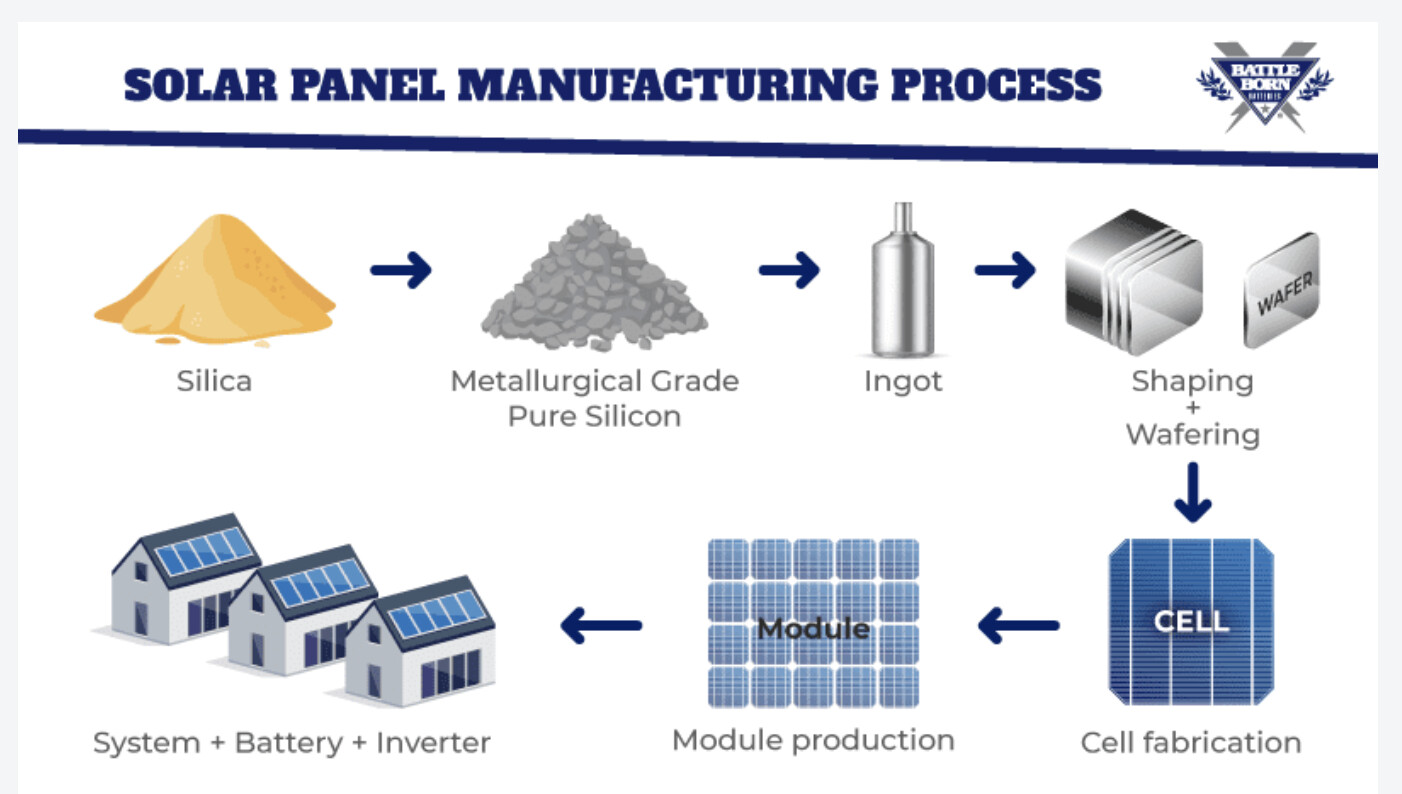

The image above illustrates the solar panel manufacturing process in detail. At present, India has sufficient solar module manufacturing capacity; it is approaching a state of oversupply. However, the country still faces a significant gap in solar cell manufacturing capacity.

In this industry, the level of backward integration directly influences profitability. The more stages of the value chain a company controls, the higher its potential margins. For example, a manufacturer that produces solar cells in-house, rather than depending on imports, can achieve net profit margins (NPM) of around 25%.

Leading players such as Waaree have taken backward integration even further, extending their operations all the way to ingot and wafer production. Waaree is also moving in forward integration to Battery and inverter manufacturing.

Duties on imported modules and cells:

For now, the revised duty structure lowers the tariff on solar cells to 20%, but with an additional 7.5% Agriculture Infrastructure and Development Cess (AIDC). For solar modules, the duty is now 20% with an additional 20% AIDC.

Even after a 40% duty, the solar module imports from China are cheaper.

Source: India Lowers Customs Duties For Solar Cells & Modules

Competition Landscape:

Waaree Energies

Waaree is India’s largest solar module manufacturer with a capacity of 12 GW for solar modules and 5.4 GW for solar cells. By FY27, Waaree targets 26 GW module capacity, 16 GW solar cell capacity, and 10 GW ingot/wafer capacity.

Adani Solar (Adani Energy Solutions / Mundra plant)

Adani Solar operates one of India’s largest integrated solar manufacturing facilities at Mundra, Gujarat. It currently has 4 GW of module capacity and 4 GW of solar cell capacity, with expansion plans to scale up to 10 GW by 2027.

Tata Power Solar

Tata Power Solar is a pioneer in India’s solar industry with more than three decades of experience. It has an installed capacity of 4.3 GW of solar modules and 705 MW of solar cells, with ongoing plans to expand.

Vikram Solar

Vikram Solar is among India’s leading solar manufacturers with a capacity of 3.5 GW of solar modules and 1.2 GW of solar cells.

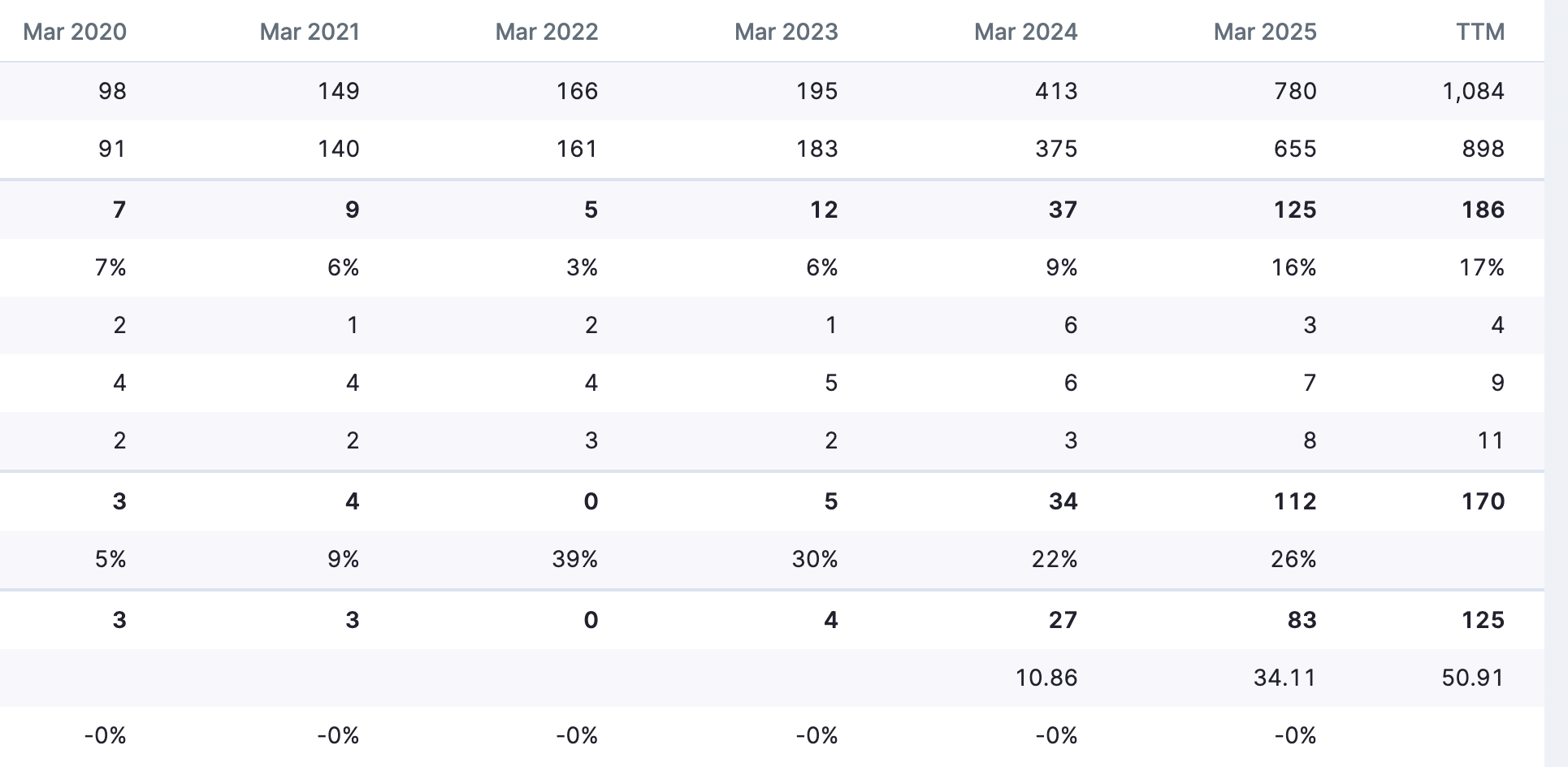

Current Company revenue split:

- Module manufacturing: 1.2 GW ( 94.1% of total Revenues in Q1FY26)

- EPC Services of AC/DC Solar Pumps: ( 5.9% of total Revenues in Q1FY26)

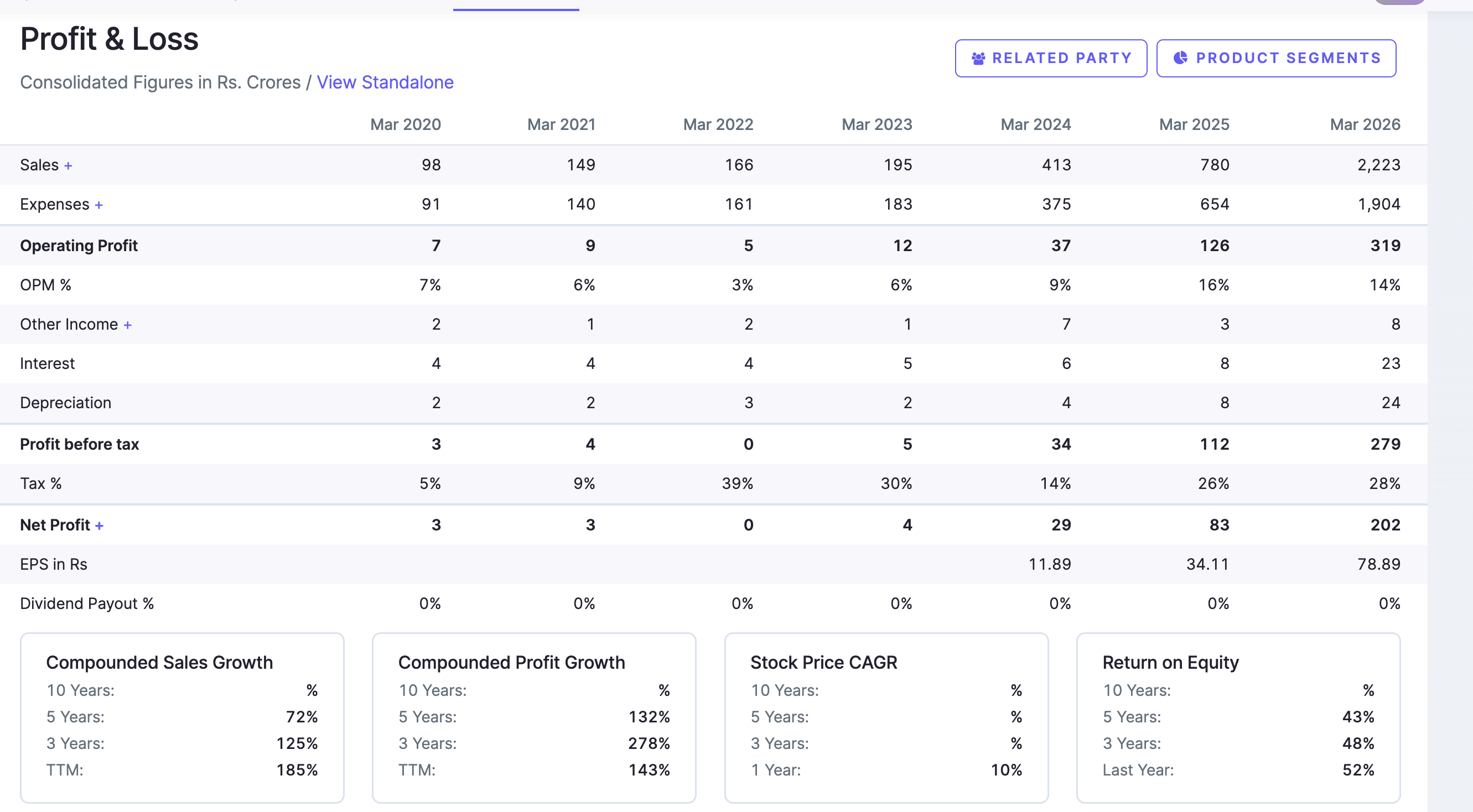

The company is going through massive expansion, raising module capacity from 1.2 GW to 3.6 GW, new cell capacity of 1.2 GW and 12,000 tons of aluminium frame manufacturing.

Order book:

As of August 20, 2025 company has an order book of 1600 cr. (Last FY revenue: 780 crore). They are expecting to execute 1600 cr. of orders in this FY. There are still 7 months left to get extra orders that will spill over in the next FY.

Details of Manufacturing Capacity Expansion

- Module Manufacturing

- Current: 1.2 GW (Greater Noida).

- Expansion: 1.2 GW additional by Nov 2025, and another 1.2 GW by Mar 2026

- Target: 3.6 GW total by June 2026.

- Cell Manufacturing

- New 1.6 GW solar cell line being built in Kosi Kotwan (Mathura).

- To be rolled out in 3 phases: 500 MW + 500 MW + 600 MW over 2 years.

- First 500 MW will be rolled out in Mar 2026.

- Second 500 MW by July 2026

- Rest 600 MW by Dec 2026

- Tech: Mono PERC and TOPCon cells.

- CAPEX: ₹642 crores (funded via internal accruals, equity, and small debt).

- Aluminum Frame Manufacturing

- Setting up capacity of 12,000 metric tons per year at Kosi.

- Backward integration to improve margins.

EPC & IPP Expansion

- Subsidiary Alpex Green Energies Pvt. Ltd. created for EPC & IPP business.

- EPC Projects: Targeting 150 MW installations over next 2 years.

- IPP Projects: Targeting 100 MW installations (with acquired SPV Chandra Energy)

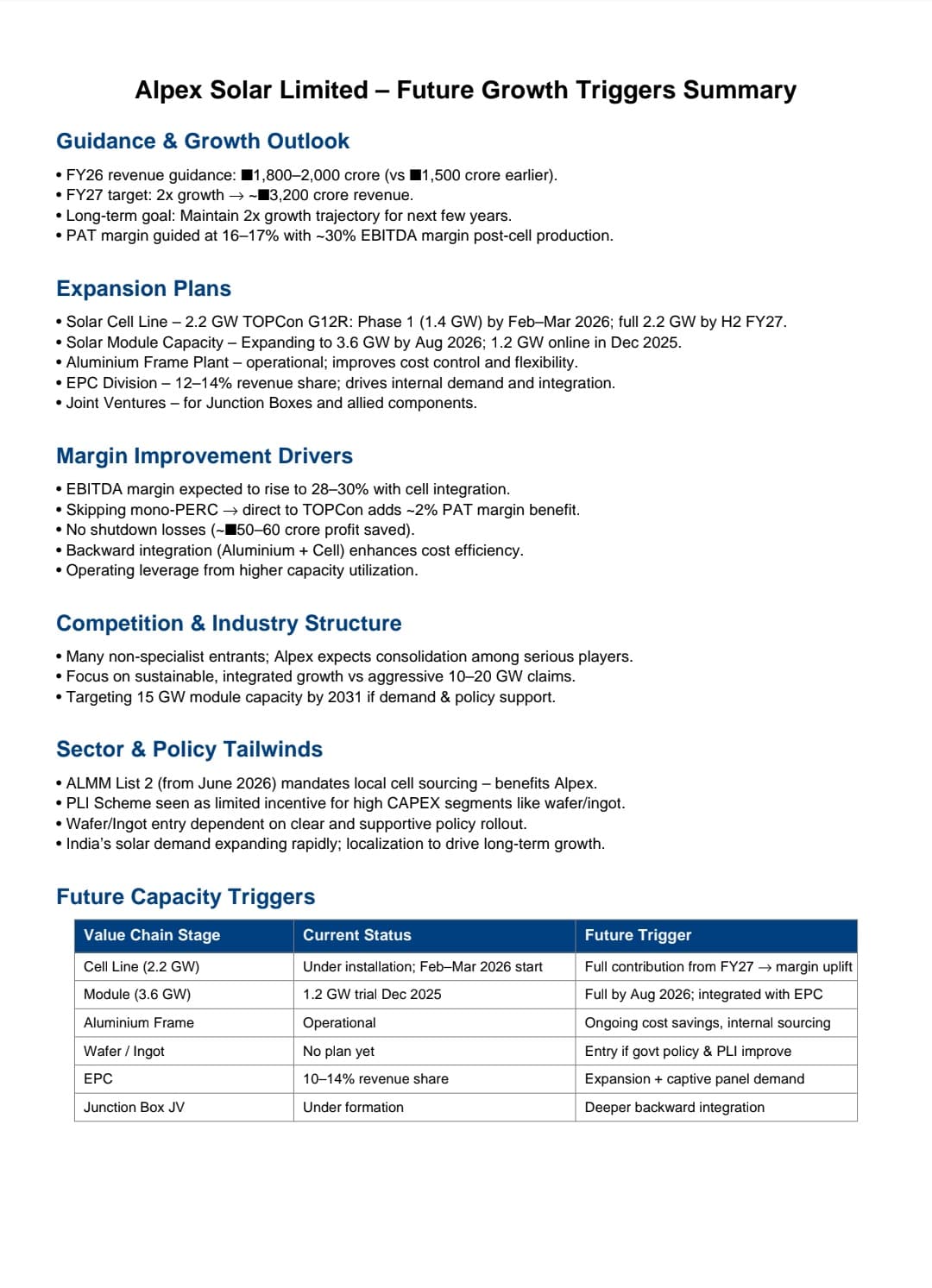

Financials: Company growing at 2x in last few years

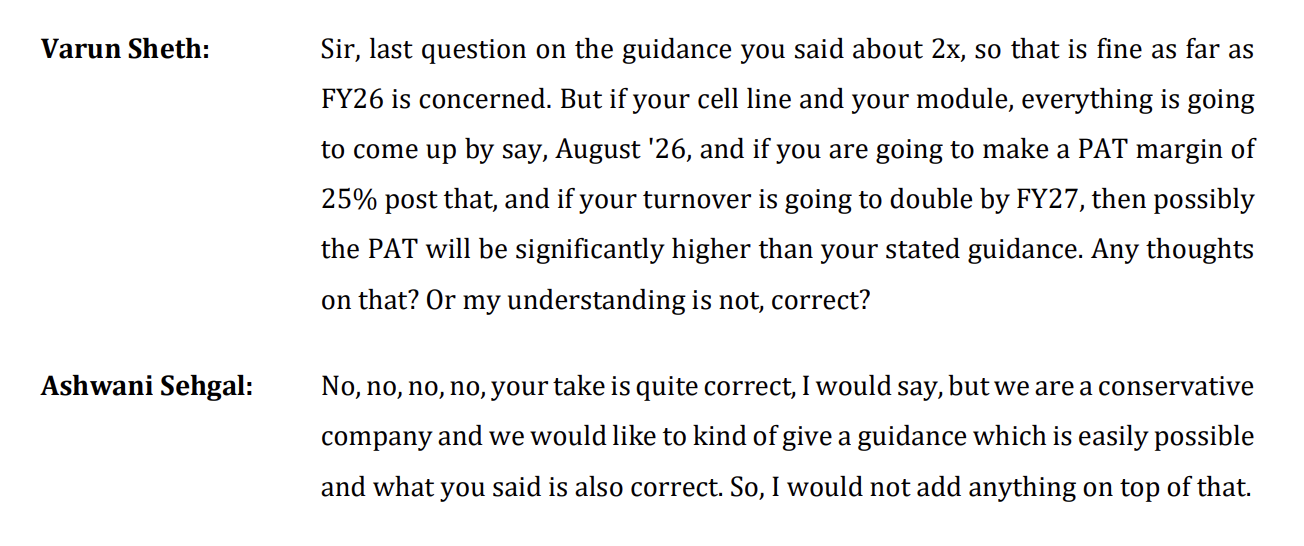

Management Guidance:

Management:

MD - Mr. Ashwani Sehgal, a Mechanical Engineer from Punjab University, has been a stalwart and pioneer in the field of solar manufacturing and currently serves as the General Secretary of the Indian Solar Manufacturers Association that is ISMA where he has also served as the President for 12 years and played a pivotal role in advocating for favorable government policies that benefit solar manufacturers.

CEO - Mr. Aditya Sehgal has a Bachelor’s Degree in Science with a focus on Electrical Engineering from the prestigious University of California. As the CEO of Alpex Solar, Mr. Aditya Sehgal has been driving the global export opportunity and is focused on developing newer markets.

Risks:

- Industry is moving towards Topcon technology, but the company is still going for Mono Perc. As per them their 90% of their order book is Mono Perc and it still has 3-4 years of life left.

- Solar theme is outdated in the market. It might not attract past valuations.

- There is a risk of overcapacity in module manufacturing by FY2030.

- Management is trying cell manufacturing for the first time.

Investment Thesis:

- Increase in PAT margins to 25% because of backward cell manufacturing.

- The company has an ambitious target of 3000 cr topline by Mar 2027.

- Even if the company achieves 3000 cr topline at 18% Net Profit Margin, with a modest PE of 20, it will have 10,800 cr MCAP. Roughly 3x from here. An 84% CAGR return in 2 years.

- The returns will shoot up further if the company achieves 25% NPM (as stated in Q2Fy26 concall), and PE might also expand as cell manufacturing attracts high PE.

Current MCAP: 3200 cr

Disclosure: Invested