Alphageo and several domestic companies are only in onshore/onland seismic survey whereas offshore survey is dominated by foreign players. Its very important and complex to understand the tough terrain of north east, himachal, rajashan areas, that’s why you don’t foreign companies,also you need local skillset to work with interior areas. Main players in onshore survey are Alphageo, Shiv-Vani, Asian Oil Fields, Quippo (subsidiary of SREI Infra Finance). Except Alpha, most of the compititors are ridden with high debt, that’s why Alpha wins most of the orders.

Main players in offshore survey are SeaBird Exploration Group, Petroleum Geo-Services, TerraSond, LoneStar Geophysical Surveys, Seismic Surveys, Inc., Dolphin Group ASA, Terraseis, MMA Offshore Limited, Kuwait Oil Company, Polaris Seismic International, Spectrum ASA, Breckenridge Geophysical and BTW Company Ltd. among others.

Follow this link to understand how 2D, 3D surveys are conduced

Is the current order not factored into the price already? (around 400 to about 900+)

Would the company remain equally debt free even while executing such a sizable order?

Would we not be outweighing our investment based on a single order when the execution could go either way during the next couple of year?

As discussed in the Annual Report, the challenges of steep resource ramp up would remain.

Last, but not the least, crude prices hold lot of significance on the market price of the scrip.

Overall, I think it could be better if we invest after some amount of cooling of price. Perhaps, some more views/reviews of experienced VP members could clear my doubts.

Is the current order not factored into the price already? (around 400 to about 900+)

I still feel there is a lot of upside left in next one year. If you do a simple maths on 10% net margin(they have done better when their that every time their sales reached near 100cr) on a 600Cr sales for FY18, it is trading at 9 times or lower. But that’s my calculation, you can have your own call.

Would the company remain equally debt free even while executing such a sizable order?

No, the company need to do a capex of 100Cr to execute the order. Hence they may take some debt.

Would we not be outweighing our investment based on a single order when the execution could go either way during the next couple of year?

In this business, the client list is very small…so you can’t have multiple orders. Execution risk is always there…

As discussed in the Annual Report, the challenges of steep resource ramp up would remain.

Yes, that’s a challenge but Client supports in such cases as there is none left in India in similar space with good balance sheet.

Last, but not the least, crude prices hold lot of significance on the market price of the scrip.

For India story is different and more strategic in nature. India imports almost 75%+ of oil needs and PM Modi has set a target to reduce the import by 10% by 2025. Hence the roll out of such large order for a huge seismic survey has been rolled out. This is the starting point of OLAP (Open Acreage License Policy) which is going to come in effect from 2019.

Came across this company on couple of custom screens on Screener.in much before this mega order win but never gave it much thought. Alas

To me this looks HUGE both from opportunity and challenges standpoint, therefore need to dive bit dipper:

Annual report 201516 page 20 lists: The order comprises six basins out of the 11 basins considered for seismic data acquisition (one remains un-awarded) aggregating 26,905 line kms of 2D seismic survey to be completed within three years.

Further, page 27 of the investor presentation lists:

The current requirement of data acquisition under NSP is about 50,000LKM.

•Out of this contracts have been awarded for approx. 42,000 LKM. Against this awarded approx. 30,000 LKM. ALPHAGEO has been

•Potential tenders from balance work in the North East approx. 1000 crores

Putting these two factors together, is it correct to conclude that award for 5/6 basis is yet to be awarded? I most likely think so. @raj1968 , @bandlab1 can you please confirm if my understanding/conclusion is correct. Else, who are the competitors who has won the rest 5 blocks. Always helps to look at it from competitors lenses

.

Current order itself has a projection of EPS INR 125/per year for each of the next 3 years. (assuming 15%* net margin on INR 5000 Mil /annual revenue with ~6 mil share outstanding). against current EPS~ INR 20/25 . I understand the stock has ran up quite a bit ( a lot actually), however, even after this run-up the CMP appears to be reasonable if we look at the potential. need to understand what Mr. Market knows that I dont?

* Net margin% for year ending March 2015 was 19.94%

is it more to do with the fact that there is no visibility AS OF NOW on the order pipeline post FY’19? going by the general day to day market behavior I don’t think that. So, the core question is, what Mr. market knows that I am missing?

Understandable that currently company balance sheet is fairly de-leveraged, however, I am sure there must be some general limit/rational upto which company can have debt financing. In this case, currently total balance sheet size of ~ INR 125 Cr. and company is seeking for new Capex of ~100 Cr via ‘low cost long term fund’ (verbatim page 21 of AR) . What that option could be?

Even a combination of debt + equity infusion seems tricky and can impact P/E adversely since current share outstanding are only 6 Million.

Lastly, what is the update on the Quippo (SREI) case. Has ONGC fillled an appeal against the Delhi High court order? Essentially, has that issue been put to rest or we can see any further ghost coming out of closet. @bandlab1 hope you can help understand the current landscape and implications well around this particular issue.

I am not an expert on what and how market thinks and values this type of order driven businesses. in my view next triggers would be

smooth execution of the order over next 3 years without stretching the bs too much

cash flow management, working capital management are very important, we need to watch the management capability in this respect. given their superb execution track record albeit on smaller scale, I am confident they can make this happen

Mgmt has categorically mentioned in AR, Investor Presentation that some more orders could come beyond 2019 from unexplored basins and further indepth survey resulting from the data processed from the existing orders (it could be 3D as well) and govt new policies (HELP, OLAP).

Regarding court case we need to get more details from AGM. We will get more details from AGM on how they are planning to execute this order (even though they explained in detail in AR) and future business prospects

You are absolutely right. Such opportunities(large order) are always an execution challenge. Please read AR for 2016 couple of times, where management did try to explain how they are gearing up for the challenge. Feels convincing but let’s wait to see how it unfolds.

I think under national seismic survey 40000 Line KM out of 50000 is given out by ONGC. OIL India however still have to issue the orders.

Net Margin should be lower as per management interview(hint) to CNBC. This is a 2D order where margin will be slightly lower compared to 3D. Also the order size is a factor for lower margin.

Sales should be 600Cr+ for FY18 as they have to completed this big order by March 2019 which is just 2 1/2 years from now.

As far as debt is concerned it will not be a problem as Management is already infusing 35Cr by way of preferential allotment. I think 25% has already come and rest will come by May 2017. They have zero long term debt, good reserve and decent cash flow as well. Hence debt taken should be minimal and managable.

I feel markets are awaiting the progress of execution before assigning it higher value.

I am planning to attend the AGM, so hopefully will be able to get some more answers of the open questions.

Guys,

I will be attending the AGM on 29th September at Hyderabad. I will try to get some answers from the management.Please do share the questions if you have any.

Group - does any one has access to this paid Petrowatch site? Even in past I concluded that this is containing some useful info around the recent policy shift and also some insight on the ONGC vs. Quippo court battle.

Please summarize the gist of this article from Petrowatch for the benefit of the group.

Thanks

Thanks