Business in detail:

Incepted in 1967.Alpha Laboratories is a leading Contract Research Organization (CRO) in India with its own in-house laboratory facilities for undertaking Bioequivalence / Bioavailability Studies, Clinical Trial Studies, Animal Toxicity Study, Dossier and DMF preparation, Medical Writing, Stability Studies, Analytical Method Development and Validation under one roof. The group has a sound financial footing and has well equipped laboratories at Navi Mumbai. The laboratory is manned by competent personnel drawn from various core areas of services. Company has more than 60 products in market as of now.

Market cap: 69 Crore.

Facility: 1.2 acre near Indore

Pros:

P/E = 7.7

P/B = 0.7

Debt to equity= 0.33

IPO in 2007

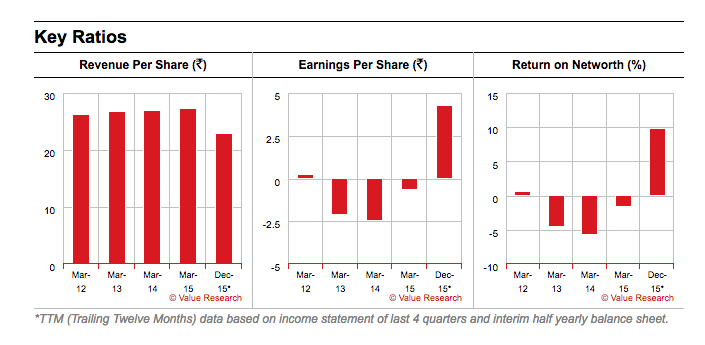

Available cheap probably because the company has given negative growth of -9.2% for last 5 years.First time gave positive earnings in 2015 afters 3 years of losses.

Porinju Veliyath holds share of alpa labs, this stocks fits Porinju’s philosophy of buying beaten down stock available at throwaway price.

Key triggers:

Available at PE of 7.

First time gave positive earnings in 2015 afters 3 years of losses.

Cons:

Negative growth of -9.2% for last 5 years.

Negative ROOE of -3.55% for last 3 years.

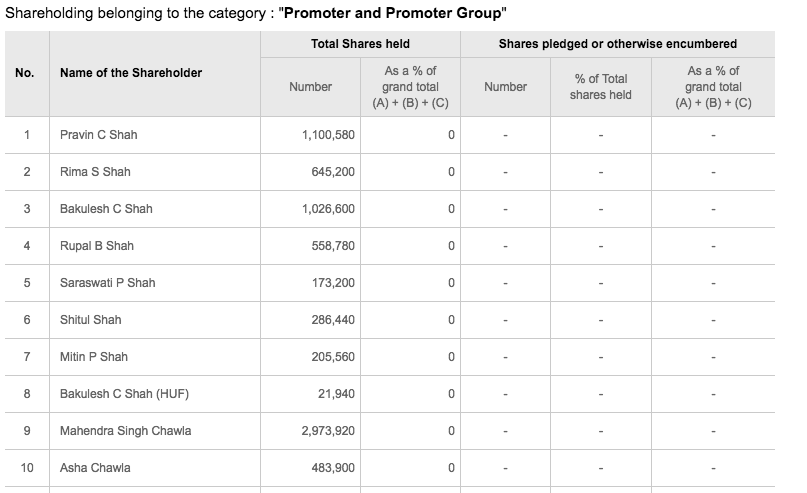

StockHolders stake:

Last five years financials:

Disc: Not invested

2 Likes

It was supposed to release Q4 results yesterday. Any news?

Disclosure: small investment.

Hi, Result is released just now. check BSE website.

Thanks. After very good Q2 - q3 and q4 have been poor. Made a mistake by buying it following Porinju and turn around Q2.

Q4 shows losses because they paid full year’s taxes in single quarter (2.89cr).

Full year the company has turned around with EPS of 3.16.

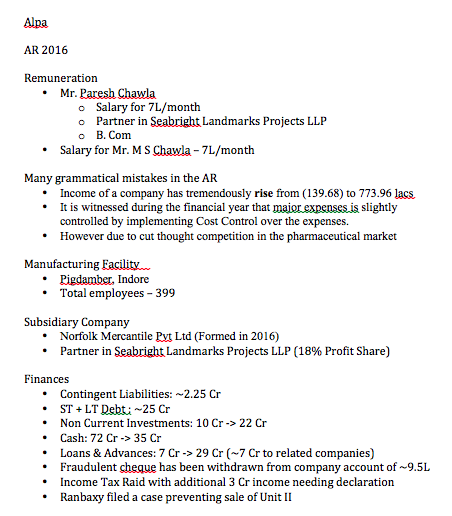

From FY16 balance sheet, company has marketable securities worth 54Cr (19Cr non-current investments + 36Cr in cash). Total debt works out to be - 25Cr (ST + LT).

So net marketable securities work out to be - 29Cr.

The company has market cap of 70Cr.

Removing the goodwill on consolidation from the balance sheet, the book value at the end of FY16 works out to be 64.

As per BSE, The Patels sold their 19% stake to Chawlas in FY16.

http://www.bseindia.com/xml-data/corpfiling/AttachHis/97B38166_C951_4344_AFFD_5DB909A1272A_101719.pdf

http://www.bseindia.com/xml-data/corpfiling/AttachHis/78D4F46D_BF30_4849_B2A4_4DC441910B0D_171617.pdf

One peculiar thing I see is that the shares were to be purchased at weighted average market price (WAMP) quoted on BSE/NSE for last 60 days.

The notice was issue in end of March and stock was trading at very high price preceding 3-4 months.

I think SEBI should investigate this part.

Company had 2 units of business operations - domestic and regulated markets.

They regulated business was making losses as company was not able to handle all the requirements.

They sold off that unit and turned around the company. We need to see what Chawlas do with the cash generated from the Sale of the unit.

The stock can be treated as turnaround and asset play at the same time in Lynch parlance.

Thanks,

Rupesh

Disc - Bought during the rally of Jan-Mar and currently staring at losses. But I want to give Chawlas another quarter or two to see what do they do with cash and plans for future. So I continue to hold

1 Like

Thanks for clarifying. I agree with you. At EBITA and pre tax level it is a big turn around. Sales have gone up significantly in Q4. Appears interesting. Worth holding and keeping a close watch.

Disclosure: sitting on huge losses as I bought in Dec and Jan following Porinju.

1 Like

Do we have any info on Chawlas.

Disc - I hold, looking to exit, not a buy/sell reco

2 Likes

What are the products of the company?